Wondering what homeowners insurance actually covers in 2026? This guide breaks down dwelling coverage, exclusions, and 10 real ways to lower your home insurance premium right now.

Introduction

If you own a home, homeowners insurance is not optional. Your mortgage lender almost certainly requires it, and even if your house is paid off, going without it is a financial risk very few people can actually afford to take.

But here is what most homeowners do not realize: a lot of people pay more for their homeowners insurance than they need to, and a lot of people assume they are covered for things that are not actually in their policy.

Both of those problems are fixable.

This guide breaks down exactly what homeowners insurance covers in 2026, what it does not cover (which is just as important), and how to actually reduce your home insurance premium without gutting your coverage.

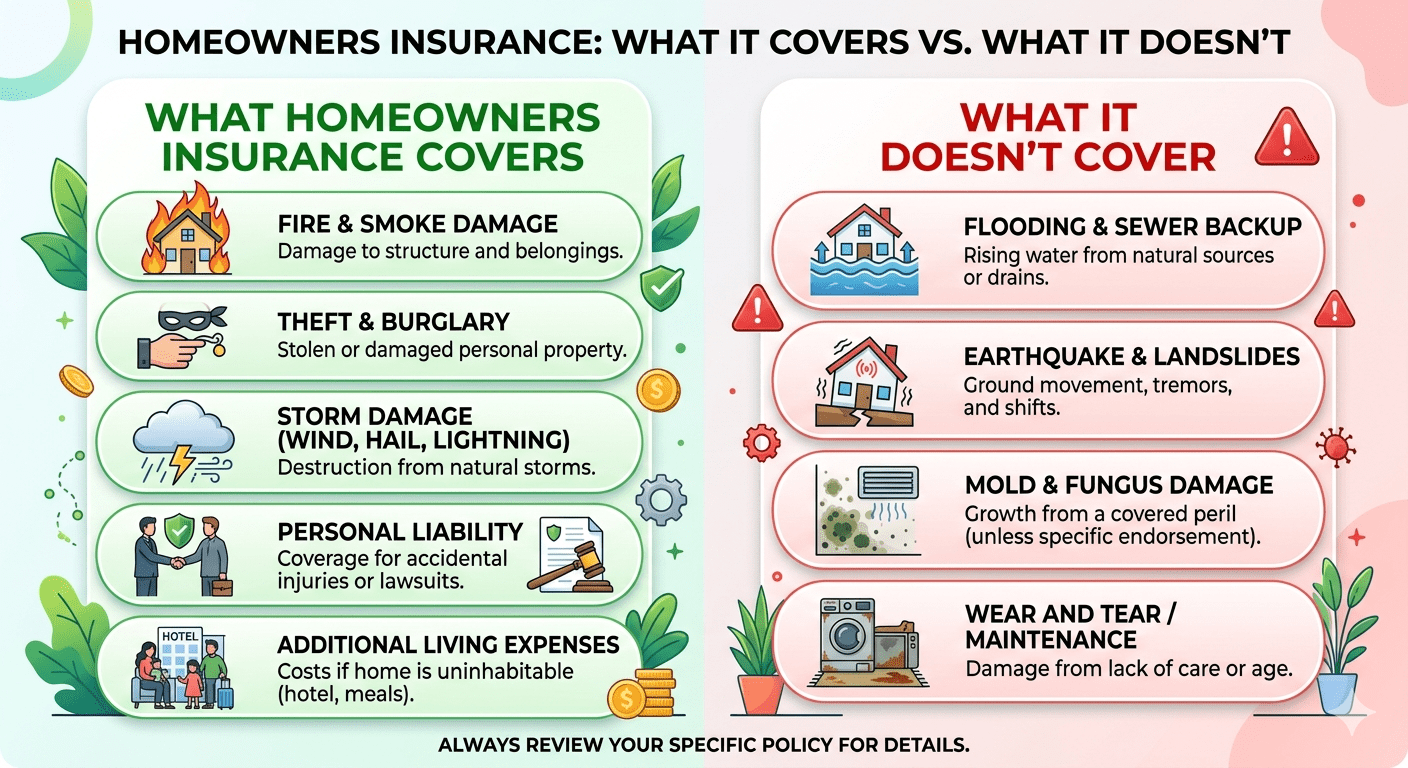

What Does Homeowners Insurance Actually Cover?

