Having a baby is one of the most exciting things you will ever do. It is also one of the most expensive, at least in the United States. A standard hospital birth without insurance can cost anywhere from $10,000 to $30,000 or more. And that is for a straightforward delivery with no complications. The moment you add a C-section, a NICU stay, or even a routine epidural with an out-of-network anesthesiologist, those numbers climb fast.

Maternity care health insurance is what stands between you and a bill that could take years to pay off. But not all maternity coverage is created equal. Some plans cover more than others. Some have waiting periods. Some have networks that may or may not include the OB you have seen for years. Understanding your options before you need them is the smartest move you can make.

This guide breaks down everything you need to know about maternity care health insurance: what it covers, what it does not, how to compare your options, and how to make sure you are ready before the baby arrives.

Is Maternity Coverage Required by Law?

Yes, and this has been the case since 2014. Under the Affordable Care Act, maternity and newborn care is one of the ten essential health benefits that all individual and small-group plans must cover. This includes plans sold through the Marketplace and most employer-sponsored group plans. Before the ACA, the majority of individual health insurance policies did not include maternity coverage at all. Pregnancy was often treated as a pre-existing condition and could result in denied coverage or unaffordably high premiums.

Today, that is no longer allowed. If you enroll in an ACA-compliant plan, maternity care health insurance is included automatically. You do not need to add it as a rider or pay extra for it. The coverage applies even if your pregnancy begins before your coverage start date.

There are a few exceptions worth knowing. Grandfathered plans, those that existed before the ACA was passed and have not significantly changed since, are not required to offer maternity coverage. Short-term health plans, which provide coverage for less than four months, also do not have to include it. If you are on one of these plan types, you should review your coverage carefully before planning a pregnancy.

What Does Maternity Care Health Insurance Actually Cover?

Coverage varies by plan, but under ACA requirements, all compliant plans must cover a core set of maternity-related services. Here is what that typically looks like:

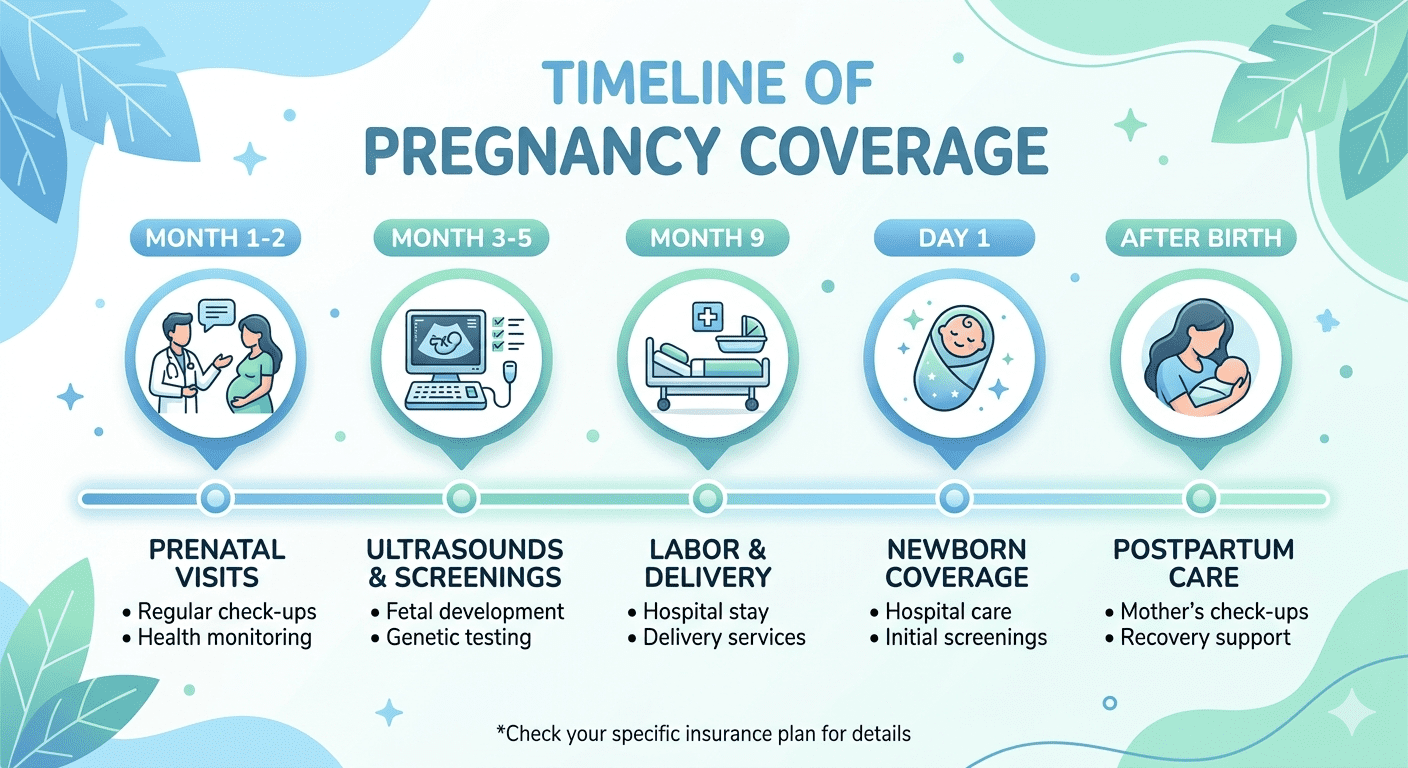

Prenatal Care

Regular checkups throughout your pregnancy are covered. This includes office visits with your OB-GYN or midwife, ultrasounds, blood tests, and screenings for conditions like gestational diabetes, anemia, and Rh incompatibility. Many preventive prenatal services, including folic acid supplements prescribed by your doctor, are covered with no cost-sharing required. That means no copay, no deductible.

Labor and Delivery

Hospitalization for labor and delivery is covered, whether you have a vaginal birth or a cesarean section. This includes the facility fee, nursing care, anesthesia (assuming your anesthesiologist is in-network), and any related medications. If there are complications that require additional procedures or a longer hospital stay, those are covered under your plan as well.

Postpartum Care

Coverage does not end the moment the baby is born. Postpartum care includes follow-up visits for the mother, medications related to recovery, and mental health support. Postpartum depression affects roughly one in five women, and quality maternity care health insurance should provide access to mental health professionals, postpartum screenings, and therapy or medication if needed.

Newborn Care

Your newborn is covered from the moment of birth for initial hospital care, routine screenings, vaccinations, and early pediatric visits. If your baby requires a NICU stay or other specialized care after birth, that is covered under general medical benefits as a separate person on your policy. You generally have 60 days after the birth to formally add your baby to your plan.

Breastfeeding Support

ACA plans are required to cover breastfeeding support at no additional cost. This includes lactation consultations, counseling, and a breast pump. Your plan typically covers one dual-suction electric breast pump with a prescription, purchased from an in-network provider.

What Is Not Covered Under Maternity Care Health Insurance?

Even with solid maternity care health insurance, there are things you may still need to pay for out of pocket. Here are some common gaps:

- Out-of-network providers: If your OB, anesthesiologist, or hospital is not in your plan’s network, you may face significantly higher costs or full price

- Elective procedures not medically necessary: Some cosmetic or elective procedures related to pregnancy may not be covered

- Certain fertility treatments leading to the pregnancy: IVF and assisted reproduction are generally not part of standard maternity coverage

- Doula services: Increasingly popular, but coverage varies widely by plan. Some insurers now include doula support up to a set dollar amount

- Private hospital rooms: Upgrades beyond standard accommodation are typically not covered

Knowing these gaps ahead of time helps you plan financially and avoid surprise bills.

