Wondering if Ambetter insurance is right for you? This guide covers plans, costs, eligibility, and how to enroll, so you can choose with confidence.

Ambetter Insurance: Plans, Costs, and How to Enroll

Picking a health insurance plan feels complicated until you understand what you are actually comparing. Ambetter insurance is one of the most widely available marketplace options in the US, offered through Centene Corporation across more than 30 states.

This guide breaks down how Ambetter plans work, what they cost, who qualifies, and what real enrollees should watch out for before signing up. By the end, you will know exactly whether Ambetter fits your situation.

What Is Ambetter Insurance?

Ambetter is a health insurance brand operated by Centene Corporation, one of the largest managed care organizations in the United States. Ambetter plans are sold exclusively through the Health Insurance Marketplace, which means they are ACA-compliant and available during Open Enrollment or after qualifying life events.

Because Ambetter targets low-to-moderate income for individuals and families, many of its plans are priced to work well with premium tax credits. If you qualify for subsidies, your monthly cost can drop significantly.

Which States Offer Ambetter Plans?

Ambetter operates in over 30 states, including Texas, Georgia, Illinois, Indiana, Kentucky, Mississippi, Missouri, Nebraska, Nevada, New Hampshire, and others. Availability varies by county, so the first step is always checking the marketplace for your specific location.

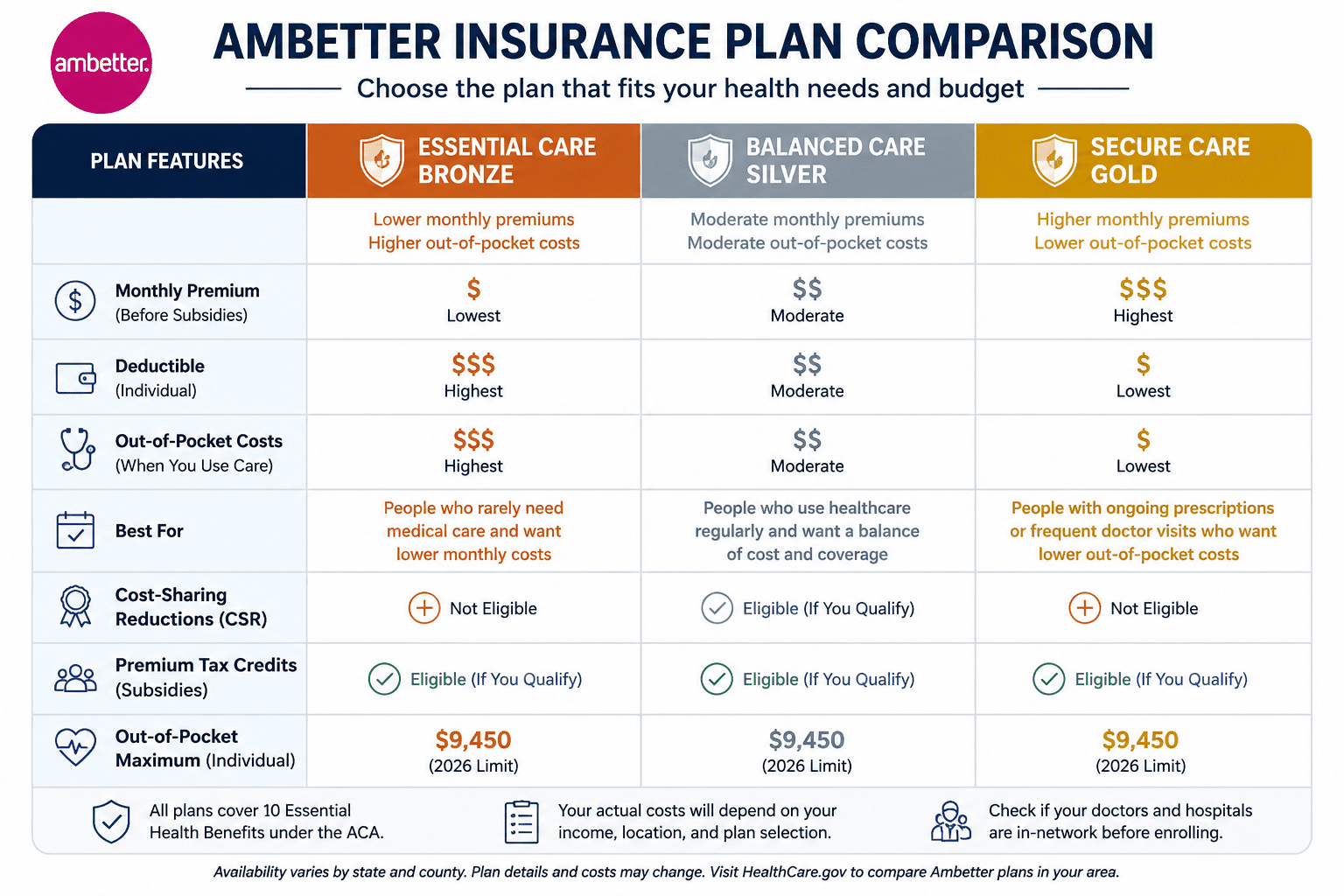

Ambetter Plan Tiers Explained

Ambetter offers plans across the standard ACA metal tiers. Each tier represents a different split between what you pay monthly versus what you pay when you actually use care.

