When most people shop for health insurance, they focus on premiums, deductibles, and copays. What many do not realize is that where they live might matter just as much as any of those numbers. State-specific insurance rules, programs, and marketplace options can completely change what you have access to, what you pay for it, and how much protection you actually get.

Two people with the same income, the same health status, and the same family size could end up with wildly different health insurance experiences simply because one lives in Massachusetts and the other lives in Mississippi. That is the reality of health insurance in the United States, and understanding it can save you real money and real headaches.

This guide explains how state-specific insurance works, what varies from state to state, and how to use that knowledge to your advantage no matter where you live.

How the Federal Government and States Share Control of Health Insurance

Health insurance in the US is a mix of federal rules and state-level flexibility. The Affordable Care Act sets a federal baseline: all individual and small-group plans must cover ten essential health benefits, cannot deny coverage for pre-existing conditions, and must follow specific cost-sharing rules. But beyond that baseline, states have a significant amount of control.

States can expand Medicaid, run their own insurance marketplaces, add coverage requirements beyond federal minimums, set their own premium rate review processes, and even create individual mandates that require residents to have coverage. This combination of federal standards and state discretion is why state-specific insurance options look so different depending on where you are.

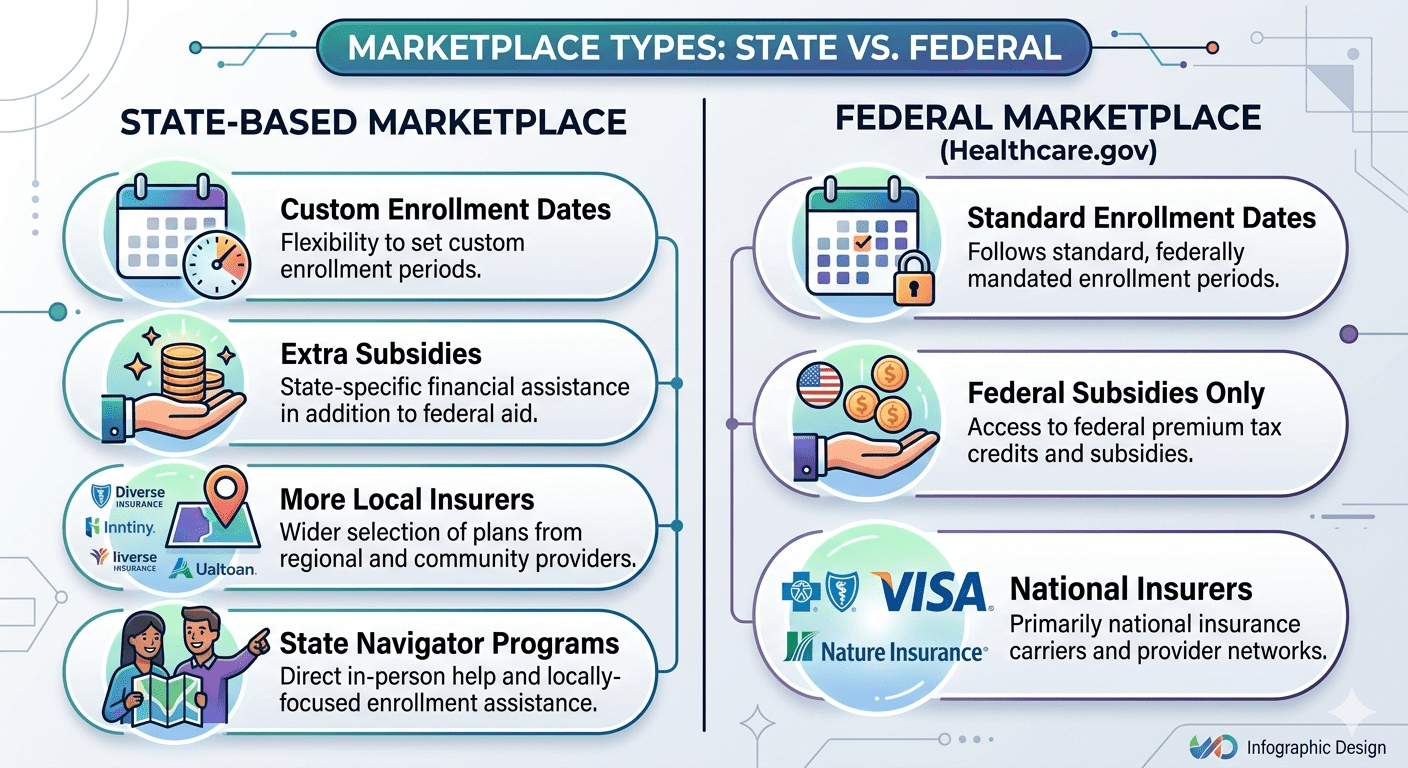

State-Run vs. Federal Insurance Marketplaces

One of the most significant differences between states is how they run their health insurance marketplace. As of 2025, 21 states and Washington D.C. have their own fully state-based marketplaces. These states have enrollment websites, set their own enrollment schedules, fund their own navigator programs, and in some cases offer additional state-funded subsidies that go beyond what the federal government provides.

The remaining states use the federal Health Insurance Marketplace at Healthcare.gov. These states still follow ACA rules, but they have less flexibility to customize the experience or add extra financial assistance for residents.

Why does this matter? State-run marketplaces often have more plan options from more insurers, better customer service infrastructure, and in some states, enhanced subsidies that make coverage more affordable than what is available on the federal exchange. If you live in a state like California, New York, or Colorado, you may have access to resources and pricing that simply are not available to people in states using Healthcare.gov.

