Confused about how to choose health insurance plan in 2026? This guide breaks down HMO vs PPO, deductibles, premiums, and open enrollment so you can pick the right plan without the headache.

Introduction

Picking a health insurance plan sounds like it should be simple. You go online, look at a few options, and choose one. But anyone who has actually sat down during open enrollment knows that it feels more like solving a puzzle without the picture on the box.

There are deductibles, copays, coinsurance, networks, and plan tiers. There are abbreviations like HMO, PPO, EPO, and HDHP. And every option seems to come with a trade-off that makes you second-guess yourself.

Here is the thing though. Choosing the right health insurance plan does not have to be painful. Once you understand what each piece actually means and how it affects your wallet, the decision becomes a lot clearer.

This guide is going to walk you through exactly how to choose a health insurance plan in 2026 without confusion, without jargon overload, and without leaving money on the table.

What Kind of Health Insurance Plans Are Out There?

Before you can choose a health insurance plan, you need to know what the options actually are. Here are the most common plan types you will run into during open enrollment 2026.

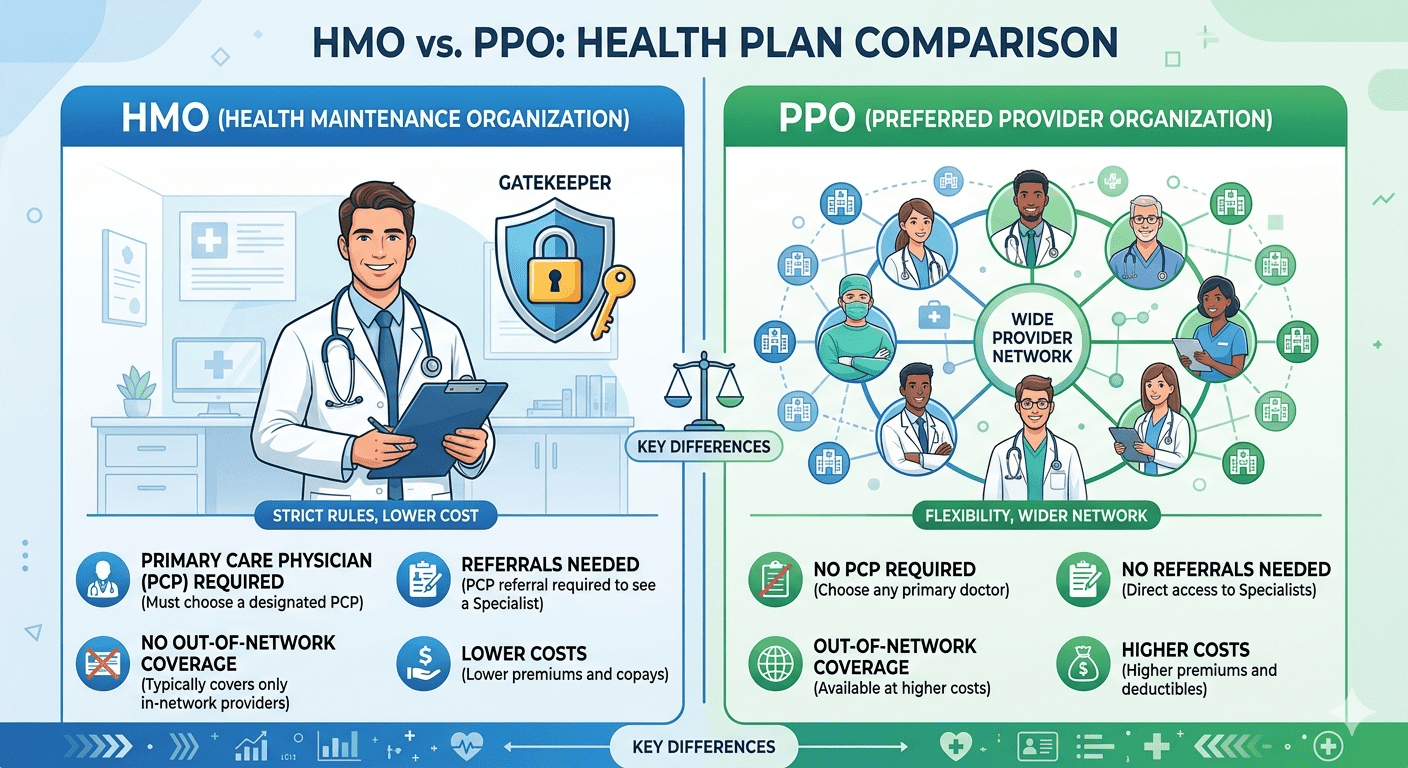

HMO (Health Maintenance Organization)

An HMO plan requires you to pick a primary care physician, or PCP, who acts as the main point of contact for all your healthcare. If you need to see a specialist, you need a referral from your PCP first. The upside is that HMO plans usually have lower premiums and lower out-of-pocket costs. The downside is less flexibility when it comes to which doctors you can see.

HMO plans work really well for people who are generally healthy, live in one area, and do not need to see specialists regularly.

PPO (Preferred Provider Organization)

A PPO plan gives you a lot more freedom. You can see any doctor, in-network or out-of-network, without needing a referral. This flexibility comes at a cost, though. PPO premiums are usually higher, and out-of-network care can be expensive.

If you have ongoing health conditions, travel frequently, or want to keep seeing specific doctors, a PPO is often worth the extra premium.

EPO (Exclusive Provider Organization)

An EPO is kind of a mix between the two. You do not need referrals, but you are limited to doctors within the plan’s network. Go outside the network, and you pay the full cost yourself (except in emergencies).

HDHP (High-Deductible Health Plan)

An HDHP has a higher deductible than standard plans, meaning you pay more out-of-pocket before insurance kicks in. But HDHPs usually come with lower monthly premiums, and they qualify you to open a Health Savings Account (HSA), which lets you set aside pre-tax money for medical expenses.

For younger, healthier people who rarely need medical care, an HDHP can save a significant amount of money every year.

Understanding the Key Terms That Actually Matter

One reason choosing a health insurance plan feels so confusing is that there are a lot of terms that sound similar but mean different things. Here is a plain-English breakdown.

