The 50/30/20 budget rule is the easiest way to manage your money in 2026. This beginner-friendly guide breaks down exactly how it works, how to calculate your numbers, and how to adjust it for your real life.

Introduction

Most people know they should have a budget. They just have no idea where to start.

There are spreadsheets. There are apps. There are budgeting methods with names that sound more like accounting degrees than actual plans you would stick to. It is no wonder so many people look at their bank account on the last day of the month and wonder where all the money went.

The 50/30/20 budget rule is different. It is the one budgeting method that actually makes sense to someone who has never budgeted before. No complicated spreadsheets. No tracking every single coffee. Just three categories, one simple split, and a plan that works with your real life.

In 2026, with living costs still elevated and most households feeling some financial pressure, having a clear, repeatable system for your money is not optional anymore. It is necessary. And the 50/30/20 rule is the perfect place to start.

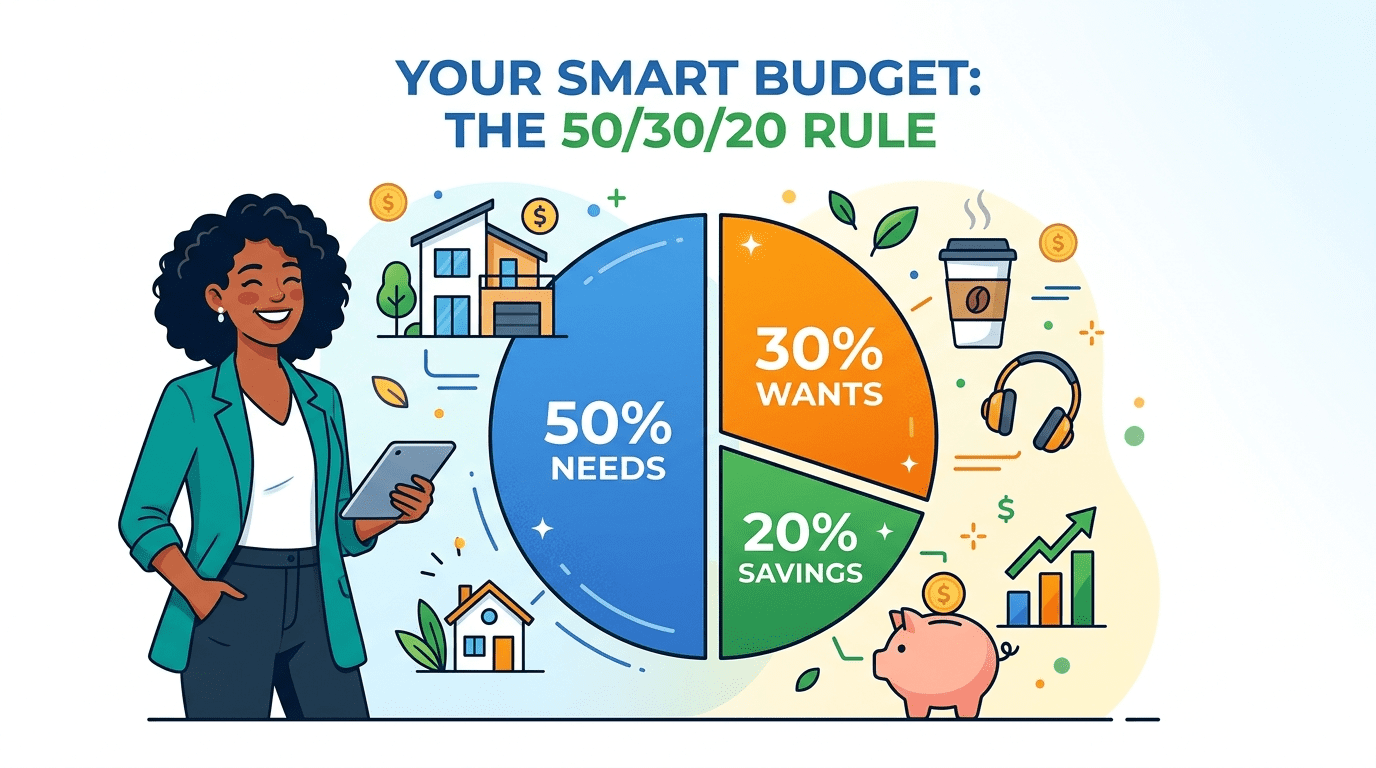

What Is the 50/30/20 Budget Rule?