Medicaid Expansion: One of the Biggest State-Specific Differences

Medicaid expansion is one of the most consequential state-level decisions in health insurance, and not all states have made the same choice. Under the ACA, the federal government gave states the option to expand Medicaid eligibility to adults with incomes up to 138 percent of the federal poverty level. Most states took that option. But as of 2025, a handful have not.

In states that have expanded Medicaid, low-income adults have access to free or very low-cost comprehensive coverage that includes doctor visits, hospital care, mental health services, prescription drugs, and maternity care. In states that have not expanded Medicaid, adults who do not meet traditional Medicaid eligibility requirements and who earn too little to qualify for ACA subsidies can fall into what is known as the coverage gap. They earn too much for traditional Medicaid but too little to get subsidized Marketplace coverage.

If you are near the lower end of the income spectrum, checking whether your state has expanded Medicaid is one of the first things you should do when shopping for state-specific insurance.

State Insurance Mandates and Extra Coverage Requirements

Some states go above and beyond federal requirements when it comes to what health insurance must cover. These state-specific insurance mandates vary widely and can significantly affect the value of the plans available to you.

Individual Mandates

After the federal individual mandate penalty was eliminated in 2019, several states implemented their own. As of 2025, California, Massachusetts, New Jersey, Rhode Island, and Washington D.C. have individual mandates that require residents to have health insurance or pay a state tax penalty. Vermont also has a mandate but no financial penalty. If you live in one of these states, having coverage is not just smart financially, it is legally required.

Enhanced Essential Health Benefits

States can also require plans to cover additional services beyond the federal ten essential health benefits. For example, some states require coverage for infertility treatments, more expansive mental health benefits, hearing aids, or specific cancer screenings. These state-specific insurance requirements make plans in those states more comprehensive than the federal minimum.

Mental Health and Substance Use Parity

While federal law requires mental health parity, some states enforce stricter rules and monitor compliance more aggressively. In these states, you are more likely to find plans that genuinely treat mental health services on par with physical health in practice, not just on paper.