Homeowners insurance is not one single type of coverage. It is a bundle of different protections that work together to protect your home, your belongings, and your finances. Here is how the main pieces break down.

Dwelling Coverage

Dwelling coverage is the core of any homeowners insurance policy. It pays to repair or rebuild the physical structure of your home if it is damaged by a covered event. This includes the walls, roof, floors, built-in appliances, and attached structures like a garage.

The key word here is “covered event.” Standard policies cover things like fire, lightning, windstorms, hail, explosions, and vandalism. They do not cover everything, which we will get to shortly.

When you set up your homeowners insurance policy, you want your dwelling coverage to reflect the full replacement cost of your home, which is how much it would cost to rebuild it from scratch. This is not the same as your home’s market value or what you paid for it.

Other Structures Coverage

This extends coverage to structures on your property that are not attached to your house. A detached garage, a fence, a shed, or a pool all fall into this category. Standard policies typically set this at 10% of your dwelling coverage automatically.

Personal Property Coverage

Personal property coverage reimburses you for your belongings if they are stolen or damaged. This includes furniture, clothing, electronics, appliances, jewelry, and most other personal items.

One thing to watch here: most standard policies cover personal property at actual cash value, which means depreciation is factored in. If your three-year-old laptop gets stolen, you get what it is worth today, not what you paid for it. Upgrading to replacement cost value for personal property usually adds a small amount to your premium but makes a significant difference if you ever need to file a claim.

Liability Coverage

Liability coverage is one of the most underrated parts of a homeowners insurance policy. If someone is injured on your property, say a neighbor slips and falls on your icy walkway, liability coverage pays for their medical bills and legal costs if they sue you.

Standard policies usually come with $100,000 in liability coverage. Most financial advisors suggest bumping that up to at least $300,000. If you have significant assets, adding an umbrella policy on top is worth considering.

Additional Living Expenses (ALE)

If your home is damaged and becomes unlivable while repairs happen, ALE coverage pays for your temporary housing, meals, and other extra costs. This is also called loss of use coverage. It kicks in if you need to stay in a hotel or rent an apartment while your roof is being rebuilt after a storm.

What Homeowners Insurance Does NOT Cover

This is the part most people skip, and it is the part that leads to the most nasty surprises when a claim gets denied.

Floods

Standard homeowners insurance does not cover flood damage. At all. Not even from a burst pipe in the street or a river that overflows nearby. Flood damage requires a separate flood insurance policy, typically purchased through the National Flood Insurance Program or private insurers.

Given that floods are now the most common and costly natural disaster in the United States, this gap in coverage catches a lot of homeowners off guard.

Earthquakes

Earthquake damage is also excluded from standard homeowners insurance policies. If you live in a high-risk area like California or the Pacific Northwest, earthquake insurance is worth seriously considering as a separate policy.

Routine Wear and Tear

Your roof slowly deteriorating over 25 years, your HVAC system aging out, or your plumbing corroding over time? None of that is covered by homeowners insurance. Insurance is designed for sudden, unexpected events, not gradual deterioration.

Mold and Pest Damage

Mold is generally not covered unless it is the direct result of a covered event, like mold that grows after a pipe bursts and you file a claim promptly. Termite damage and pest infestations are almost always excluded entirely.

High-Value Items Above Policy Limits

Jewelry, fine art, collectibles, and high-end cameras are covered under personal property, but usually only up to a sublimit, which might be $1,500 for jewelry. If you have items worth more than that, you need a scheduled personal property endorsement, which is an add-on that covers specific items at their full appraised value.

How Much Does Homeowners Insurance Cost in 2026?

The average homeowners insurance premium in the United States has been rising. In 2026, most homeowners are paying somewhere between $1,500 and $2,500 per year for a standard policy, though costs vary significantly depending on where you live, the value of your home, your claims history, and the coverage levels you choose.

