Do I have to have health insurance in 2026? There is no federal penalty, but the real costs of going uninsured can be devastating. Here is everything you need to know.

Introduction

If you have been asking yourself, “do I have to have health insurance?” you are not alone. Millions of Americans ask this exact question every year, especially when open enrollment rolls around and they are staring at premium prices that feel impossible to afford.

The short answer? At the federal level, no, you do not have to have health insurance. There is no IRS penalty waiting for you if you go without coverage. But the longer, more honest answer is a lot more complicated, and the consequences of going uninsured can turn a single bad month into years of financial recovery.

This article breaks down what the law actually says, which states still require health insurance, what happens if you get sick without coverage, and whether skipping it is ever a smart financial move.

The Federal Law: What Changed and Where Things Stand in 2026

Back when the Affordable Care Act first launched, there was a federal individual mandate that required most Americans to have health insurance or pay a penalty on their taxes. That penalty was called the “individual shared responsibility payment,” and it was real.

In 2017, Congress passed the Tax Cuts and Jobs Act, which zeroed out that federal penalty starting in 2019. So if you do not have health insurance in 2026, the federal government will not fine you. You do not need to report your insurance status on your federal tax return, and the IRS is not going to come after you.

That part is simple enough.

But saying “no federal penalty” is not the same as saying “no consequences.” And if you are asking whether you legally have to have health insurance, the answer depends on where you live.

