Your 20s are the single best time to get smart with money and build financial habits, because small decisions made now compound into big results by your 30s and 40s. Most people wait until debt piles up, or a financial crisis hits before they pay attention. You do not have to be one of them.

This guide breaks down exactly how to be smart with money, from building a budget to making your first investment, without needing a finance degree or a six-figure salary.

What does Being Smart with Money actually mean?

Being smart with money does not mean being cheap. It is about making intentional choices with what you earn, so you are not scrambling at the end of every month.

Smart money habits come down to three core areas:

- Spending less than you earn

- Saving and investing the difference consistently

- Avoiding high-interest debt.

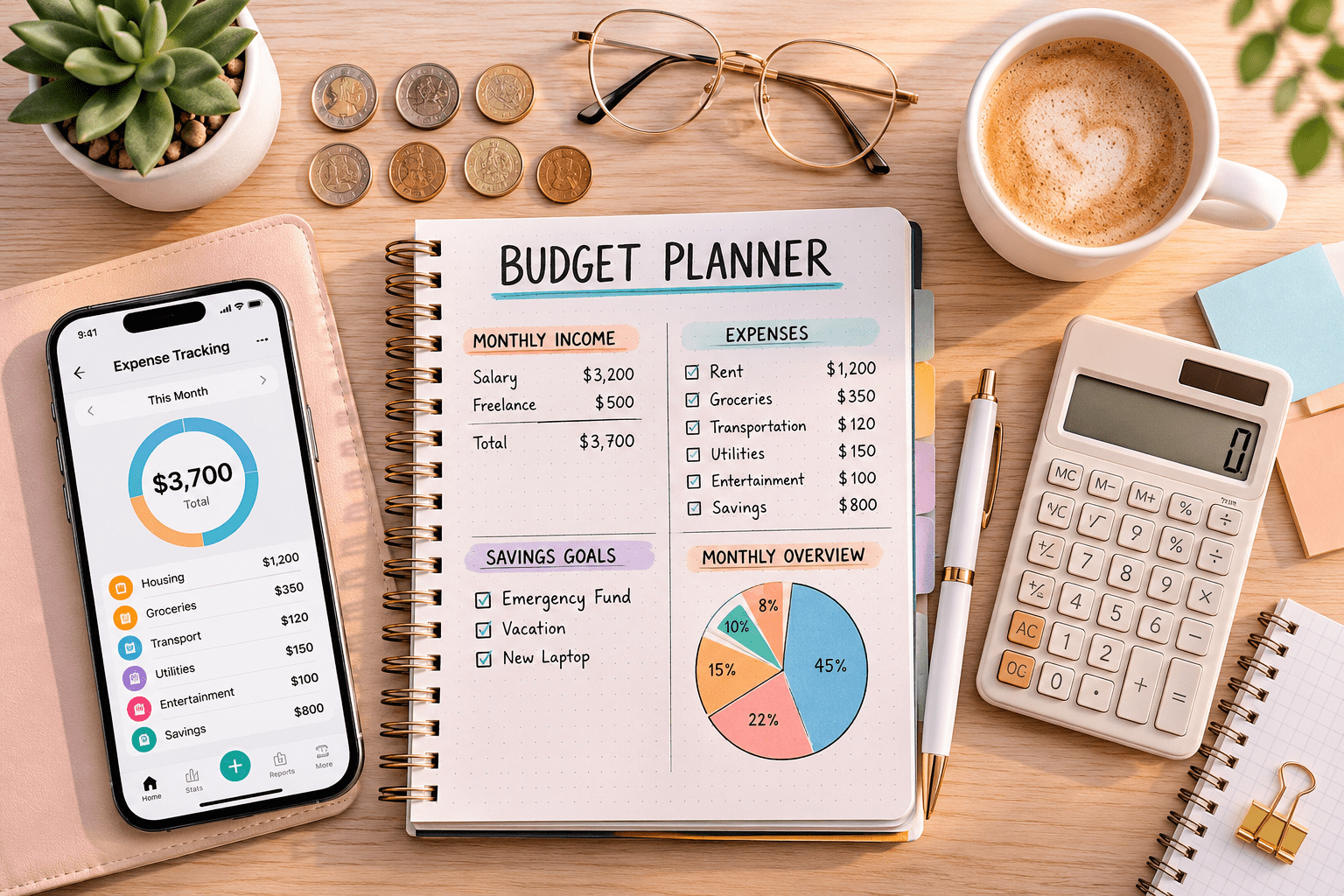

Build a budget that you will actually stick to?

Most people fail at budgeting because their system is too rigid. They make unrealistic goals in budgeting. They stay consistent and track every penny for 2 weeks and then give up.