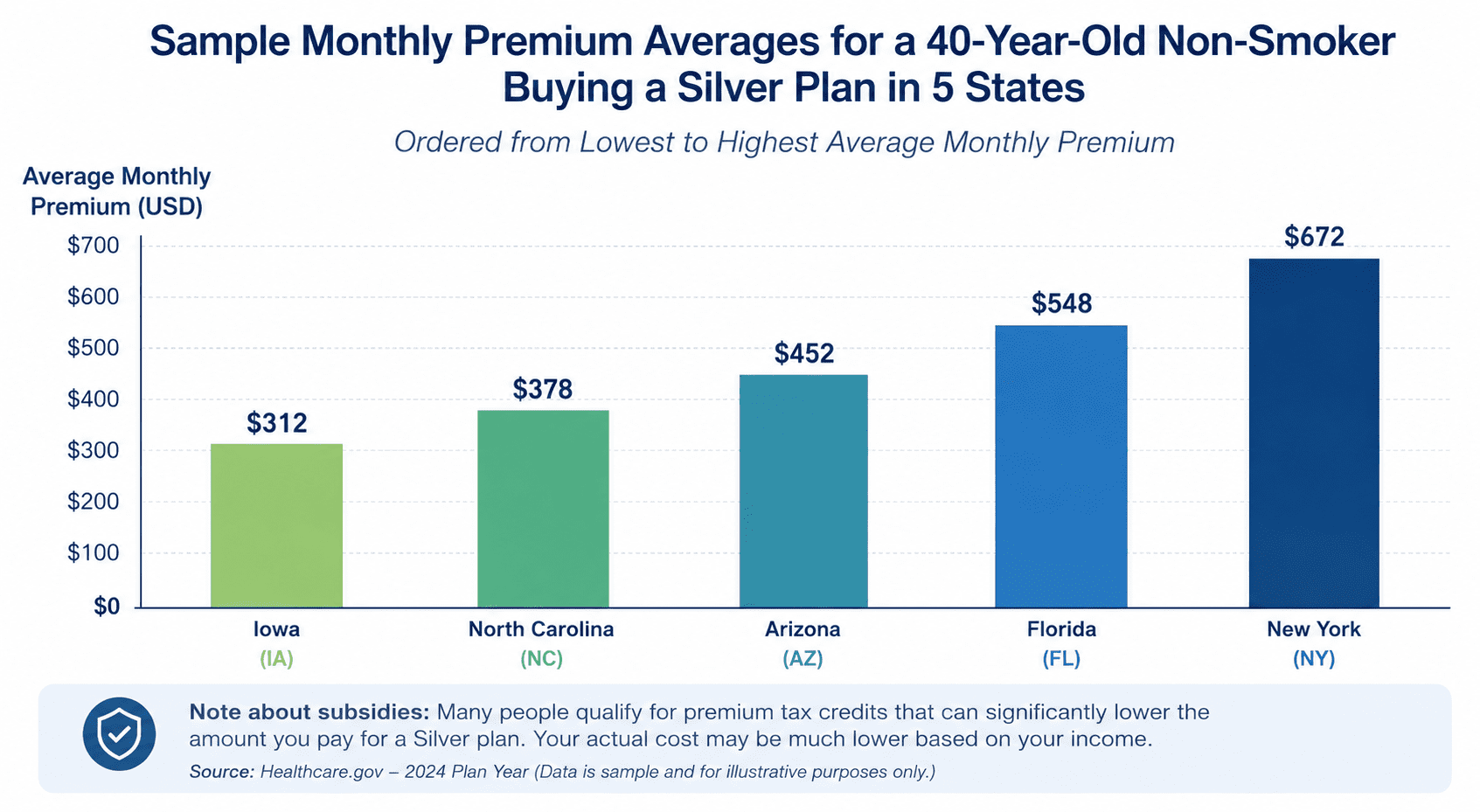

How Premium Costs Vary by State

Even if two people buy the same tier of ACA plan, a Silver plan in one state can cost dramatically more or less than a Silver plan in another state. Several factors drive these differences:

- Local healthcare costs and provider prices

- The number of insurers competing in that state’s marketplace

- The health status of the state’s overall insured population

- How aggressively the state reviews and negotiates insurer rate filings

- State regulations that affect how insurers can price their products

Premium increases for 2026 have been particularly uneven across states. The median proposed increase is 18 percent nationally, but some states are seeing proposed hikes of 20 percent or more while others have seen much smaller increases. States with active rate review programs and strong marketplace competition tend to see lower increases.