Essential Care (Bronze)

- Lowest monthly premiums

- Higher deductibles and out-of-pocket costs when you use services

- Best for people who rarely need medical care and want low monthly costs

Balanced Care (Silver)

- Mid-range premiums

- Moderate deductibles

- The only tier eligible for cost-sharing reductions if your income qualifies

- Best for people who use healthcare regularly

Secure Care (Gold)

- Higher monthly premiums

- Lower out-of-pocket costs per visit or procedure

- Best for people with ongoing prescriptions or frequent doctor visits

How Much Does Ambetter Insurance Cost?

Ambetter premiums vary by state, age, household income, and plan tier. A 30-year-old in Texas might pay $180-$280 per month for a Silver plan before subsidies. With a premium tax credit, that cost can fall to $0-$80 per month depending on income.

Key cost factors to compare before enrolling:

- Monthly premium

- Annual deductible

- Copays and coinsurance per visit

- Out-of-pocket maximum

- Whether your current doctors are in network

Does Ambetter Qualify for Subsidies?

Yes. Since Ambetter plans are sold on the ACA marketplace, you can apply any premium tax credits you qualify for. If your household income falls between 100% and 400% of the federal poverty level, you likely qualify for subsidies that reduce your monthly premium.

Ambetter Network and Coverage

Ambetter uses a managed care model, which means you typically need to use in-network providers to get the lowest costs. Before enrolling, check whether your primary care doctor, any specialists you see, and your preferred hospital are in the Ambetter network for your plan.

What Does Ambetter Cover?

All Ambetter plans include the ten essential health benefits required under the ACA:

- Preventive care and wellness visits

- Prescription drug coverage

- Emergency services

- Hospitalization

- Mental health and substance use treatment

- Maternity and newborn care

- Pediatric services

- Lab tests

- Outpatient care

- Rehabilitative services

My Health Pays Rewards Program

Ambetter includes a rewards program where members earn points for completing health-related activities like annual checkups, diabetes management, or filling out health assessments. Points can be redeemed for rewards that offset out-of-pocket costs. It is a small but useful feature for active members.

How to Enroll in Ambetter Insurance

- Go to HealthCare.gov or your state’s marketplace during Open Enrollment (November 1 – January 15 in most states)

- Enter your household information to check subsidy eligibility

- Compare available plans in your county

- Select an Ambetter plan and complete enrollment

- Pay your first premium to activate coverage

If you miss Open Enrollment, you can enroll outside this window only if you have a qualifying life event such as losing other coverage, getting married, or having a baby.

Ambetter Insurance – Common Complaints and What to Know

Ambetter consistently receives mixed reviews. Lower-income enrollees who receive strong subsidies often rate the value highly. Complaints tend to center on narrow provider networks, prior to authorization requirements for certain procedures, and customer service responsiveness.

Before enrolling, verify:

- Your preferred providers are in network

- Your regular prescriptions are on the Ambetter formulary

- You understand prior authorization requirements for any ongoing treatments

Is Ambetter Insurance Worth It?

For subsidy-eligible individuals and families who primarily need basic healthcare coverage and preventive care, Ambetter can be an excellent value. For people with complex medical needs, frequent specialist visits, or strong preferences about providers, it is worth carefully checking the network before committing.

Ambetter is not the right fit for everyone, but it is a legitimate, ACA-compliant option that works well for a large portion of the marketplace’s population.

Conclusion

Ambetter insurance offers solid ACA marketplace coverage across more than 30 states, with plan tiers ranging from low-premium Bronze to lower-deductible Gold options. The key to getting value from an Ambetter plan is understanding the network, verifying your providers are covered, and applying any subsidies you qualify for.

Ready to see what Ambetter costs in your area? Visit HealthCare.gov during Open Enrollment to compare plans and check your subsidy eligibility before the deadline.

To know more about insurance debts, check out this article.

One thought on “AMBETTER INSURANCE: EXCLUSIVE WHAT YOU NEED TO KNOW IN 2026”