Did you ever look at your bank account 10 days past your pay day and wonder why I am poor despite a very satisfying salary package? Do I need a part time job to meet my both ends? Do I need to borrow money from a friend or bank this month again? The only answer to all these questions is “personal finance management”.

When you introduce discipline in your life, you make your life easy.

When you enter discipline in your finances, you make your financial life smooth.

This article will enlighten all the aspects of your life that are making you feel poor when you are not even poor and give you a road map of wealth, financial stability, and mental peace.

Why do you need Personal Finance Management?

Back in 2022, despite earning quite well, my financial life was drastic.

Different studies suggest that a large percentage of people live paychecks to paychecks due to poor personal finance management; I was one of them.

I was earning almost $2500 from a corporate job. At that time, I was living with my parents, so I had no rent or other major expenses.

Still, I used to become financially miserable by the end of the month. I was not very happy about this situation.

After months of mental exhaustion of borrowing money from my friend’s circle, parents and colleagues.

I finally decided to find the root cause of my suffering.

On a random Sunday evening, I sat down with a hot cup of my favorite chocolate milk in my hand.

I opened a spreadsheet.

Write down my total income.

Then, one by one I enlist all the expenses.

At the end of the list, I was shocked. I came to this realization that I was spending a massive amount of my income on unnecessary and useless things.

Here is a sample of my spread sheet realization list:

| INCOME | ||

| DATE | SOURCE | AMOUNT |

| 1/9/2022 | Basic pay | $2200 |

| 1/9/2022 | Commission | $300 |

| TOTAL INCOME | $2500 | |

Now, check out the list of expenses:

| Expense | Amount |

| Car loan | $400 |

| Maintenance | $300 |

| Parcels | $500 |

| Outdoor dinning’s | $500 |

| Mobile loan | $300 |

| Subscriptions | $200 |

| Travelling | $300 |

| Total Expenses | $2500 |

I was shocked because I realized I gave $500 just to McDonald’s and KFC because I was bored at midnight.

I ordered useless things from amazon just because I was in a bad mood and needed dopamine to feel good.

I was spending $200 on subscriptions of platforms I didn’t even get time to watch.

I was saving $0.

I had no emergency funds.

With such carelessness, I usually got out of money by mid of the week and had to take loans to manage remaining days.

I am sure most people can relate to this story.

Now let’s get to the plan of how I broke this pattern and made my financial life better and how you can do it too.

7-STEP guide to Personal Finance Management:

Here is a step-to-step guide to implement Personal finance management into your life:

STEP 1

Identification of Problem:

My first step towards financial stability was awareness. Like every other problem, fixing a problem requires identification of the problem.

Recognize your problem.

Sit down and ask yourself questions like:

- How am I struggling financially in my life?

- Are my expenses exceeding my income?

- How can I save more?

- How can I pay my debts?

- What are my future goals?

These are some basic questions you can ask more than that.

Take a pen and notebook and start writing down the answer to every question.

It can give you mental clarity. You will be able to identify the core reason for your financial struggles.

Identification of a problem is just like stepping into your new house, which is dark inside, you put on the light, and everything is covered in dust and filth. You hated the scene; you don’t like a single thing about the house but putting on the light gives you an insight to see everything clearly and power to change what you don’t like.

STEP NO. 2

Track Income and Resources.

First, write down all your income sources.

I was a salaried person but not everyone gets the same fixed amount of income every month. There are diverse voices and cultural tailoring in financial matters.

For example, gig workers or freelancers who work remotely, or their income is earned on a per project basis.

So, their monthly income can vary every month.

Then, there are caregivers who mostly get paid for their services according to per hour or per day, so for them, personal finance management can be different from salaried or gig persons.

Students usually get pock moneys or stipends to manage their expenses.

So, your life stage is essential for you to create a realistic budget and set or achieve your future goals.

I am sharing my budget plan with you; you can add layers or customize them according to you.

I used spreadsheet, you can use traditional notebook and pen method.

STEP NO. 3

Set a Budget:

To set a budget,

- Accurately assess your monthly income.

- Make three categories.

- NEEDS

- WISHES

- SAVINGS

As suggested by UNFCU, You can use the 50/30/20 rule here.

Give 50% to your basic needs, 30% budget to your wishes, and save 20%.

It’s just like a water tank, water getting into the tank is your income, water overflowing from the tank is your expenses, and stored water is your savings.

Now, personal finance management is about balancing out the ins and outs of the water tank and store enough for later use.

STEP NO. 4

Allocate Money:

Now, wisely allocate money to the three categories you made.

First, cover all your basic needs.

Then, give money to wishes and put the remaining money in the saving category.

Now most of you will put the remaining money in the saving category after all the spending.

Here is a powerful hack.

I tried it and it works magic for me till this day.

Always give the money to the savings category first and then spend the remaining money.

In my case, I had a total income of $2500. So, I stopped using all my money to set my budget.

I simply put $500 aside and created my budget from $2000. It automatically cut out my unnecessary spendings.

Here is a look at my budget planner after implementing this strategy.

| Expense | Amount |

| Car loan | $400 |

| Maintenance | $300 |

| Parcels | $300 |

| Outdoor dinning’s | $100 |

| Mobile loan | $300 |

| Subscriptions | $200 |

| Travelling | $300 |

| Emergency Fund | $100 |

| Savings | $500 |

| Total Expenses | $2500 |

STEP NO. 5

Create an Emergency Fund:

When do you need to borrow money from others? Sudden incidents that disrupt your whole budget of the month left you behind in debt.

The best way to deal with such situations is to create an emergency fund during your budget allocation process.

Always set some money aside for emergency situations.

