Want to compare health insurance plans in 2026 but do not know where to start? This guide breaks down premiums, deductibles, HMO vs PPO, and exactly how to pick the right plan for your budget.

Introduction

Trying to compare health insurance plans without a roadmap is genuinely confusing. You land on a comparison page, see a wall of numbers, abbreviations, and plan types, and it is hard to know what actually matters and what you can safely ignore.

The problem is not that health insurance is impossibly complicated. The problem is that nobody teaches you how to compare health insurance properly. You are just expected to figure it out.

This guide is going to change that. By the time you finish reading, you will know exactly what to look for when you compare health insurance plans, what the numbers actually mean, which plan type makes sense for your situation, and how to avoid the most common mistakes people make when picking coverage.

The Five Numbers That Actually Matter When You Compare Health Insurance

Most people look at one thing when they compare health insurance: the monthly premium. That is a mistake that costs a lot of people a lot of money.

The true cost of any health insurance plan is the combination of five numbers. Once you understand all five, you can compare health insurance plans properly.

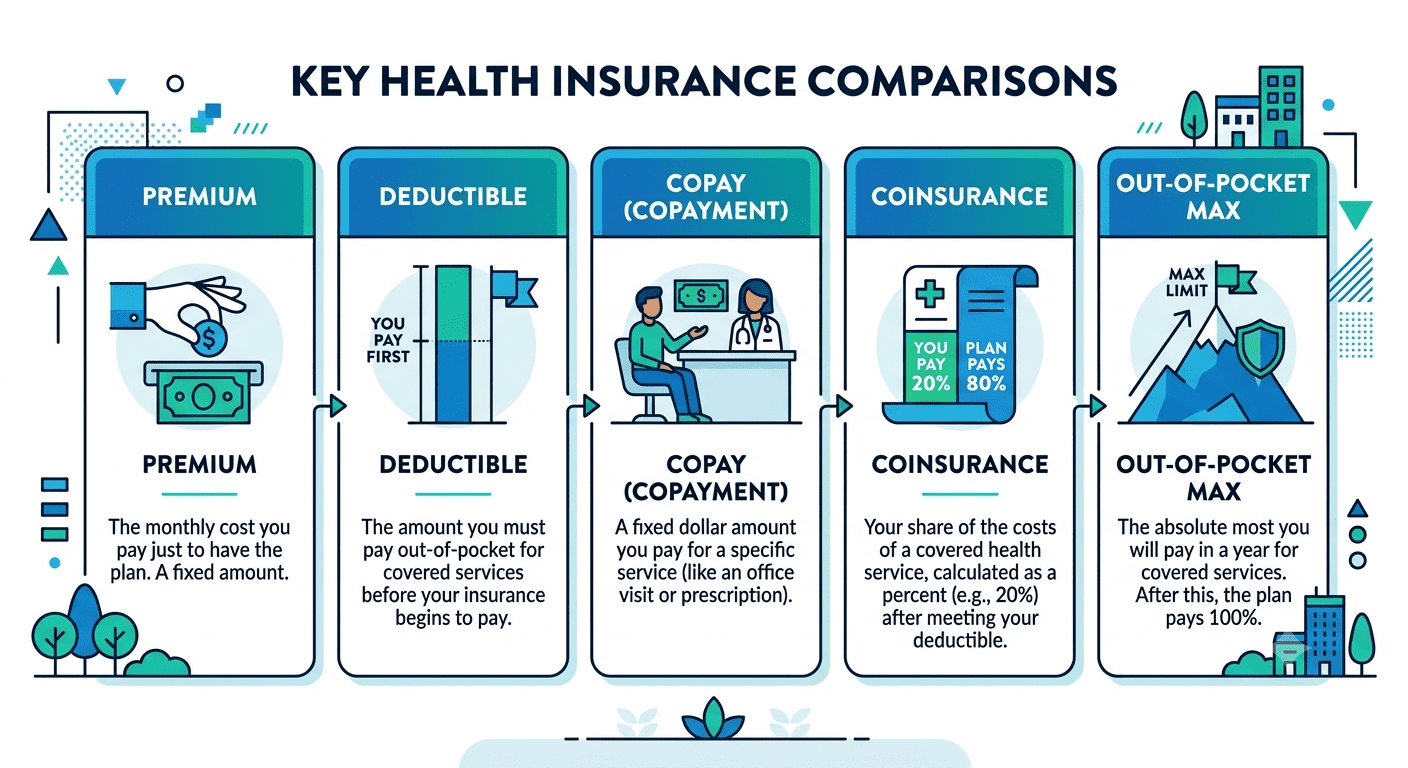

1. Premium

The premium is what you pay every month just to keep the plan active, whether you use any healthcare that month or not. Think of it like a subscription fee for having access to coverage.

