Most people think of health insurance as one thing. You pay your premium, you get sick, the insurance helps pay the bill. Simple enough, right? But if you have ever tried to get coverage for something outside the standard list, like fertility treatments, hearing aids, or mental health therapy, you know it is not always that straightforward. That is where specialized coverage comes in.

Specialized coverage in health insurance fills the gaps that regular plans leave behind. It is designed for people who need something a little different from the typical Bronze or Silver plan on the marketplace. If you have a chronic condition, work in a high-risk field, need specific therapies, or just want more comprehensive protection, specialized coverage could be exactly what you are looking for.

In this guide, we are going to break it all down for you. What specialized coverage is, what it includes, who needs it, and how to find the best plan for your situation.

What Is Specialized Coverage in Health Insurance?

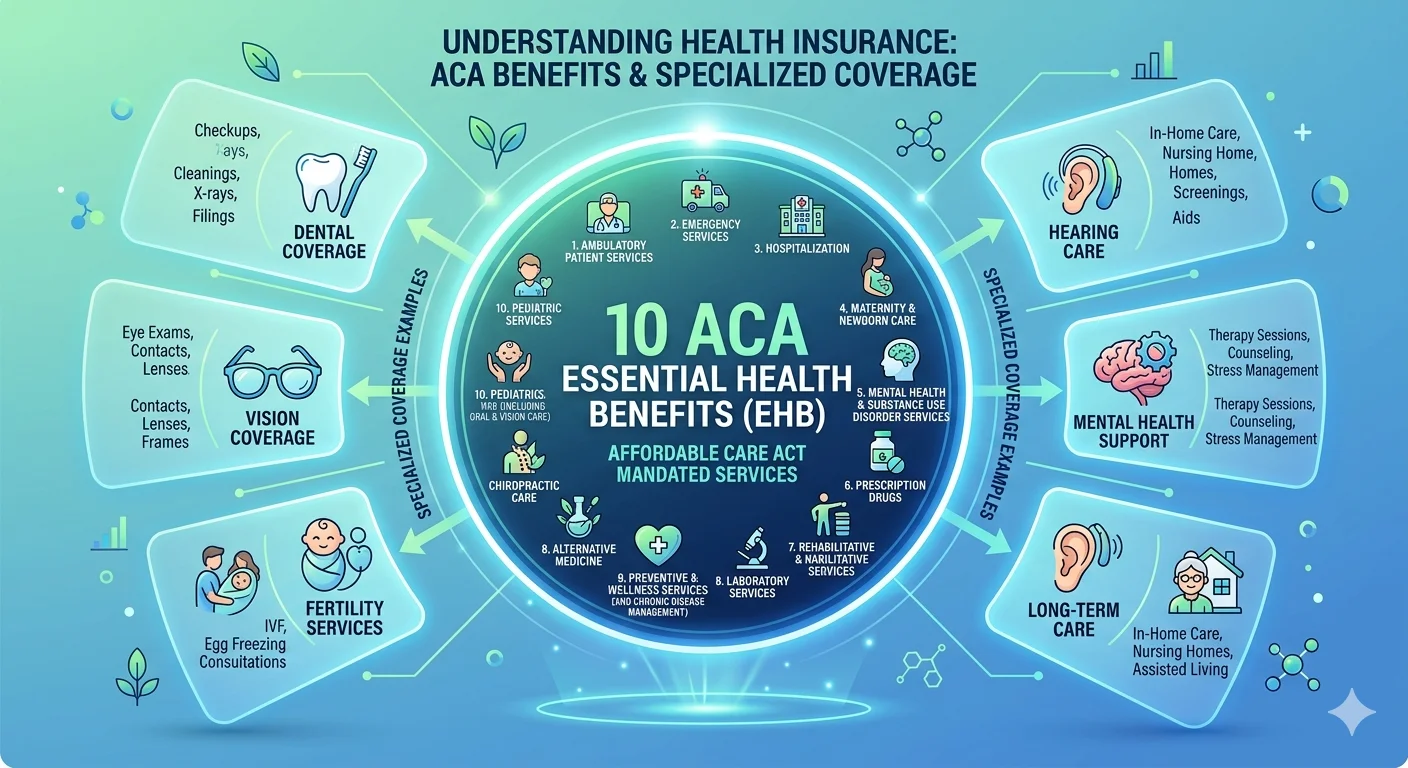

Specialized coverage refers to insurance plans or add-on policies that go beyond the standard essential health benefits. The Affordable Care Act (ACA) requires all marketplace plans to cover ten essential health benefits, things like emergency services, hospitalization, prescription drugs, and preventive care. But there is a whole world of healthcare needs that fall outside of that list.

Specialized coverage in health insurance fills those gaps. It can come in several forms:

- Standalone specialty plans that cover a specific type of care

- Riders added to your existing health plan for extra protection

- Supplemental insurance policies that pay out when you need a specific type of treatment

- Niche or high-risk plans designed for specific professions or conditions

Think of it this way: a standard health plan is like a general store. It carries the basics. Specialized coverage is like a specialty shop that stocks exactly what you need and nothing else gets in the way.