The budget should be flexible.

The 50/30/20 rule explained to get smart with money

The 50/30/20 rule is the most practical framework for young adults:

⦁ 50% of your after-tax income goes to needs (rent, groceries, transport)

⦁ 30% goes to wants (eating out, subscriptions, entertainment)

⦁ 20% goes to savings and debt repayment

If your income is consistent, adjust the ratios but keep the structure. The goal is to give every dollar a job before your account hits zero.

Tools to Track your spendings:

If you hate spreadsheets, you don’t need one.

These applications make money tracking automatic:

⦁ Rocket Money: links to your bank and categorizes transactions

⦁ YNAB (You Need a Budget): best for people who want full control

⦁ Your bank’s app: most major banks now have built-in spending breakdowns

Pick one and check it weekly. Five minutes a week is enough to stay aware.

Smart Money Habits to start this month:

Habits beat motivation to be smart with money. Here are the two highest impact ones to build right now.

Pay Yourself First:

Before you pay rent, bills, or anything else, transfer a fixed amount to savings the day your paycheck arrives. Even if it is $50 a month. The habit matters more than the amount in the beginning.

Cut Expenses Without Feeling Deprived:

Cutting costs does not mean living like a monk. Target the areas that drain money without adding real value:

⦁ Subscriptions you forgot about (audit these quarterly)

⦁ Food delivery fees (cooking twice a week at home cuts costs significantly)

⦁ Unused gym memberships

⦁ Impulse purchases from late-night online browsing

A simple rule: wait 48 hours before buying anything over $30 that is not a necessity.

Most impulse urges disappear on their own.

Smart Ways to Save Money on Groceries and Daily Spending:

Groceries are one ofthe easiest categories to cut without sacrificing quality. Here is what actually works:

⦁ Shop with a list: unplanned trips lead to unplanned spending

⦁ Buy store-brand staples: flour, canned goods, pasta, and cleaning products are almost identical to name brands

⦁ Use cashback apps: apps like Ibotta or Fetch Rewards give you money back on everyday purchases

⦁ Meal plan for the week: knowing what you will cook prevents food waste, which is essentially throwing cash in the bin

⦁ Buy in bulk for non-perishables: unit price drops significantly on items you use consistently

These are not groundbreaking tips. The groundbreaking part is actually doing them every week.

Smart Ways to Invest Money in Your 20s

Saving money keeps it safe. Investing money makes it grow. Both matter.

Start With an Emergency Fund:

Before you invest a single dollar, build an emergency fund of 3-6 months ofliving expenses. This is not optional. Without it, one unexpected car repair or medical bill forces you to pull money out ofinvestments at the worst time.

Keep your emergency fund in a high-yield savings account – not your regular checking account. Most online banks now offer 4-5% APY, which is far better than the 0.01% most big banks offer.

Low-Risk Investment Options for Beginners

Once your emergency fund is solid, start here:

⦁ 401(k) with employer match – ifyour employer matches contributions, that is a 50-100% instant return. Always take the full match first.

⦁ Roth IRA – contributions are made with after-tax money, and growth is tax-free.

The 2024 contribution limit is $7,000 per year. (Source: IRS.gov)

⦁ Index funds – low-cost, diversified, and outperform most actively managed funds over time. S&P 500 index funds are a standard starting point.

⦁ High-yield savings – for money you will need in under 3 years, keep it in savings rather than the market.

The best investment strategy for your 20s is boring: contribute consistently, do not panic-sell during market dips, and let time do the heavy lifting.

Common Money Mistakes Young Adults Make

Avoiding mistakes is just as important as building good habits. These are the most common ones:

⦁ Carrying credit card balances month to month – credit card interest rates average 20%+, which wipes out any savings gains

⦁ Lifestyle inflation – every raise gets spent on a nicer apartment or newer car, leaving nothing to invest

⦁ Skipping health insurance – one hospital visit without coverage can set you back years financially

⦁ Not reading financial aid or loan terms – student loan repayment surprises catch thousands ofpeople offguard each year

⦁ Waiting until you “earn enough” to start saving – there is no perfect income level to start. Starting small beats not starting.

Start Now, Not Later:

The difference between people who are financially stable in their 30s and those who are not almost always comes down to habits built in their 20s, not salary, not luck, not family wealth.

Pick one thing from this guide and do it today. Set up the automatic savings transfer. Cancel one subscription. Open that Roth IRA account. One action beats ten plans sitting in your notes app.

And ifyou want to keep building from here, check out our guides on smart ways to invest money and how to build a budget from scratch.

To get more insights on personal finance management, check out this article.