The 50/30/20 budget rule is a personal budgeting framework that divides your after-tax income into three categories:

- 50% goes to Needs

- 30% goes to Wants

- 20% goes to Savings and Debt Repayment

That is it. Three buckets. Every dollar you bring home fits into one of them.

The rule was popularized by Senator Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan.” It was designed to give people a simple framework for managing money without requiring hours of detailed tracking every month.

The 50/30/20 budget rule works because it balances three things that a good budget needs to address: the things you must pay for, the things that make life worth living, and the financial foundation you are building for your future.

How to Calculate Your 50/30/20 Budget rule

Before you can apply the rule, you need one number: your monthly after-tax income.

This is your take-home pay. The money that actually lands in your bank account after taxes are taken out. If your employer also deducts things like health insurance or a 401k contribution, add those back in first. Those belong in your savings and needs categories, so they count separately.

If you are self-employed or have irregular income, use your average monthly income from the last three to six months as your baseline.

Quick Example:

Say your take-home pay is $4,000 per month.

- 50% for Needs = $2,000

- 30% for Wants = $1,200

- 20% for Savings = $800

Those three numbers are your monthly targets. Now let’s talk about what actually goes in each category.

The 50%: What Counts as a “Need”?

Needs are the expenses you cannot reasonably avoid. These are the things that keep your life functioning. If you stopped paying them, something would go seriously wrong.

Here is what belongs in the needs category:

- Rent or mortgage payments

- Groceries and basic food

- Utilities (electricity, water, gas, internet)

- Health insurance and essential medical costs

- Transportation (car payment, fuel, public transit)

- Minimum debt payments on student loans or credit cards

- Basic clothing

Needs are not always easy to define. The key question is: could you reasonably postpone or eliminate this expense without serious consequences? If the answer is no, it is a need.

One thing a lot of people get tripped up on: subscriptions and services that feel essential are not always needs. Your phone plan is a need. Netflix is not. Your gym membership because your doctor says you need exercise might be borderline, but a premium gym when a cheaper option exists is probably a want.

In 2026, housing alone takes up a huge portion of income for many people. The average American now spends around 34% of their take-home pay just on rent or mortgage. If your rent already eats 40% or more of your income, the 50/30/20 rule does not mean you are failing. It means you may need to adjust the percentages or make changes in other areas to bring your numbers back to a workable balance.

The 30%: What Counts as a “Want”?

Wants are the expenses that make your life enjoyable but that you could live without if you had to. This is not a judgment on whether these things have value. They do. The 30% category actually builds in room for them, which is one reason the 50/30/20 rule feels sustainable long-term.

Common wants include:

- Dining out and takeaway

- Entertainment (streaming services, concerts, movies)

- Hobbies and sports

- Travel and vacations

- Shopping for non-essential clothes or home items

- Gym memberships and wellness extras

- Subscriptions like Spotify, Amazon Prime, etc.

The 30% category is where most people overspend without realizing it. Small wants add up fast. Three streaming services, two food delivery orders a week, a gym membership you barely use, and a few impulse purchases can easily push you well past your 30% limit before the month is halfway through.

This does not mean you have to eliminate the things you enjoy. It means you are intentional about them. You pick what matters most, you budget for it, and you stop when you hit your limit.

The 20%: Savings and Debt Repayment

This is the most important category, and it is the one most people skip when money feels tight.

The 20% category covers:

- Emergency fund contributions

- Retirement savings (401k, IRA, Roth IRA)

- Extra debt payments beyond the minimums

- Investing

- Saving for specific goals like a house down payment or a new car

A lot of beginners think of savings as what is “left over” after everything else is paid. That is the wrong order. Savings should come first, before wants, and ideally as soon as your paycheck arrives. This is called paying yourself first, and it is one of the most effective financial habits you can build.