Lower premiums sound great, but they almost always come with trade-offs in the other numbers on this list. A plan with a $200 monthly premium and a $7,000 deductible may actually cost you more than a plan with a $400 monthly premium and a $1,500 deductible, depending on how much care you actually use.

2. Deductible

The deductible is the amount you pay out of your own pocket for covered services before your insurance starts sharing the cost. If your deductible is $2,000, you pay the first $2,000 of your medical bills every year before your insurer kicks in anything beyond basic covered services.

High-deductible plans have lower monthly premiums. Low-deductible plans have higher premiums. The question is which combination makes more sense given how much healthcare you actually use.

3. Copay

A copay is a fixed fee you pay for specific services. For example, your plan might charge a flat $30 copay every time you visit your primary care doctor, or $15 for a generic prescription. Copays apply whether or not you have met your deductible, depending on the plan.

When you compare health insurance plans, pay close attention to copay amounts for the services you use most often, things like regular prescriptions, specialist visits, or mental health appointments.

4. Coinsurance

After you meet your deductible, you do not automatically stop paying. Coinsurance is the percentage of costs you share with your insurer after hitting the deductible. A common split is 80/20, meaning your insurance pays 80% and you pay the remaining 20% until you hit your out-of-pocket maximum.

5. Out-of-Pocket Maximum

This is arguably the most important number when you compare health insurance, and the one people overlook most often. The out-of-pocket maximum is the most you will ever pay in a single plan year for covered services.

Once you hit that ceiling, your insurance pays 100% of covered costs for the rest of the year. This number is your protection against financial catastrophe. A plan with a $9,000 out-of-pocket maximum and a serious illness could still leave you with a $9,000 bill. A plan with a $3,500 out-of-pocket max caps your exposure there.