States with high risk for hurricanes, tornadoes, or wildfires are seeing the steepest increases. Florida, Louisiana, California, and Texas have all seen double-digit premium hikes in recent years as insurers adjust for increased climate-related risk.

That makes shopping smart more important than ever.

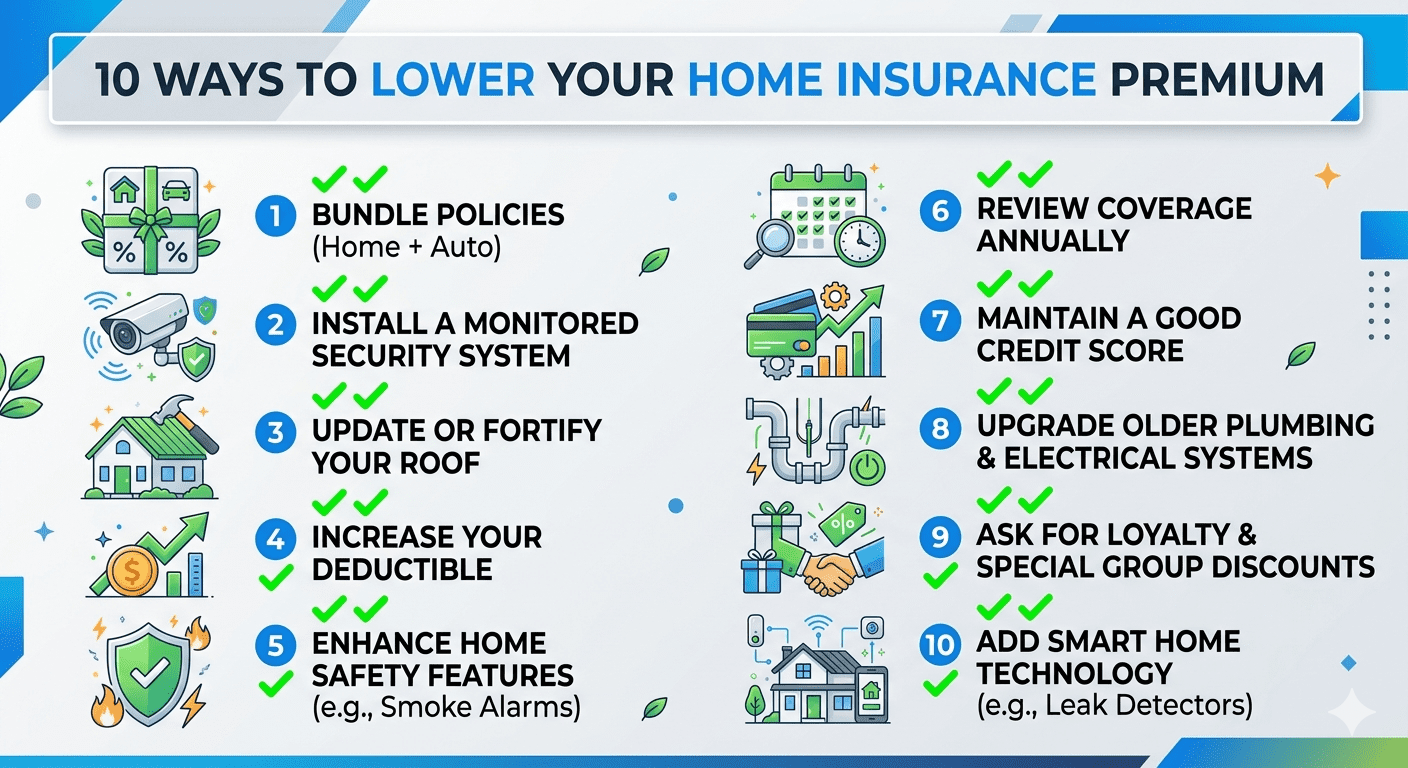

10 Real Ways to Lower Your Homeowners Insurance Premium

Here is the part most people are looking for. The good news is that there are legitimate ways to reduce your home insurance premium without just cutting coverage you actually need.