Who Needs Specialized Coverage?

Specialized coverage is not just for people with complicated medical histories. There are many situations where a standard health plan simply does not cut it. Here are some of the most common ones:

People With Chronic Conditions

If you are managing diabetes, heart disease, multiple sclerosis, or another ongoing condition, your healthcare needs are higher and more specific than average. Specialized coverage options like disease management programs or supplemental policies can help reduce your out-of-pocket costs and give you access to specialists and treatments that standard plans may limit.

Professionals in High-Risk Fields

Certain jobs carry inherent risks. Construction workers, healthcare professionals, and first responders often face a higher chance of injury or illness on the job. Specialty accident and health insurance is specifically designed for people in these fields, offering benefits that standard group health plans do not always provide.

Families Planning for Pregnancy or With Fertility Concerns

Fertility treatments and assisted reproduction are rarely covered under basic plans. Specialized coverage for fertility can include IVF, IUI, egg freezing, and related medications. If building a family is part of your plan, this type of coverage deserves serious consideration.

People Needing Mental Health or Substance Use Support

While mental health parity laws require most plans to cover mental health at the same level as physical health, many people still find that their coverage is limited in practice. Specialized mental health coverage can provide access to more therapy sessions, residential treatment, or specialized programs without hitting a cap too quickly.

Seniors Needing Long-Term Care

Medicare does not cover long-term care such as nursing home stays or in-home care for activities of daily living. A standalone long-term care insurance policy is one of the most important forms of specialized coverage for people approaching retirement age.

Common Types of Specialized Coverage in Health Insurance

There are more options out there than most people realize. Here is a look at some of the most widely used forms of specialized coverage:

Dental and Vision Insurance

These are the ones most people are already familiar with. Standard ACA plans do not include dental or vision for adults, so separate dental and vision plans are among the most common forms of specialized coverage. Costs vary widely, but even a basic dental plan can save you significantly on routine cleanings and unexpected work.

Mental Health and Behavioral Health Coverage

Beyond what a standard plan covers, there are standalone behavioral health plans and mental health riders that expand access to therapy, psychiatric care, and substance abuse programs. If mental wellness is a priority, this type of specialized coverage is worth exploring.

Critical Illness Insurance

Critical illness coverage pays a lump sum if you are diagnosed with a serious condition like cancer, a heart attack, or a stroke. The specialty insurance market is currently growing at a significant pace, and critical illness plans are one of the fastest-growing categories. The reason is simple: major illnesses come with major costs that go well beyond hospital bills, including lost income, travel for treatment, and home modifications.

Accident Insurance

Accident insurance pays a benefit if you are injured in a covered accident. It can help cover emergency room visits, ambulance rides, follow-up care, and even lost wages. This is popular with people in active lifestyles or physical jobs.

Disability Insurance

Short-term and long-term disability insurance replaces a portion of your income if you are unable to work due to illness or injury. This is particularly important for self-employed people or those whose employer does not offer disability benefits.

Fertility and Reproductive Health Coverage

Coverage for fertility treatments, prenatal care enhancements, and reproductive health services is becoming more available as demand grows. Some employers now offer this as part of their benefits package, but standalone plans are also available.

Pet Insurance

Yes, pet insurance counts as specialized coverage too. Veterinary costs have risen dramatically, and having a plan for your pet can protect you from unexpected large bills.

How Specialized Coverage Works With Your Main Health Plan

Most specialized coverage is not meant to replace your primary health insurance. Instead, it works alongside it. Here is how that typically looks in practice:

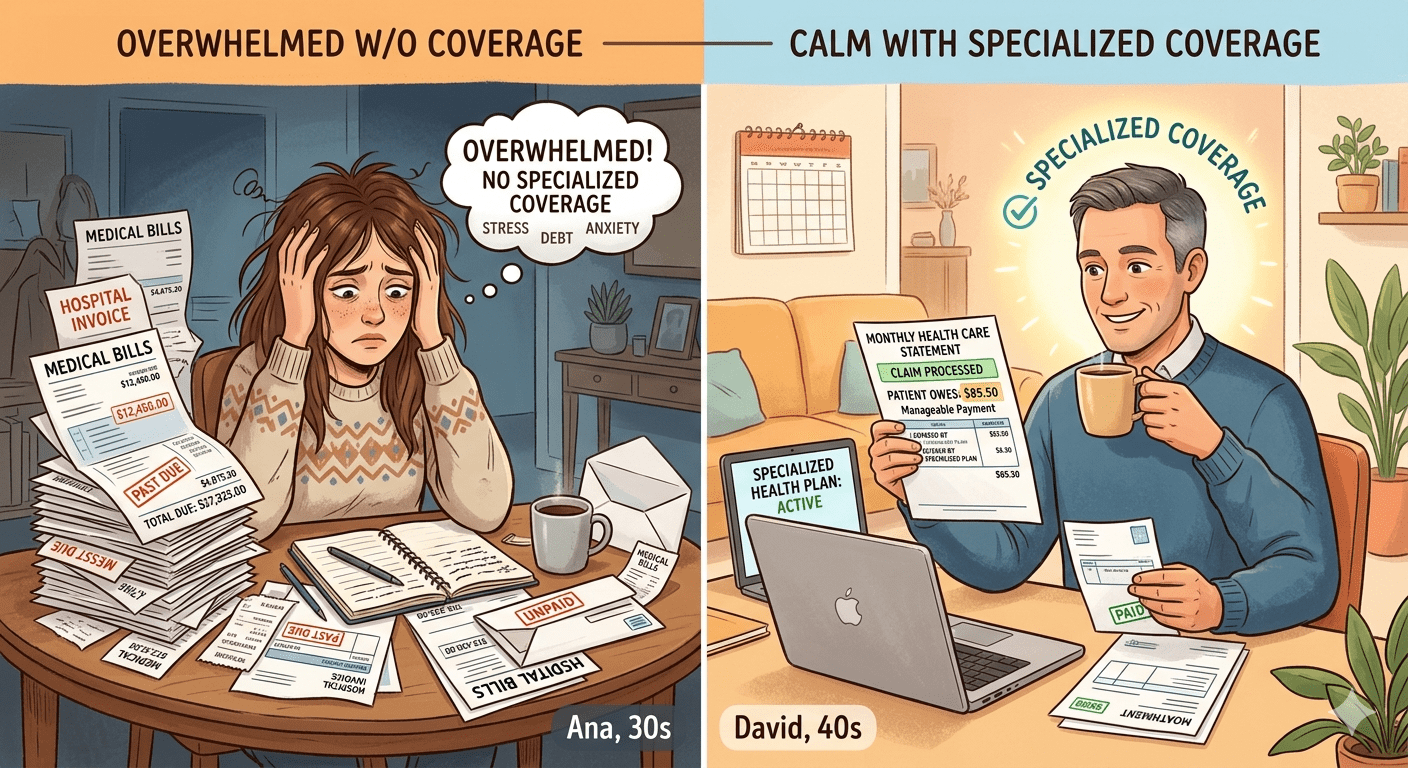

Your main health insurance plan handles the bulk of your medical care. Then, if you face a situation that falls outside of what it covers, your specialized plan steps in. For example, if you are diagnosed with cancer, your standard plan may cover your hospital stays and treatments. But a critical illness policy could pay you a separate lump sum to cover your mortgage while you recover, replace lost income, or pay for travel to a specialist.

Some specialized coverage, like dental or vision plans, work completely independently. You pay a separate premium and use that plan specifically for those services.

What to Look for When Choosing Specialized Coverage

Shopping for specialized coverage can feel overwhelming because there are so many options. Here are the key things to focus on:

- What specific need am I trying to address? Start with the gap, not the product.

- Does the specialized plan coordinate with my existing health insurance?

- What are the waiting periods before coverage kicks in?

- Are there annual or lifetime benefit limits?

- What does the plan actually cost, including premiums and any cost-sharing?

- Is the insurer financially stable and well-reviewed by policyholders?

It is also worth checking if your employer offers any specialized coverage as part of your benefits package. Many employers are adding supplemental options like critical illness, accident insurance, and expanded mental health coverage as employee expectations around benefits continue to evolve.

How Much Does Specialized Coverage Cost?

Costs vary widely depending on the type of coverage, your age, health status, and location. Here are some general ranges to give you an idea:

- Dental insurance: $15 to $50 per month for individuals, more for families

- Vision insurance: $5 to $25 per month

- Critical illness insurance: $25 to $100 per month depending on coverage amount

- Accident insurance: $10 to $40 per month

- Short-term disability: typically 1 to 3 percent of your annual income in premiums

- Long-term care insurance: $100 to $300 per month, depending heavily on age at purchase

The younger and healthier you are when you purchase these plans, the lower your premiums will generally be. Waiting until you have a health issue to look into specialized coverage often means higher costs or outright exclusions.

Where to Find Specialized Coverage

There are several places to look for specialized coverage depending on what you need:

- Your employer benefits package during open enrollment

- The ACA Marketplace for supplemental and standalone plans

- Private insurance brokers who specialize in niche or supplemental coverage

- Professional associations, which sometimes offer group rates on specialty plans

- Direct from insurers, especially for dental, vision, and critical illness products

If you are not sure where to start, a licensed insurance broker can help you identify the gaps in your current coverage and recommend options that fit your budget and needs. There is no one-size-fits-all answer here, which is exactly why specialized coverage exists.

Final Thoughts

Specialized coverage in health insurance is not a luxury. For many people, it is a smart financial safeguard that prevents one unexpected health event from derailing everything else. Whether you need dental, vision, disability, critical illness, mental health, or fertility coverage, there are plans out there built specifically for your situation.

The key is to start with your needs, understand what your current plan covers and what it does not, and then look for specialized coverage that fills those specific gaps. It takes a bit of research, but the peace of mind it brings is well worth the effort.

Need help comparing health insurance options? Fiscible.com is here to make your financial decisions simpler and smarter.