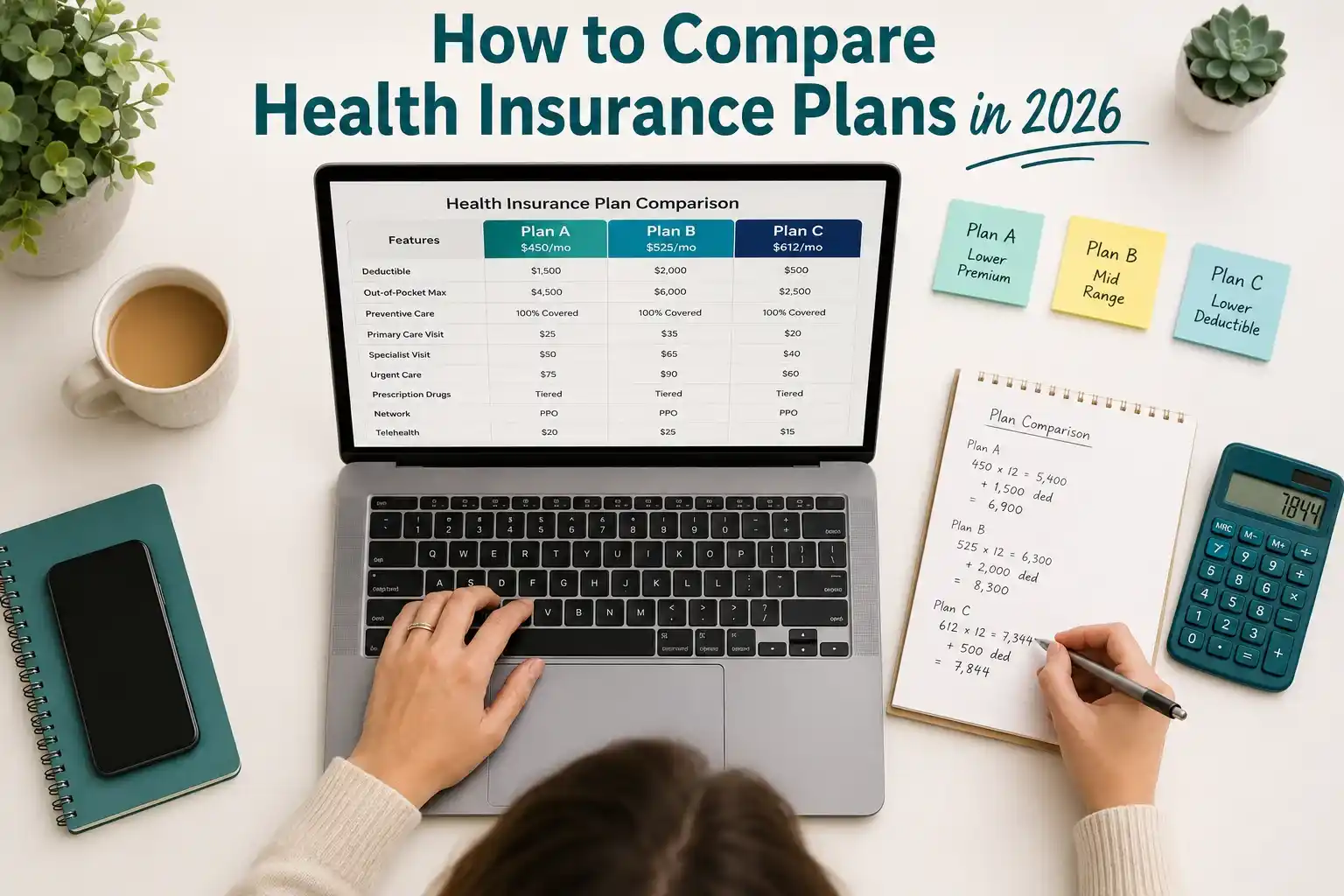

The Formula for Comparing Total Cost

Here is a straightforward formula that makes it much easier to compare health insurance plans on an apples-to-apples basis:

Total Annual Cost = (Monthly Premium x 12) + Expected Out-of-Pocket Costs

To use this, estimate how much medical care you realistically expect to use in the coming year. If you are generally healthy and rarely see a doctor, your expected out-of-pocket costs will be low. If you have ongoing prescriptions, regular specialist visits, or a planned procedure, factor those in.

Then run the math for each plan you are considering. The cheapest monthly premium is not always the cheapest annual plan.

HMO vs PPO vs EPO vs POS: Which Plan Type Is Right for You?

When you compare health insurance plans, you will also need to choose a plan structure. The four main types are HMO, PPO, EPO, and POS. Each one handles your access to doctors and specialists differently.

HMO (Health Maintenance Organization)

An HMO requires you to choose a primary care physician (PCP) who acts as your point of contact for all healthcare. If you need to see a specialist, your PCP has to provide a referral first. You must stay within the plan’s network for covered care, except in genuine emergencies.

HMOs typically have the lowest monthly premiums and predictable copays. The trade-off is less flexibility in choosing your doctors.

An HMO is a good fit if you live in one area and are happy using in-network doctors, you want lower monthly costs, and you do not mind going through your primary doctor for specialist referrals.

PPO (Preferred Provider Organization)

A PPO gives you much more freedom. You can see any doctor or specialist you want without getting a referral. You pay less when you use in-network providers, but you still have partial coverage if you go out of network.

PPOs have higher monthly premiums and usually higher deductibles than HMOs. But if you have an existing relationship with a specialist, travel frequently, or want maximum flexibility in your healthcare choices, a PPO is worth considering.

A PPO works well if you travel often and need consistent access to care across different locations, you have a specific doctor or specialist you want to keep seeing, or you want the freedom to seek care without going through a gatekeeper.

EPO (Exclusive Provider Organization)

An EPO is a middle ground. You do not need referrals to see specialists, which gives you more flexibility than an HMO. But like an HMO, you must stay within the network for non-emergency care. Going out of network on an EPO means paying the full cost yourself with no insurance contribution.

EPOs tend to have premiums between HMO and PPO levels. They are a good option if you want specialist access without referrals but are willing to stay within a set network.

POS (Point of Service)

A POS plan combines features of both HMO and PPO plans. You need a primary care doctor and referrals for specialists like an HMO, but you can also go out of network like a PPO, at a higher cost. POS plans can get complicated to navigate, but they offer flexibility if you occasionally need care from providers outside the network.

Metal Tiers: Bronze, Silver, Gold, and Platinum Explained

If you are shopping on the ACA marketplace, health insurance plans are organized into four metal tiers. These tiers describe how costs are split between you and the insurer, not the quality of care you receive.