1. Bundle Your Home and Auto Insurance

Most major insurers offer a discount when you buy both your homeowners and auto insurance from the same company. The discount typically ranges from 5% to 25%. This is the fastest, easiest way to lower your premium without changing anything about your coverage.

2. Raise Your Deductible

Your deductible is what you pay out-of-pocket before insurance pays the rest. Raising your deductible from $500 to $1,000 or $2,000 can noticeably lower your premium. The trade-off is that you will pay more if you do file a claim. This strategy works best if you have an emergency fund to cover the higher deductible if needed.

3. Improve Your Home Security

Installing a monitored alarm system, smart smoke detectors, deadbolt locks, or a video doorbell often qualifies you for a security discount with your insurer. Some companies give discounts of 5% to 15% for these upgrades. The upfront cost of a security system can pay for itself quickly through insurance savings.

4. Make Your Home More Disaster-Resistant

Adding storm shutters, upgrading your roof to impact-resistant materials, or reinforcing your garage door against high winds can all reduce your premium, especially in states where severe weather is common. Ask your insurer specifically which home improvements qualify for discounts.

5. Avoid Filing Small Claims

This one feels counterintuitive, but it is real. Filing frequent small claims can raise your premium at renewal or even get your policy non-renewed. If you have a minor repair that would cost $400 and your deductible is $500, just pay for it yourself. Your claims history affects your insurance rates, and keeping it clean saves you money in the long run.

6. Check Your Credit Score

In most states, insurers use your credit score as a factor in calculating your homeowners insurance premium. A stronger credit score typically means a lower rate. Paying down debt, keeping credit card balances low, and making on-time payments all contribute to a better insurance rate over time.

7. Shop Around Every Year

Loyalty to an insurance company rarely pays off. Rates change, and new customers often get better deals than long-term policyholders. Getting quotes from at least three different insurers before your renewal date is one of the most effective ways to find savings on your homeowners insurance.

8. Ask About Discounts You Might Be Missing

Insurers have discounts for all kinds of things, and they do not always advertise them. Ask specifically about discounts for being claim-free, being over 55, having a new home, being a non-smoker, or having a newer roof or updated electrical system. You might be leaving money on the table without knowing it.

9. Remove Coverage You No Longer Need

If you have paid off a boat you owned when you first set up your policy, or if an older vehicle is now covered elsewhere, make sure your homeowners insurance reflects your current situation. Outdated coverage levels or unnecessary add-ons quietly inflate your premium.

10. Consider Paying Annually Instead of Monthly

Many insurers charge a small fee for monthly installments. Paying your homeowners insurance premium in full once a year, if your budget allows, can save a few percent off the total cost.

How to Make Sure You Have Enough Coverage

Choosing the lowest possible premium should not come at the cost of being underinsured. Here is what to check.

Your dwelling coverage should be set to the rebuild cost, not the market value. These two numbers are often very different. Construction costs have risen significantly, so if you set your dwelling coverage three or four years ago and haven’t revisited it, there is a good chance you are underinsured today.

Your personal property coverage should reflect what you actually own. Do a home inventory. Take photos or video of each room and note high-value items. This makes claims faster and helps you see whether your coverage limit is realistic.

And if your liability coverage is still at the default $100,000, bump it up. The cost difference is small and the protection difference is enormous.

Final Thoughts

Homeowners insurance is one of those things that feels invisible until you desperately need it. When your house catches fire, when someone gets hurt on your property, when a storm tears off part of your roof, a good policy is what stands between you and a financial crisis.

Understanding what your homeowners insurance covers and what it does not puts you in a position to fill the gaps. And using the practical strategies in this guide, you can bring your premium down without leaving yourself exposed.

Take an hour this year to review your homeowners insurance policy. Check your coverage amounts, compare quotes, ask about discounts, and make sure your coverage still matches your life. That one hour could save you hundreds of dollars a year and a whole lot of stress if something goes wrong.

To know more about insurance debts, check out this article on fiscible.