Master your finances with proven smart money tips. Learn budgeting, savings, investing, and debt payoff strategies that work for every income level.

Money struggles don’t start because people are bad at math. They start because nobody teaches you the foundations early enough. By the time most people face a financial crisis, they’ve already lost years they could have spent building wealth.

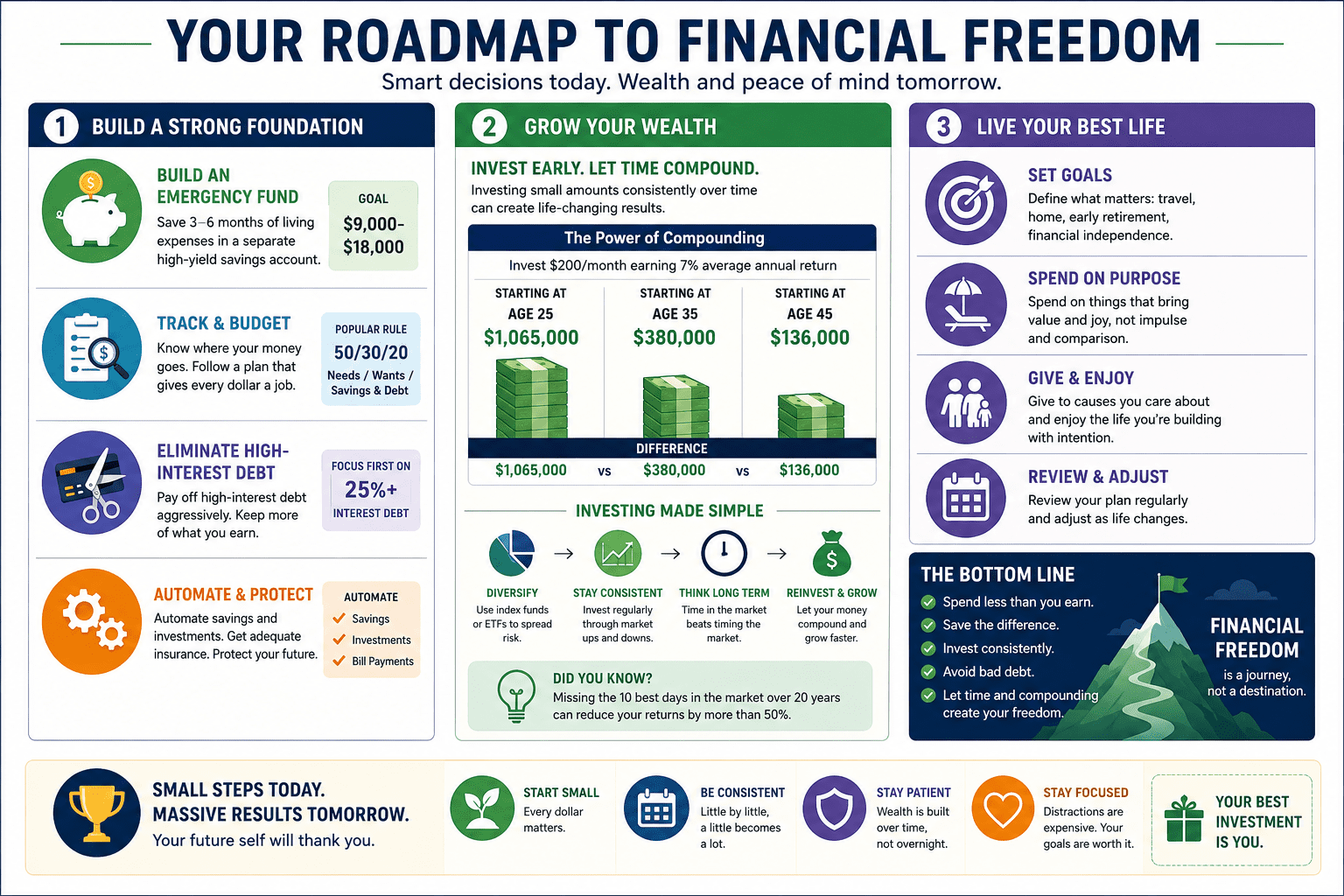

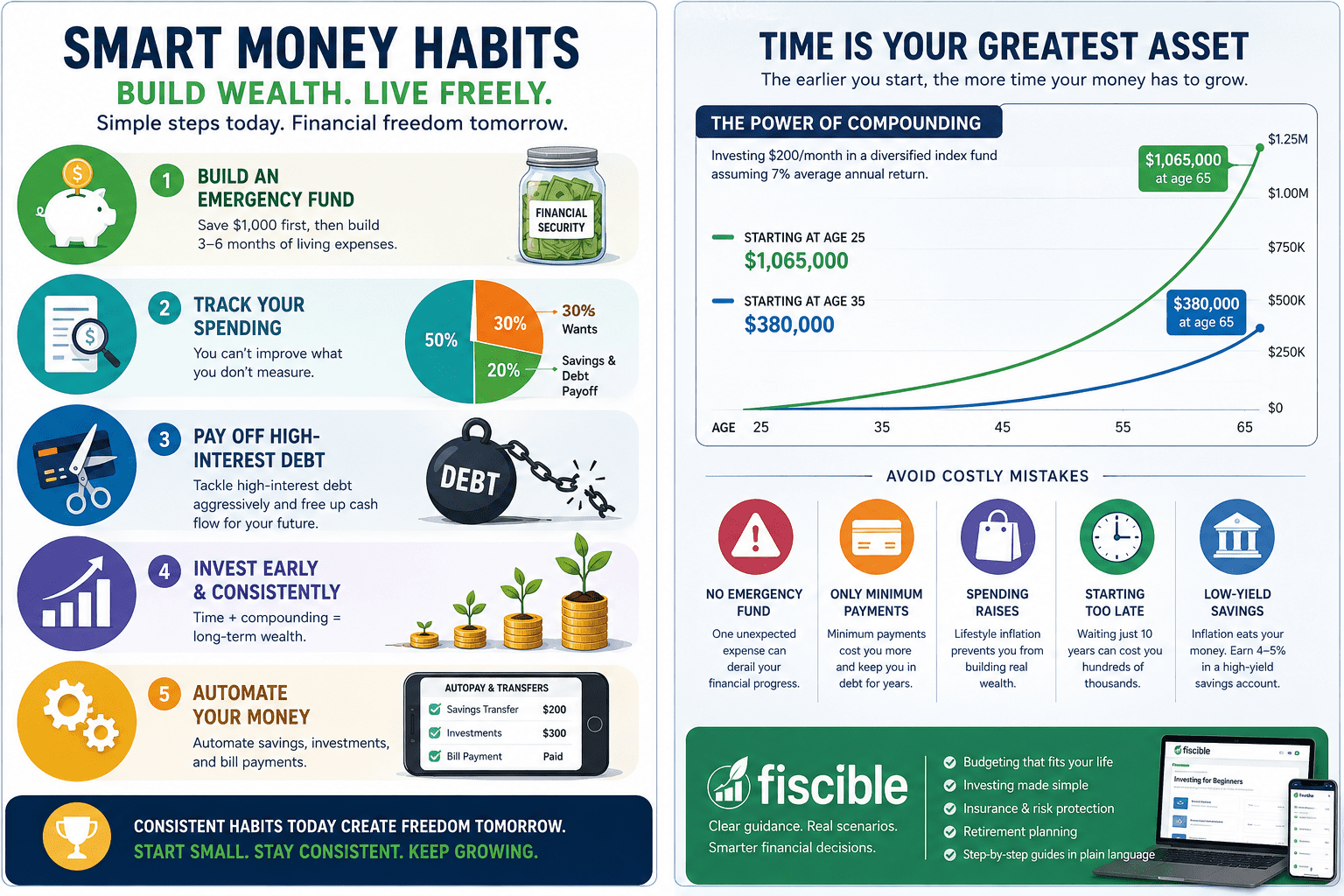

The good news: smart money tips aren’t complicated. They’re simple habits that compound over time. Whether you’re earning $40,000 or $400,000, the same principles apply. Build an emergency fund, track spending, eliminate debt, invest early, and let time do the work.

Why smart money tips help management matters

Less than 50% of Americans can cover a $1,000 emergency without savings. That statistic isn’t about income-it’s about awareness. People know they should save, but they don’t know where to start.