STEP NO. 6

Eliminate Debt:

If you are under debt, first eliminate it.

Cut out all other unnecessary expenses and fix an amount to repay all the debts.

STEP NO. 7

Start Investing:

The best way to utilize your saved money is investing it somewhere. There are a lot of money investment options like stocks for long-term growth, Mutual funds and saving accounts etc. that can protect your money and give you profit as well. To explore those options, you can check out this article.

What is the definition of “rich” for you?

Being rich does not mean increasing your income or winning a lottery or some hidden treasure that would solve all your financial problems.

Mostly, Increased income alone never solves your financial problems without proper personal finance management.

Only proper financial management can solve your financial problems.

If you tally my before and after budget draft, you can clearly see that I was earning enough money for myself, but I was not organized.

When I started practicing personal finance management strategies, my income remained the same, but a shift in my priorities changed my financial situation as well.

I cut out unnecessary expenses by 30% and within 3 months I started to save enough money to invest somewhere and created an emergency fund for myself.

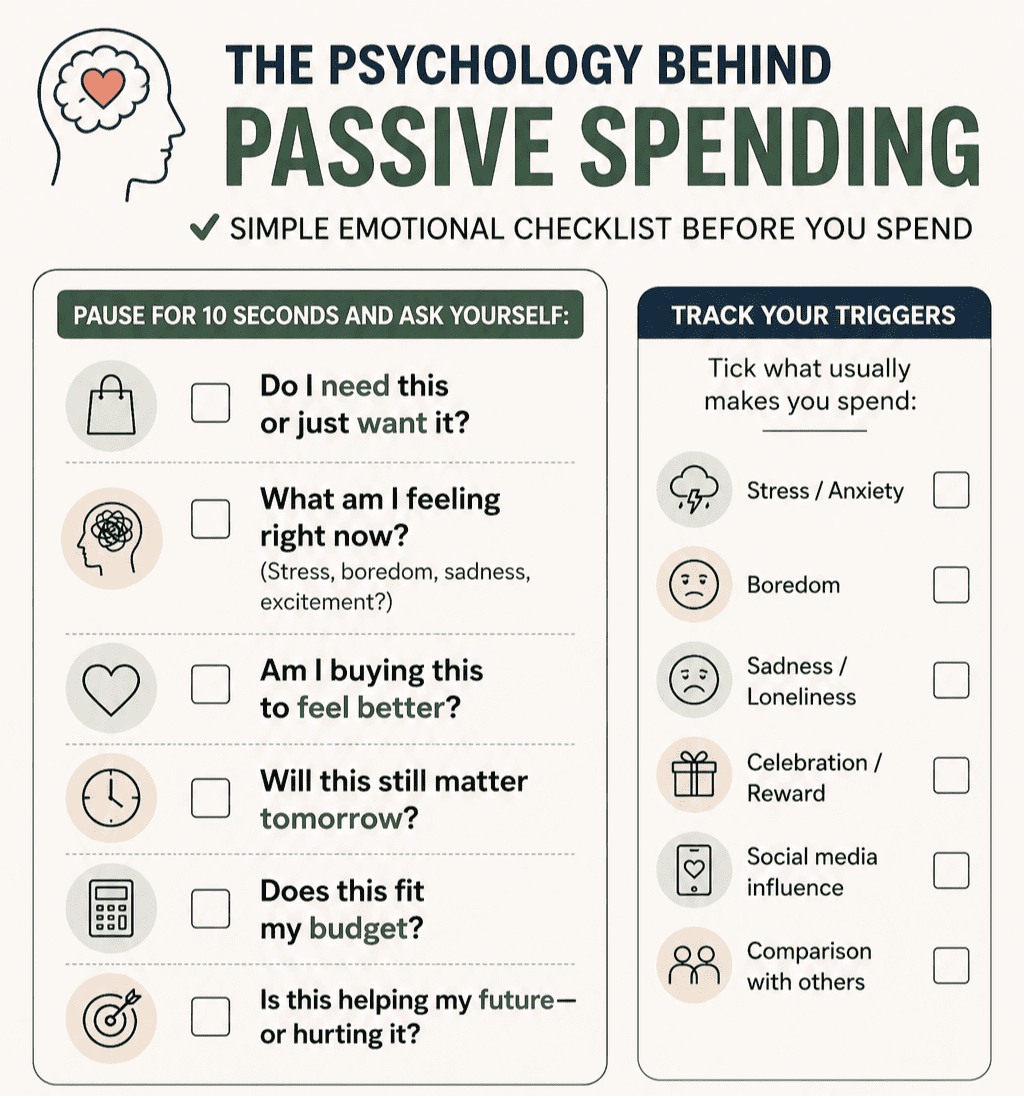

The Psychology Behind Passive Spending:

Mostly people don’t buy things because they need them rather, they want them.

Making impulsive purchases gives you momentarily relief and satisfaction. But it can cause leaks in your budget that will make you regret it later.

You also need to track your emotional triggers for successful personal finance management.

Here is a checklist for your emotional triggers. Before making any purchase, take a deep breath and mark this list.

Conclusion:

Take a step towards your financial stability today.

This article is based on a real-life case study about how to manage your finances and implement personal financial management in your life.

You can customize your budget according to your financial status and life stage.

Crack what works for you and stick to it. Remember that consistency is key. I have been following this financial routine for almost 3 years now and I am in a much better place now financially and emotionally.

Personal finance management is about setting priorities right and introducing mindful choices in your life.

3 thoughts on “HOW TO BECOME RICH; A PROVEN 7-STEP PERSONAL FINANCE MANAGEMENT GUIDE ”