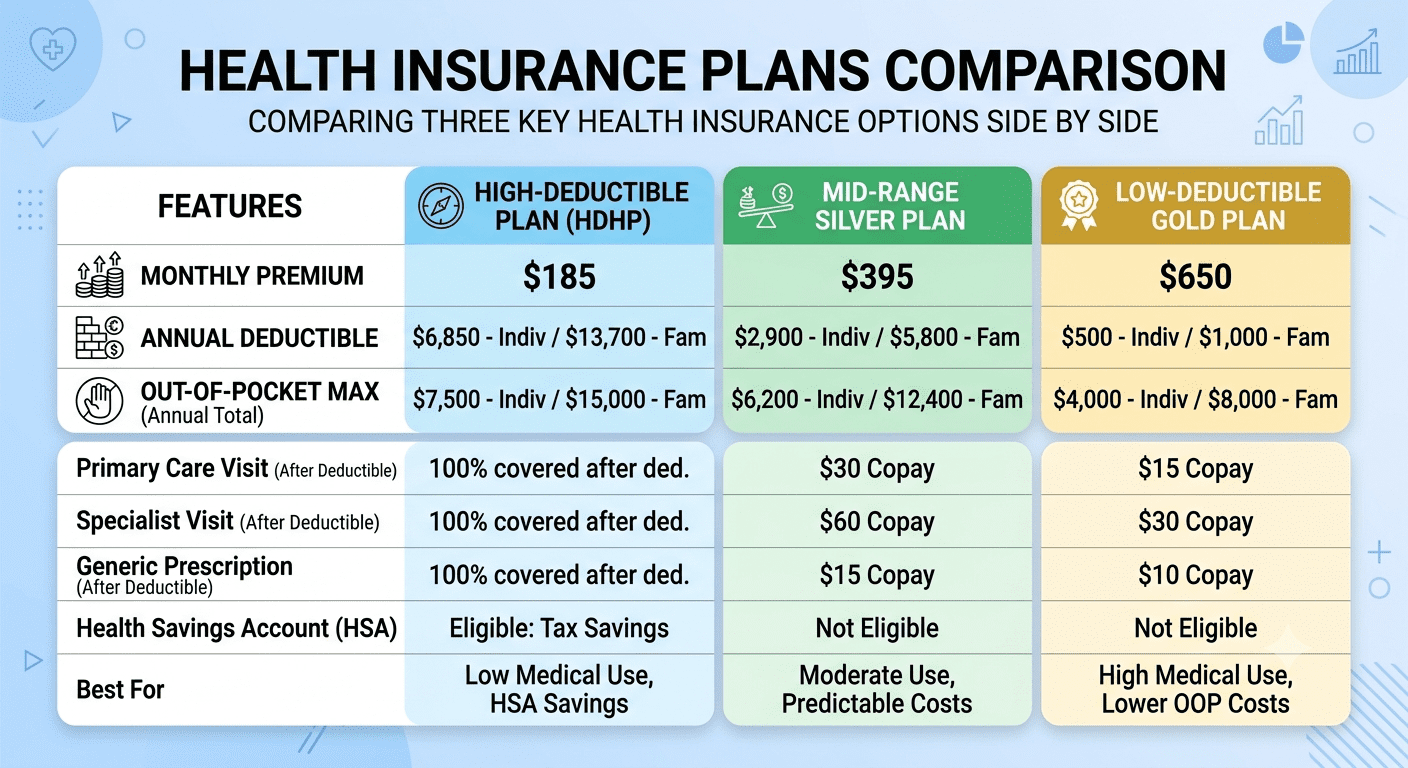

Bronze plans have the lowest monthly premiums but the highest deductibles and out-of-pocket costs. The plan generally covers about 60% of healthcare costs on average, and you cover the other 40%. Bronze plans work best for people who are very healthy, rarely use healthcare, and want protection against catastrophic costs without paying high monthly premiums.

Silver plans are the middle ground, with the insurer covering about 70% of average costs. Silver plans are important because they are the only tier eligible for cost-sharing reductions if your income qualifies. Even if the premium for a silver plan is similar to a bronze plan after subsidies, the silver plan’s reduced deductibles and copays can save a lot of money for regular healthcare users.

Gold plans have the insurer covering about 80% of average costs. Premiums are higher, but deductibles and out-of-pocket costs are lower. Gold plans make financial sense if you know you will have significant medical needs throughout the year.

Platinum plans have the highest premiums but cover roughly 90% of average costs, leaving you with the least out-of-pocket exposure. These plans make sense for people with frequent, predictable healthcare needs who want maximum coverage and minimal surprises.