Types of Plans That Include Maternity Care Health Insurance

ACA Marketplace Plans

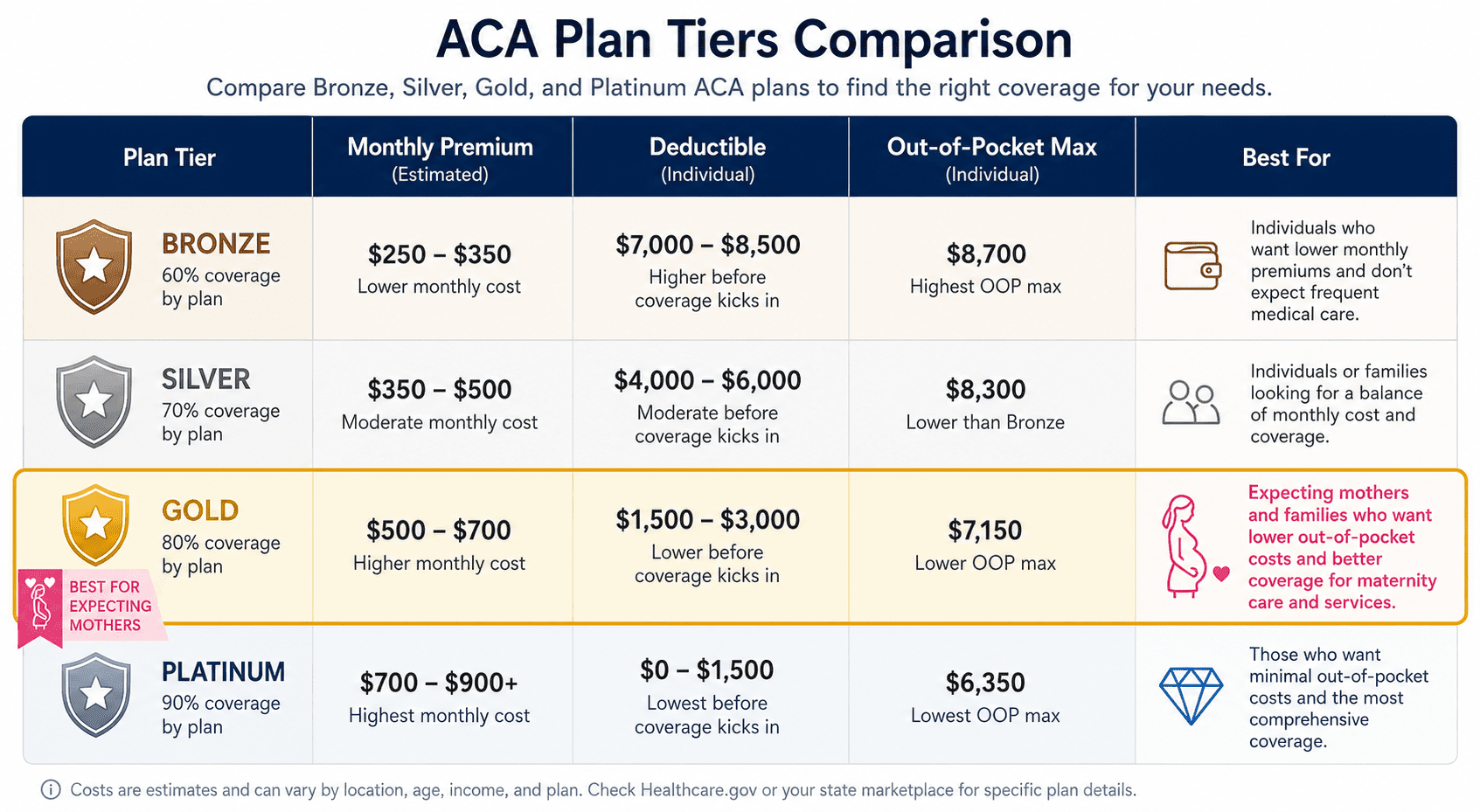

All plans sold through the Health Insurance Marketplace include maternity coverage as a required essential health benefit. These plans are available at four metal tiers: Bronze, Silver, Gold, and Platinum. Bronze plans have lower monthly premiums but higher deductibles. Platinum plans have higher premiums but lower out-of-pocket costs. For expecting parents, a Gold or Platinum plan often makes more financial sense because you know you will be using significant medical services throughout the year.

Employer-Sponsored Plans

If you get health insurance through work, your employer-sponsored plan is required to include maternity coverage if it is an ACA-compliant plan. Employer plans often have lower premiums because your employer pays a portion of the cost. Check whether your preferred OB and hospital are in the plan’s network before relying on it for your pregnancy care.