The other challenge is invisible: Americans carry over $1.2 trillion in credit card debt, much of it at 25%+ annual interest rates. That’s money flowing out of your hands and into bank profits instead of building your future.

The difference between someone who’s wealthy and someone who isn’t often comes down to one thing: starting early. Someone who invests $200/month at age 25 can accumulate over six figures by retirement through compounding alone. Wait until age 35, and you’ve lost a decade of growth that no amount of catch-up saves you.

Smart money tips you can implement right now

Build an emergency fund first using smart money tips

This is non-negotiable. An emergency fund isn’t about being pessimistic-it’s about being prepared. When an unexpected expense hits without a cushion, people turn to credit cards or high-interest loans, and suddenly you’re paying interest on something you couldn’t afford in the first place.

Start small if you need to. Your first goal is $1,000. That covers most car repairs, medical bills, or sudden expenses without debt. Once you hit $1,000, expand to 3-6 months of living expenses (about $9,000-$18,000 for the average household).

Keep this money in a separate high-yield savings account, not your checking account. You won’t see it every day, and it earns 4-5% interest instead of the <1% big banks offer.

Track your spending ruthlessly

You can’t fix what you don’t measure. Most people guess at their spending and are usually way off.

Spend one week writing down everything you spend money on. Coffee, lunch, subscriptions, gas, groceries, all of it. At the end of the week, you’ll see patterns you didn’t notice. Many people discover they’re spending $200-300/month on subscriptions they forgot they had, or eating out far more than they realize.

The 50/30/20 budgeting rule is a good starting point: 50% of after-tax income on needs (housing, food, utilities), 30% on wants (dining, entertainment, hobbies), and 20% on savings and debt payoff. If those percentages don’t match your life, adjust them. The key is visibility and intention.

Pay off high-interest debt aggressively

Credit card debt at 25% interest is wealth-destroying. If you owe $5,000 on a card at that rate and pay the minimum, you’ll pay thousands more in interest and take years to clear it.

Two strategies work: the avalanche method (pay off highest-interest debt first to save money) or the snowball method (pay off smallest balances first for psychological wins). Most people stick longer with the snowball because seeing wins builds momentum.

Beyond credit cards, consider refinancing student loans if interest rates have dropped or your income has increased. Even a 1-2% rate reduction saves tens of thousands over 10 years.

Start investing earlier than feels comfortable

One Reddit user in r/personalfinance put it simply: “Investing feels risky until you realize not investing is riskier.” Inflation eats away at savings sitting in low-interest accounts.

You don’t need to pick individual stocks. Index funds and ETFs are designed for beginners: you buy a fund that holds hundreds of companies, your money is diversified, and you benefit from market growth without needing expertise just using smart money tips.

If your employer offers a 401(k) match, contribute enough to get the full match. That’s free money with an immediate 50-100% return.

Automate everything you can

Automation removes willpower from the equation. You can’t spend money if it’s already in savings before you see it.

Set up automatic transfers to savings the day after payday. If you earn a raise, increase the automatic transfer instead of spending the extra money. Automate credit card payments so you never miss a due date or rack up interest.

Automation makes consistency effortless and smart money tips efficient.

Money mistakes everyone makes at least once

Nearly everyone misses something on their financial journey. The goal is to avoid the mistakes that cost the most time and money. To successfully implement smart money tips you need to identify:

The biggest ones:

- Neglecting an emergency fund. The first unexpected $2,000 expense you face without savings sends you backward fast.

- Only making minimum payments on debt. Minimum payments extend debt for decades and triple the total cost.

- Spending raises instead of saving them. When your income goes up, send half the increase to savings or investments before you get used to spending it.

- Starting retirement savings at 45 instead of 25. Time is your most valuable asset in investing. Starting late means working longer.

- Keeping money in low-interest accounts. Savings accounts earning <1% lose purchasing power to inflation. Move it to a high-yield account earning 4-5%.

Try Fiscible

Building smart money habits takes focus and the right tools. Fiscible breaks down personal finance topics that most people find overwhelming, from budgeting and investing to insurance and retirement planning. to smart money tips.Their guides walk you through real scenarios step-by-step in plain language, so you actually understand what you’re doing with your money instead of just following rules.

Whether you’re starting from zero or optimizing an existing plan, smart money tips are built for people who want clear, actionable advice without the jargon or sales pitch.