A breakdown of how 401k contributions reduce your take-home pay and why the math isn’t what you’d expect.

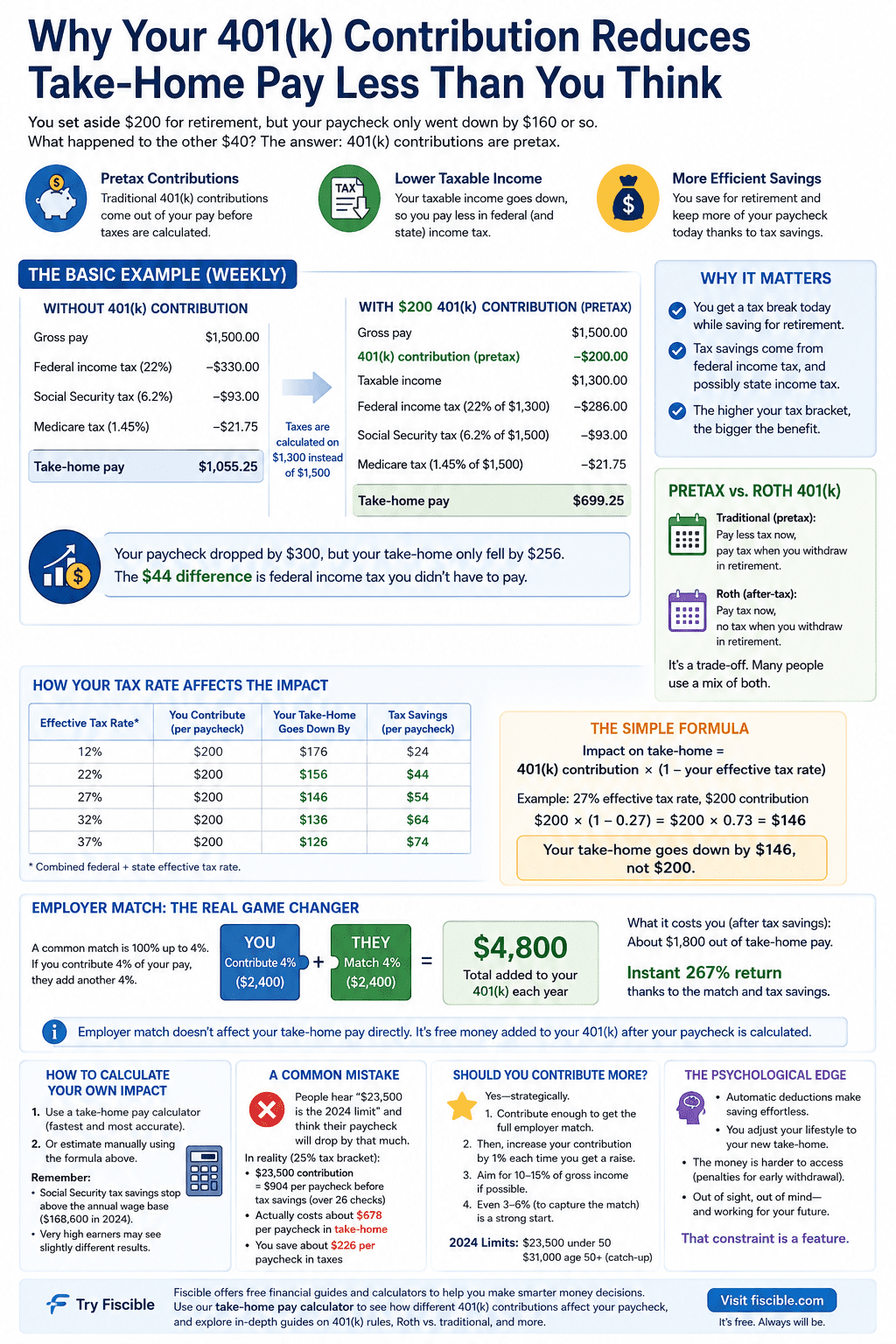

If you’ve ever looked at your paycheck after signing up for a 401k, you’ve probably noticed something confusing: the reduction in take-home pay doesn’t match the contribution amount. You might have set aside $200 for retirement, but your actual paycheck only went down by $160 or so. What happened to the other $40?

The answer is that 401k contributions work differently than most deductions, and understanding that difference can completely change how you think about retirement savings. Let’s break it down.

The basic math: pretax vs. gross pay

When you contribute to a traditional 401k, the contribution comes out of your pay before taxes are calculated. That’s the key phrase: pretax. Your employer sends that $200 straight to your 401k account, but your taxable income for the year goes down by that same amount.

Here’s why that matters. If you earn $60,000 a year and contribute $3,000 to your 401k, your taxable income becomes

$57,000, not $60,000. Taxes are calculated on the smaller number. Over the course of a year, contributing to your 401k directly reduces the amount of federal income tax you owe.

Let’s walk through a real example. Say you’re paid weekly and your gross paycheck is $1,500. Here’s what might happen without a 401k contribution:

Gross pay: $1,500

Federal income tax (at 22% bracket): $330 Social Security tax (6.2%): $93

Medicare tax (1.45%): $21.75

Take-home pay: $1,055.25

Now, you decide to contribute $200 per week to your 401k. That $200 reduces your taxable income before taxes are withheld. So your employer calculates taxes on $1,300, not $1,500:

Gross pay: $1,500

401k contribution (pretax): $200

Taxable income: $1,300

Federal income tax (at 22% bracket): $286

Social Security tax (6.2% on $1,500): $93

Medicare tax (1.45% on $1,500): $21.75

Take-home pay: $699.25

In this example, your paycheck dropped by $300, but your take-home only fell by $256. That $44 difference is the federal income tax you didn’t have to pay because your 401k contribution reduced your taxable income.