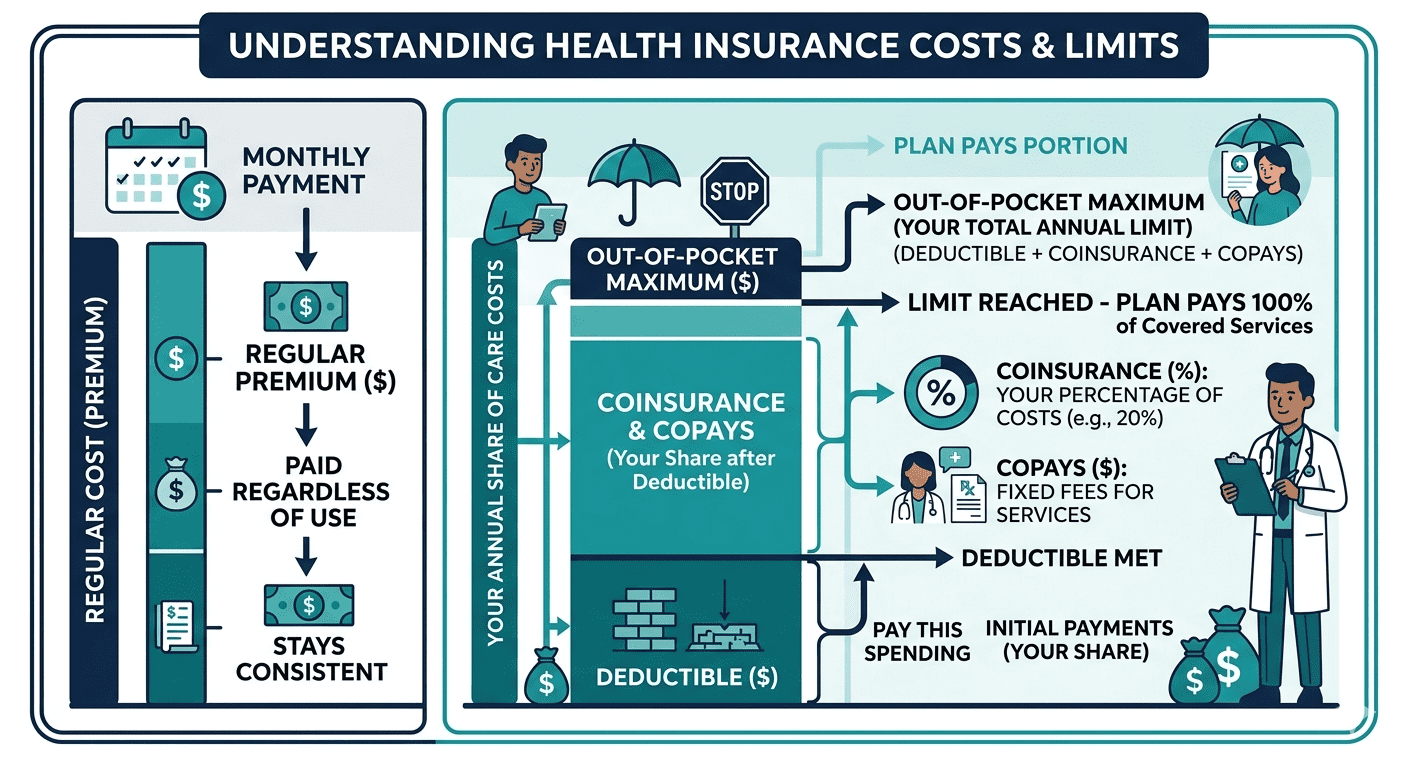

Premium This is the monthly amount you pay to have health insurance, regardless of whether you use it or not. Think of it like a subscription fee.

Deductible This is the amount you pay out-of-pocket for covered health services before your insurance company starts paying. If your deductible is $2,000, you pay the first $2,000 of medical bills yourself each year.

Copay A copay is a fixed amount you pay for a specific service, like $30 for a doctor visit or $15 for a prescription. Copays often apply even after you’ve met your deductible.

Coinsurance After you meet your deductible, coinsurance is your share of the costs. If your plan has 20% coinsurance, you pay 20% of covered services and the insurance company pays 80%.

Out-of-Pocket Maximum This is the most you will ever pay in a single year. Once you hit this number, your insurance covers 100% of covered services for the rest of the year. This is your financial safety net.

How to Actually Choose a Health Insurance Plan: Step by Step

Now that you know the vocabulary, here is how to go through the actual decision process.

Step 1: Think About Your Health Needs for the Year

Before you even look at plans, take stock of what you actually need. Ask yourself:

- How often did you visit the doctor last year?

- Do you take any regular prescriptions?

- Do you have any planned procedures, like surgery or having a baby?

- Do you have kids or dependents who need coverage?

If you are generally healthy and rarely see a doctor, a lower-premium plan like an HDHP might make sense. If you have ongoing conditions or take expensive medications, you will want a plan with lower out-of-pocket costs even if the premium is higher.

Step 2: Check If Your Doctors Are In-Network

This is one of the most overlooked steps when choosing a health insurance plan. People sign up for a plan and then discover their favorite doctor is not covered, which means either paying out-of-network rates or switching providers.

Before you lock in any plan, call your doctor’s office directly or use the insurer’s provider search tool to confirm that your doctors are included in the network.

Step 3: Calculate the True Cost, Not Just the Premium

A lot of people compare health insurance plans based on the monthly premium alone. That is a mistake. The real cost of a health insurance plan includes your premium plus your expected out-of-pocket spending.