States That Still Require Health Insurance in 2026

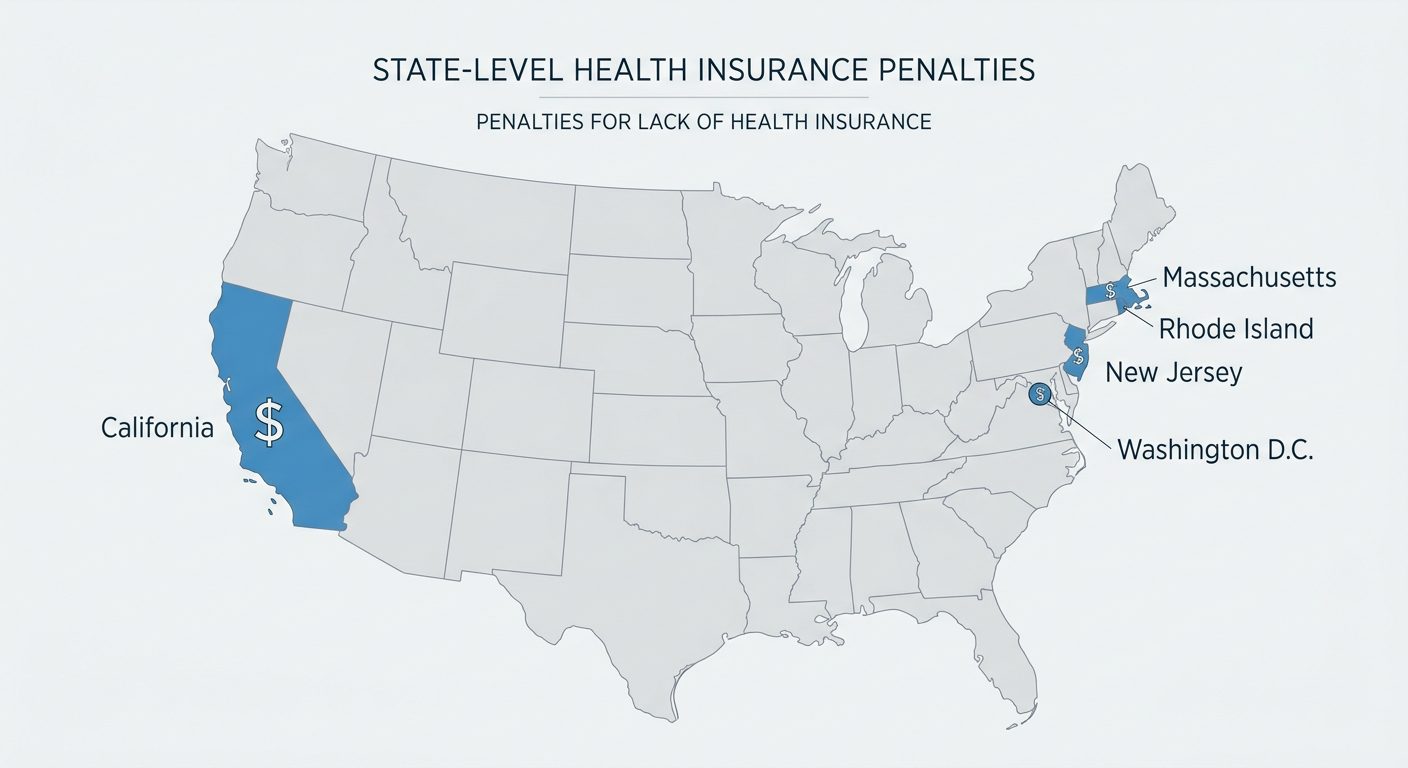

Even though the federal mandate is gone, several states created their own requirements. If you live in one of these places, you do have to have health insurance, and there are real financial penalties for skipping it.

Here is the current list:

California reinstated its own individual mandate starting in 2020. If you are uninsured for any part of the year, you will face a penalty calculated by the California Franchise Tax Board. For 2025 taxes filed in 2026, the minimum penalty is around $950 per adult and $450 per dependent child. Higher incomes mean higher penalties.

Massachusetts has required health insurance since 2006, long before the ACA even existed. The state requires adults 18 and older who can access affordable coverage to get it. Penalties in Massachusetts vary based on your income relative to the federal poverty level.

New Jersey has enforced its own state-level mandate since 2019. Like California, the penalty is based on income and household size, calculated using the price of bronze-level health insurance in the state.

Rhode Island also requires residents to maintain health coverage. The penalty kicks in at tax time if you did not have qualifying coverage throughout the year.

Washington, D.C. follows a similar structure with its own individual responsibility requirement.

Vermont technically has a mandate on the books, but as of now, there is no monetary fine attached to it.

If you live in any of these states, the question “do I have to have health insurance” has a clear legal answer: yes, you do, or you will pay for it at tax time.

So What Actually Happens If You Go Without Health Insurance?

Here is where the conversation gets serious. Just because there is no federal penalty does not mean going without health insurance is free. The health insurance penalty 2026 includes:

You pay the full bill, at full price.

When you have health insurance, your insurer has negotiated discounted rates with hospitals, doctors, and labs. An insured patient might pay a $150 copay for an MRI. An uninsured patient gets the full “chargemaster” rate for that same scan, which can be $2,500 or more. You are paying 2 to 5 times what an insured person pays for the exact same service.

A single emergency can cost tens of thousands of dollars.

A three-day hospital stay now averages over $30,000. A trip to the emergency room for something as routine as a broken arm can exceed $7,500. For serious conditions like a heart attack, stroke, or cancer diagnosis, you are looking at bills that can run into the hundreds of thousands of dollars.

Federal law (called EMTALA) requires hospitals to stabilize you in an emergency regardless of whether you can pay. But stabilization is not the same as full treatment, and the bill still comes. Every single time.

Medical debt follows you.

Unpaid medical bills go to collections agencies. Collections accounts appear on your credit report and can drag your credit score down significantly, making it harder to rent an apartment, qualify for a car loan, or pass a background check for a job. In some cases, hospitals and collection agencies can pursue wage garnishment or place liens on your property if they win a judgment against you.

According to research from the Kaiser Family Foundation, more than six in ten uninsured Americans report medical debt from expenses they could not afford. That number drops to about four in ten for people who have coverage.

You are less likely to catch serious conditions early.

When you do not have health insurance, you are much more likely to skip preventive care, avoid going to the doctor when something feels off, and delay filling prescriptions. Conditions that are cheap and easy to treat when caught early become expensive and dangerous when left alone for months or years.

Do I Have to Have Health Insurance If I am Young and Healthy?

This is the argument a lot of people make, and honestly, there is some truth in it for a very specific scenario. If you are young, genuinely healthy, and would be paying high premiums entirely out of pocket without any employer contribution or subsidy, your total annual healthcare costs might technically be lower going uninsured, assuming nothing goes wrong.

The key phrase there is “assuming nothing goes wrong.”

Nobody plans to get hit by a car. Nobody plans to have appendicitis at 28. Nobody plans to get a cancer diagnosis in their 30s. The whole point of insurance is to protect you from the scenarios you cannot predict.