Why this matters

The tax savings on 401k contributions is one of the biggest reasons financial planners recommend them. You get to save for retirement while paying less in taxes right now. It’s not free money, but it’s a meaningful benefit that many people miss.

The math gets even better if you live in a state with income tax. New York, California, and other high-tax states will also reduce your state income tax based on 401k contributions. If you’re in a 32% combined federal and state tax bracket, that

$200 contribution only reduces your take-home by about $136. You’re effectively paying $64 less out of your own pocket to save $200 for retirement.

Roth 401k changes the equation

Some employers offer a Roth 401k option instead of (or in addition to) traditional 401k. A Roth 401k works differently.

Contributions are made after taxes, not before. Your taxable income doesn’t go down.

Using the same example: if you contribute $200 per week to a Roth 401k, your paycheck still takes a $200 hit, but you don’t get the tax break now. Instead, when you withdraw that money in retirement, you won’t owe any taxes on it. This is a tradeoff: pay taxes now, no taxes later.

For someone in a lower tax bracket right now who expects to be in a higher bracket in retirement, Roth can make sense. For someone in a high bracket now who expects to be in a lower bracket in retirement, traditional is usually better. Most people don’t know which they’ll be, so they do a mix of both.

Employer match complicates things

Many employers offer to match your 401k contribution. A common match is 100% up to 3% or 4%, meaning if you contribute 4% of your pay, they add another 4%.

Here’s the important part: employer match doesn’t directly affect your take-home pay. It’s free money added to your 401k account after your paycheck is calculated. If your employer matches up to 4%, you should almost always contribute at least 4% yourself, because you’re immediately doubling your money.

Let’s say you earn $60,000 a year. Contributing 4% ($2,400) costs you roughly $1,800 in take-home pay after tax savings. Your employer adds another $2,400 as a match. You’ve just added $4,800 to retirement savings while only reducing take-home by $1,800. That’s an instant 267% return, thanks to the combination of the employer match and tax savings.

How to calculate your own take-home impact

The simple way is to use a take-home pay 401k calculator. Most payroll services and financial websites have them. You plug in your gross salary, contribution amount, tax bracket, and state, and it shows you the impact.

If you want to estimate manually, here’s the formula:

Impact on take-home = (401k contribution) × (1 – your effective tax rate)

If you’re in the 22% federal bracket with 5% state tax (27% total), and you contribute $200:

Impact = $200 × (1 – 0.27) = $200 × 0.73 = $146

Your take-home goes down by $146, not $200.

One caveat: this assumes all of your contribution comes out of federal and state taxable income. If you hit the Social Security wage base limit (earnings above $168,600 in 2024, adjusted yearly), 401k contributions stop reducing Social Security tax. Also, very high earners phase out from certain tax benefits, which can change the math slightly.

A common mistake: assuming contributions hit take-home directly

Many people hear “I can contribute $23,500 to my 401k” (the 2024 limit) and assume their paycheck will drop by that amount. In reality, the after-tax cost is much lower.

If you spread $23,500 across 26 paychecks, that’s $904 per paycheck before tax savings. If you’re in a 25% effective tax bracket, it actually costs you about $678 per paycheck in take-home pay. You’re saving $226 per paycheck in taxes.

Over a year, that’s $5,876 in actual take-home reduction to save $23,500 for retirement. That’s roughly a 4-to-1 leverage: you reduce your lifestyle spending by $5,876 to save $23,500 for retirement.

Should you contribute more if the tax savings are that good?

For most people, the answer is yes, but strategically. If your employer offers matching, contribute enough to get the full match first. Then, if you can afford it, increase your contribution by a percentage point each time you get a raise. This way, you’re not cutting your current spending, just directing a portion of new income to retirement.

The IRS limits how much you can contribute ($23,500 in 2024 for those under 50, $31,000 for those 50 and older), but for the vast majority of people, maxing out your 401k isn’t realistic or necessary. Aim for at least 10-15% of gross income if possible, but even 3-6% (enough to capture employer match) is a solid foundation.

Employer match is the real money move

Here’s what many people miss: the real value of a 401k isn’t the tax savings (though that’s nice). It’s the employer match. If your employer offers a match, that’s free money that only shows up if you contribute. There’s no reason not to capture that.

Some employers even allow you to contribute to a Roth 401k and still get a traditional match. Others let you contribute part of your match to Roth and part to traditional. Check with your HR or benefits team to see what options you have.

Capturing the full match should be non-negotiable; everything else is about optimizing your personal situation.

The psychological benefit

Beyond the math, there’s a psychological component to 401k contributions. Many people find it easier to save for retirement through automatic payroll deductions than to save manually. Your paycheck is smaller, so you adjust your budget accordingly. That “out of sight, out of mind” effect can be incredibly powerful for building long-term wealth.

Once the money is in a 401k, it’s harder to access (there are penalties for early withdrawal), which creates a forcing function. You can’t accidentally spend your retirement savings on a new laptop or a vacation. That constraint, which can feel restrictive, is actually a feature, not a bug.

Try Fiscible

If you’re just starting to think about retirement savings or want to brush up on the fundamentals, Fiscible has a full suite of free financial guides and calculators. Their take-home pay calculator lets you experiment with different contribution levels and see exactly how each impacts your paycheck, and they offer in-depth explanations of how 401k rules work.

One thought on “HOW 401k CONTRIBUTIONS AFFECT YOUR TAKE-HOME PAY”