Do a quick estimate. If you are choosing between a $300/month premium plan with a $1,000 deductible and a $150/month premium plan with a $4,000 deductible, think about which one costs less based on how much healthcare you actually use.

For someone who visits the doctor twice a year and takes a cheap generic drug, the lower-premium plan wins easily. For someone managing a chronic condition who sees specialists regularly, the higher-premium plan with lower cost-sharing usually comes out ahead.

Step 4: Look at the Drug Formulary

If you take prescription medications, pull up the plan’s drug formulary, which is the list of covered drugs. Insurers divide drugs into tiers, and the tier determines your copay. A medication that costs $20 under one plan might cost $150 under another.

This step alone can save you hundreds of dollars a year.

Step 5: Consider an HSA If You Are Eligible

If you are leaning toward an HDHP, check whether it is HSA-eligible. In 2026, you can contribute up to $4,300 as an individual or $8,550 for a family to a Health Savings Account. That money goes in pre-tax, grows tax-free, and comes out tax-free when you spend it on qualified medical expenses.

An HSA is genuinely one of the most powerful tax advantages available to regular people, and most people do not use it.

Open Enrollment 2026: What You Need to Know

Open enrollment is the window each year when you can sign up for or change your health insurance plan. For marketplace plans in 2026, the enrollment window typically runs from November 1 through January 15 in most states, though dates can vary by state.

Outside of open enrollment, you can only make changes to your health insurance plan if you experience a qualifying life event. These include getting married, having a baby, losing other coverage, or moving to a new area.

If you miss open enrollment and do not have a qualifying event, you are stuck with your current plan until the next enrollment period. So marking the dates on your calendar matters.

Health Insurance for Self-Employed People in 2026

If you are self-employed, a freelancer, or a gig worker, you do not have an employer picking up part of your premium. You are covering the full cost yourself, which can sting.

Here is what works for self-employed people when it comes to health insurance:

The ACA marketplace is usually the first place to look. Depending on your income, you may qualify for premium tax credits that significantly reduce your monthly cost. In 2026, these subsidies have remained stronger than they were a few years ago, so it is worth running the numbers before assuming you cannot afford coverage.

Health insurance associations and professional organizations sometimes offer group rates to members, which can be more affordable than individual marketplace plans.

If you are in good health and want to keep costs low, a catastrophic plan combined with an HSA is another option. You pay very little monthly, handle routine care out-of-pocket using your HSA, and have protection against major medical events.

Common Mistakes People Make When Choosing a Health Insurance Plan

Plenty of people get this wrong every year. Here are the mistakes worth avoiding.

Choosing based on the lowest premium alone is probably the most common one. A rock-bottom premium often comes with a sky-high deductible. If you actually need medical care, you could end up paying far more than you would have with a slightly higher-premium plan.

Not checking the network is another big one. Assuming your doctor is covered without verifying it leads to unpleasant surprises when the bill comes in.

Ignoring the out-of-pocket maximum is a real problem if something serious happens. The out-of-pocket max is your most important number in a worst-case scenario.

Forgetting to compare drug costs is a mistake that hits hardest for people on regular medications. Always check the formulary.

Final Thoughts

Choosing a health insurance plan does not have to feel overwhelming. The trick is to stop looking at it as a bureaucratic chore and start treating it like a financial decision, because that is exactly what it is.

Know your health needs, understand the real cost of each plan, check your network, look at your prescriptions, and use an HSA if you qualify. Do all of that, and you will be in a much stronger position than most people who just pick whatever looks cheapest at first glance.

Open enrollment comes every year. Make 2026 the year you actually choose a health insurance plan that works for you.

Try the Take-Home Pay Calculator at Fiscible.

One thought on “HOW TO CHOOSE HEALTH INSURANCE PLAN IN 2026: A COMPLETE GUIDE FOR BEGINNERS”