Health economists at Harvard and Johns Hopkins have pointed out that for truly healthy young people who only need occasional primary care, total costs could theoretically be lower uninsured. But the moment you have any significant medical event, that calculation flips completely. And one bad year can follow you financially for a decade.

Alternatives to Traditional Health Insurance If You Cannot Afford It

If the reason you are asking “do I have to have health insurance” is really about the cost, there may be options you do not know about.

Medicaid is free or very low cost health coverage for people with lower incomes. Eligibility varies by state, but roughly half of uninsured Americans qualify for either Medicaid or subsidized marketplace coverage and simply do not know it. You can check your eligibility at healthcare.gov.

ACA Marketplace Plans with Subsidies are available to people who earn too much for Medicaid. Depending on your income, you may qualify for premium tax credits that significantly reduce what you pay each month. In some cases, marketplace plans are available for as little as a few dollars a month after subsidies.

Medicaid Expansion States have broader eligibility rules. If you live in a state that expanded Medicaid under the ACA, your income limit for free coverage is higher.

CHIP (Children’s Health Insurance Program) covers children in families that earn too much for Medicaid but cannot afford private insurance. If you have kids, this is worth checking regardless of your own situation.

Community Health Centers (also called FQHCs) offer medical care on a sliding fee scale based on what you can afford. Even if you are uninsured, these centers provide primary care, mental health services, and prescription assistance.

Short-Term Health Plans are cheaper than ACA plans but cover less and are not available in all states. They can fill a temporary gap, but they are not a long-term substitute for comprehensive coverage.

Special Enrollment Periods: When You Can Sign Up Outside Open Enrollment

Open enrollment typically runs from November through mid-January for coverage starting the following year. But if you miss it, you are not necessarily stuck until the next open enrollment period.

You qualify for a Special Enrollment Period if you experience a qualifying life event, such as losing a job (and the coverage that came with it), getting married or divorced, having or adopting a child, moving to a new state, or turning 26 and aging off your parents’ plan.

If you recently lost coverage for any of these reasons, you have a window to enroll in a new plan without waiting for open enrollment.

Do I Have to Have Health Insurance If My Employer Offers It?

Employers with 50 or more full-time equivalent employees are still required under the ACA’s employer mandate to offer affordable health coverage to their full-time workers. You are not legally required to accept it, but if your employer offers qualifying coverage and you decline it, you generally cannot receive subsidies on the marketplace either.

From a purely financial standpoint, if your employer contributes to your premium, saying no to that coverage is turning down compensation. Most employer-sponsored plans are worth taking, especially when the employer is covering a significant portion of the cost.

How to Think About This Decision: Do I Have to Have Health Insurance

So, do you have to have health insurance? Legally, it depends on your state. Practically, the risks of going without it are significant for most people.

A simple way to think through it is given below:

If you live in California, Massachusetts, New Jersey, Rhode Island, or Washington D.C., you are legally required to have qualifying coverage or face a state tax penalty. That is not optional.

If you live anywhere else, there is no federal or state penalty. But the financial exposure from a single medical emergency dwarfs almost any premium you would pay for a basic plan.

If cost is the barrier, check your eligibility for Medicaid or marketplace subsidies before assuming you cannot afford it. A lot of people who think health insurance is out of reach qualify for coverage that costs far less than they expect.

If you are genuinely healthy, rarely use healthcare, and earn too much for any subsidies while having no employer option, there is a small chance you could come out ahead financially by going uninsured in a given year. But that calculation only holds as long as nothing goes wrong.

Bottom Line: Is health insurance required

The federal government no longer requires you to have health insurance, and there is no national penalty for going without it. But five states and Washington D.C. still enforce their own mandates with real financial consequences. And even in states with no penalty, the risk of catastrophic medical bills, damage to your credit, and delayed care make going uninsured a genuinely risky choice for most people.

If you are weighing this decision, start by understanding what coverage options are available at your income level. You might be surprised at what you can access for a lot less than the sticker price suggests.

Fiscible provides educational financial content to help you make smarter money decisions. This article is for informational purposes only and does not constitute legal, tax, or insurance advice. Consult a licensed professional for guidance specific to your situation.