Medicaid and CHIP

For those who qualify based on income, Medicaid provides comprehensive maternity care health insurance at little to no cost. Coverage includes prenatal visits, labor and delivery, and postpartum care. As of 2025, 47 states and Washington D.C. have extended Medicaid postpartum coverage to 12 months after delivery, meaning you stay covered for a full year after your baby is born. If you give birth while on Medicaid, your newborn is automatically enrolled and remains eligible for at least one year.

ICHRA and Employer Reimbursement Arrangements

If your employer uses an Individual Coverage Health Reimbursement Arrangement, you can use those tax-free funds to purchase your own individual health plan through the Marketplace. Since all Marketplace plans include maternity coverage, this approach gives you flexibility while ensuring you are covered.

How to Choose the Right Maternity Care Health Insurance Plan

With so many options out there, picking the right plan for your pregnancy does not have to be complicated. Focus on these key factors:

Check Network Coverage First

Before anything else, make sure your OB-GYN, midwife, and preferred hospital are in the plan’s network. Out-of-network costs can be dramatically higher, and you do not want to discover mid-pregnancy that your doctor does not accept your insurance.

Calculate Total Costs, Not Just Premiums

A lower monthly premium can be tempting, but if a plan has a $5,000 deductible, you will pay that entire deductible before coverage kicks in on most services. For a planned pregnancy, add up the expected premium costs plus your deductible plus estimated out-of-pocket costs. That total often tells a very different story than the monthly premium alone.

Look at the Out-of-Pocket Maximum

Your out-of-pocket maximum is the most you will have to pay in a year before your insurance covers 100 percent of costs. For maternity care, this number matters a lot. A plan with a $3,000 out-of-pocket max is going to protect you better than one with a $9,000 cap.

Review Mental Health Coverage

Postpartum mental health is real and it matters. Make sure your plan covers therapy, psychiatric visits, and postpartum depression screenings. Some plans now specifically include postpartum depression treatment as a covered benefit.

Look for Telehealth Options

Telehealth for prenatal and postpartum care has become much more common and convenient. If your plan includes robust telehealth, you can address a lot of routine questions and concerns without leaving home, which is a genuine quality-of-life improvement during pregnancy and early parenthood.

When to Enroll in Maternity Care Health Insurance

Timing matters. If you are already pregnant, you may still be able to enroll in a plan:

- During Open Enrollment (typically November 1 through January 15 for federal marketplace plans)

- During a Special Enrollment Period if you have a qualifying life event such as losing other coverage or getting married

- In Medicaid or CHIP at any time of the year if you meet income requirements

If you are planning to become pregnant but have not yet, enroll during Open Enrollment before the pregnancy begins if possible. Pregnancy itself is not a qualifying life event that triggers a Special Enrollment Period, so if you become pregnant outside of Open Enrollment, you may be stuck with whatever plan you already have until the next enrollment window.

Costs You Should Plan For Even With Coverage

Even with strong maternity care health insurance, there are predictable out-of-pocket costs to prepare for. Setting money aside in an HSA or FSA can help cover these:

- Your annual deductible, which may apply to labor and delivery costs

- Copays for prenatal visits after your plan’s preventive care threshold

- Prescription costs for prenatal vitamins not covered by your plan

- Costs for out-of-network providers if your preferred doctor is not in the network

- Newborn’s own deductible and out-of-pocket costs once added to the plan

- Childcare costs after maternity leave ends

Final Thoughts

Maternity care health insurance is one of the most important financial tools you will use during one of the most meaningful times in your life. The right plan can mean the difference between a manageable experience and a financial setback that takes years to recover from.

Take the time to compare your options. Look beyond the premium. Think about your specific providers and your expected healthcare needs over the course of the pregnancy. And if you qualify for Medicaid or premium tax credits through the Marketplace, use them. They exist precisely for situations like this.

Fiscible.com helps you make sense of your financial decisions, including the big ones. Explore our health insurance guides to find the coverage that fits your life.