How to Actually Compare Health Insurance Plans Step by Step

When you sit down to compare health insurance plans, here is the process that makes the most sense.

Step 1: Decide what you need.

Start with an honest assessment of your healthcare use. How often do you see a doctor? Do you have regular prescriptions? Are there specific specialists you want to keep seeing? Do you have any planned procedures in the coming year?

Step 2: Check your doctors are in network.

Before comparing costs, confirm that your preferred doctors, hospitals, and specialists are in the network for any plan you are seriously considering. A great premium means nothing if you have to switch every doctor you currently see.

Step 3: Run the total cost formula.

Use the formula from earlier. Multiply the monthly premium by 12, then add your estimated out-of-pocket costs based on your health situation. Do this for every plan you are comparing.

Step 4: Compare out-of-pocket maximums.

This is your financial safety net. Know the worst-case scenario for each plan before you commit.

Step 5: Check prescription drug coverage.

If you take regular medications, look up your specific drugs in each plan’s formulary (the list of covered drugs). Coverage and cost tier for the same medication can vary significantly between plans.

Step 6: Consider an HSA-eligible plan.

If you choose a High Deductible Health Plan (HDHP), you may be eligible to open a Health Savings Account (HSA). Contributions to an HSA are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses. For people who are relatively healthy, this combination can be one of the most tax-efficient ways to manage healthcare cost.

Common Mistakes People Make When They Compare Health Insurance

Understanding what to avoid is just as useful as knowing what to look for.

Focusing only on the monthly premium. The cheapest plan on paper can easily become the most expensive plan in practice if you end up with a high deductible, limited network, or poor prescription coverage. Always calculate total annual cost.

Skipping the network check. Your favorite doctor, the hospital closest to your home, or the specialist managing a chronic condition might not be in the network for a plan you are considering. Always verify before you enroll.

Ignoring the out-of-pocket maximum. This number is your protection against financial disaster. A plan with a very high out-of-pocket maximum is a plan that could cost you tens of thousands of dollars in a bad year.

Assuming all silver plans are equal. Even within the same metal tier, plans vary significantly in premiums, deductibles, copay amounts, and network coverage. Always compare the specific plan details, not just the tier.

Not checking your prescriptions. Drug formularies vary between plans. A medication that costs you $20 on one plan might cost $150 on another, or might not be covered at all on a third. This can matter enormously for anyone managing a chronic condition.

When to Compare Health Insurance Plans

You can compare health insurance plans during the annual open enrollment period, which typically runs from early November through mid-January for marketplace coverage. Coverage purchased during this window starts on January 1.

Outside of open enrollment, you can compare and switch plans if you experience a qualifying life event: losing job-based coverage, getting married or divorced, having a baby, moving to a new area, or aging off a parent’s plan at 26.

If you get coverage through an employer, your enrollment period is typically set by the company, usually in the fall for the following calendar year.

Free Tools to Help You Compare Health Insurance

You do not have to do all of this manually.

Healthcare.gov lets you compare ACA marketplace plans side by side, enter your income to see subsidy eligibility, and check which plans are available in your ZIP code.

Your state’s health insurance marketplace (if you live in a state with its own exchange) offers similar tools with state-specific plan options.

Licensed insurance brokers can help you compare health insurance plans across multiple carriers and are typically paid by the insurer, so there is no direct cost to you for their help.

The KFF Subsidy Calculator helps you estimate what you might pay for a marketplace plan after premium tax credits based on your income and household size.

Bottom Line

Knowing how to compare health insurance plans properly is one of the most valuable financial skills you can develop. The difference between picking the wrong plan and the right one can be thousands of dollars in a single year.

Start with the five key numbers: premium, deductible, copay, coinsurance, and out-of-pocket maximum. Use the total annual cost formula. Check your network. Verify your prescriptions. And think honestly about how much healthcare you actually use.

The right plan for you is not the cheapest plan on the list. It is the plan that fits your health needs and your budget together, with the out-of-pocket maximum giving you a safety net if the unexpected happens.

Take your time, run the numbers, and pick based on the full picture. Your future self will thank you.

Fiscible helps everyday people make smarter financial decisions with clear, honest information. This article is for educational purposes only and does not constitute professional insurance or financial advice. Always consult with a licensed insurance professional for guidance specific to your circumstances.

One thought on “HOW TO COMPARE HEALTH INSURANCE PLANS IN 2026: A SIMPLE GUIDE THAT ACTUALLY MAKES SENSE”