This is one more reason why the state-specific insurance landscape matters. If you have flexibility in where you live, such as working remotely, the cost of health insurance in different states can be a meaningful factor in your decision.

State-Specific Programs Beyond the Marketplace

Beyond Medicaid and the Marketplace, many states have developed their own programs to fill gaps in coverage or improve affordability. Here are some examples of the kind of state-specific insurance initiatives you might find:

Basic Health Programs

A handful of states have created Basic Health Programs under the ACA that offer lower-cost coverage to residents who earn just above the Medicaid threshold. New York and Minnesota have the most established versions of this program. It essentially extends affordability further up the income scale.

State Reinsurance Programs

Some states have used a federal waiver to implement reinsurance programs, where the state helps cover insurers’s costs for the most expensive patients. This brings down premiums for everyone in that state’s marketplace. Alaska, Colorado, and several other states have successfully used this approach to keep premium growth in check.

State-Funded Subsidies

Certain states offer additional financial assistance for health insurance on top of federal premium tax credits. California, for example, provides state subsidies that extend financial help to residents at higher income levels than the federal program covers alone. If you are in a state with these extra subsidies, you may qualify for help even if you have been told you do not qualify federally.

Why Your State Matters When You Move

If you are moving to a new state, your health insurance situation may change significantly even if you have the same income and health status. Here is what to watch for:

- Your current plan likely does not follow you to a new state. You will need to re-enroll.

- Moving is a qualifying life event that triggers a Special Enrollment Period, giving you 60 days to get new coverage.

- Medicaid eligibility, which is state-administered, requires re-application in your new state.

- The available insurers, plan types, and network options in your new state may look very different from what you had before.

- If your new state has an individual mandate and your old one did not, you need to get covered quickly to avoid a penalty.

Taking the time to research state-specific insurance options before you move, rather than after, can help you avoid a gap in coverage and make better decisions about timing.

How to Find the Best State-Specific Insurance for Your Situation

Navigating state-specific insurance does not have to be complicated. Here is a straightforward approach:

Step 1: Start With Your State’s Marketplace

If your state has its own marketplace, start there. Go directly to your state’s enrollment website rather than Healthcare.gov, because state-specific resources, plans, and subsidy calculators will be more relevant.

Step 2: Check Medicaid Eligibility

Before looking at private plans, check whether you qualify for Medicaid in your state. If you do, it is almost always the most cost-effective option.

Step 3: Use a Subsidy Calculator

Your eligibility for federal premium tax credits depends on your income relative to the federal poverty level. A subsidy calculator at Healthcare.gov or your state’s marketplace can quickly tell you whether you qualify and how much help you might get.

Step 4: Compare Plans With Your Actual Needs in Mind

Look at the total cost picture, not just the premium. A plan with lower premiums but a very high deductible may not be the best deal if you expect to use your insurance regularly. Also check that your preferred doctors and hospitals are in-network.

Step 5: Ask About State-Specific Programs

Contact your state insurance department or a local navigator to ask about state-funded programs, reinsurance, or additional subsidies you may not know about. These programs exist to help people find affordable coverage, and many eligible residents never take advantage of them because they are not aware they exist.

The Bottom Line on State-Specific Insurance

Health insurance in the United States is not a single unified system. It is a patchwork of federal rules and state choices that creates dramatically different environments depending on where you live. State-specific insurance options, programs, mandates, and marketplace structures can affect your premiums, your access to care, your eligibility for financial help, and even whether you are legally required to have coverage at all.

Understanding your state’s specific landscape is not optional if you want to get the most out of your health insurance. It is one of the most practical things you can do to protect both your health and your finances.

Whether you are shopping for coverage for the first time, switching plans during Open Enrollment, or moving to a new state, take the time to learn what your state offers. The differences are real, and they can add up to hundreds or even thousands of dollars a year.

Fiscible.com helps you navigate the complex world of personal finance and insurance. Explore our resources to find the coverage that works for where you are and where you are going.