Even if you can only put $100 a month into savings right now, that is real progress. Small amounts invested consistently over time grow into something significant. The 50/30/20 rule builds savings into your budget by design, not as an afterthought.

What to Do When Your Numbers Don’t Fit the 50/30/20 Budget Rule

Here is an honest truth: for a lot of people in 2026, the 50/30/20 split does not work perfectly on the first try. Rent might be too high. Income might be too low. Debt might be eating a bigger share than expected. That does not mean the rule is broken. It means you need to adjust it for your reality.

A few common adjustments that work:

If your needs are over 50%: Try a 60/30/10 or a 70/20/10 split. The goal is still to have something going to savings, even if it is not 20% right now. Progress matters more than perfection.

If you have a lot of debt: Shift more of your 20% toward aggressive debt repayment. Once the high-interest debt is gone, redirect that money to savings and investing.

If you earn a high income: The 30% wants category can become too generous at higher income levels. Some high earners choose to follow a 50/20/30 reverse split, putting more into savings and less into lifestyle spending.

If you are in a high cost-of-living city: You may not be able to keep needs under 50% without moving or changing your housing situation. Be realistic. Track your actual numbers and adjust the percentages to reflect your real life.

The 50/30/20 budget rule is a guideline, not a rigid law. The version that works for your specific income, city, and life stage is the right version for you.

How to Actually Start Using the 50/30/20 Budget Rule

Here is a simple action plan you can start today:

Step 1: Calculate your monthly take-home pay Add up all income after taxes. If you have irregular income, use your average from the last three months.

Step 2: Multiply by 0.50, 0.30, and 0.20 These are your three targets for the month.

Step 3: Look at last month’s spending Sort your recent bank and credit card statements into needs, wants, and savings. Be honest about which category each expense falls into.

Step 4: Compare your actual spending to your targets Where are you over? Where are you under? That gap is where you start making changes.

Step 5: Set up automatic savings Set an automatic transfer to a savings account on the day your paycheck arrives. Even $50 or $100 a month counts. The habit is what matters.

Step 6: Track monthly and adjust You do not need a fancy app to do this. A simple note on your phone or a basic spreadsheet works fine. The point is awareness.

Best Budgeting Apps to Help You Use the 50/30/20 budget Rule in 2026

You do not need a budgeting app, but they do make it easier to stay consistent. A few options that work well with the 50/30/20 framework:

- YNAB (You Need a Budget): Best for people serious about getting out of debt and building savings. It has a learning curve but gets results.

- Monarch Money: Clean interface, great for tracking spending by category. Works well for households with shared finances.

- Copilot: Excellent for automatic categorization. Many users find it does most of the sorting work for them.

- A basic spreadsheet: Google Sheets works perfectly well and costs nothing.

Any of these can be set up with three simple categories: needs, wants, and savings. You do not need 47 sub-categories. You need three buckets and consistent attention.

The 50/30/20 Budget Rule vs Other Budgeting Methods

You may have heard of other budgeting methods like zero-based budgeting or the envelope system. Here is how they compare:

The zero-based budget assigns every single dollar a job. It is more detailed and more powerful for people who want complete control, but it takes more time and effort to maintain each month.

The envelope system uses physical cash in envelopes for different spending categories. It is very effective for controlling impulse spending, but inconvenient in a world where most transactions are digital.

The 50/30/20 rule is the best starting point for beginners because it requires the least effort while still producing real results. Once you have the basics down and want more control, you can layer in more detailed methods.

Final Thoughts: The 50/30/20 Budget Rule Is a Starting Point, Not a Destination

The 50/30/20 budget rule is not going to solve every financial problem overnight. But it will give you something most people desperately need: a clear picture of where your money is going and a simple system for improving it.

Start with your numbers. Sort your expenses honestly. Set up even a small automatic savings. Then adjust as your income and life situation evolve.

The goal is not perfection. The goal is progress. And the 50/30/20 budget rule, even in its simplest form, is one of the most effective tools for making real financial progress in 2026.

Want to know exactly how much you take home after taxes? Use our free Take-Home Pay Calculator at Fiscible. It takes less than a minute and gives you the exact number you need to start budgeting with the 50/30/20 rule.