Getting a quote on medical insurance sounds straightforward. You enter your zip code, answer a few questions, and boom, a number shows up on your screen. But here is the thing most people miss: that number is just the starting point. Understanding what that quote actually means, and whether the plan behind it is worth your money, is a whole different conversation.

This guide walks you through exactly how to get a quote on medical insurance in 2026, what factors affect the price you see, how to compare quotes the right way, and what mistakes to avoid so you do not end up with a plan that looks cheap but leaves you with massive bills.

Why Getting a Quote on Medical Insurance Feels So Complicated

Most people searching for a quote on medical insurance are not confused by the technology. They are confused by the language. Words like premium, deductible, out-of-pocket maximum, copay, and coinsurance all get thrown around on every quote comparison page, and if you do not know what those terms mean, the numbers are basically useless.

Here is a quick breakdown before we go further:

Premium is what you pay every month, no matter what. Even if you never see a doctor that month, you owe the premium.

Deductible is what you pay out of pocket before your insurance starts covering most costs. If your deductible is $3,000, you pay the first $3,000 of medical bills each year yourself.

Out-of-pocket maximum is the most you will ever pay in a given year. Once you hit that ceiling, insurance covers 100% of covered services.

Copay is a flat fee you pay for a specific service, like $30 every time you visit your primary care doctor.

Coinsurance is the percentage you pay after meeting your deductible. If your coinsurance is 20%, you pay 20% and insurance pays 80%.

Once you understand these five terms, a quote on medical insurance actually starts making sense.

Where to Get a Quote on Medical Insurance in 2026

There are a few reliable ways to pull quotes, and each one has its own advantages.

HealthCare.gov / State Marketplace If you are not covered through an employer and you want ACA-compliant plans with potential subsidies, the federal or your state marketplace is the best place to start. You can get a quote on medical insurance here and see instantly whether you qualify for premium tax credits based on your income. The out-of-pocket maximum for ACA individual plans in 2026 is capped at $9,100.

Directly Through an Insurance Company Most major insurers, including UnitedHealthcare, Blue Cross Blue Shield, Aetna, and Cigna, let you get a quote on medical insurance directly on their website. This is useful if you already know which company you prefer or want to see plans that may not appear on the marketplace.

Insurance Quote Comparison Sites Sites like SmartFinancial, InsuranceQuotes, and Quote.com pull multiple quotes in one place. These tools are convenient and can show you a range of options side by side. That said, make sure you are comparing the same coverage level across plans so the comparison is actually apples to apples.

Independent Insurance Brokers A licensed broker can pull a quote on medical insurance from multiple carriers and walk you through the differences. Brokers are paid by the insurance companies, not by you, so this option costs you nothing extra.

What Affects Your Medical Insurance Quote

When you request a quote on medical insurance, the price you see is calculated based on several personal factors.

Age is the biggest driver. Older applicants pay more. Under ACA rules, insurers can charge older adults up to three times more than younger adults for the same plan.

Location matters a lot too. Healthcare costs vary significantly by state and even by county. A plan in rural Kansas costs very differently from the same coverage tier in New York City.

Tobacco use can raise your medical insurance quote by up to 50% on ACA plans in states that allow tobacco surcharges.

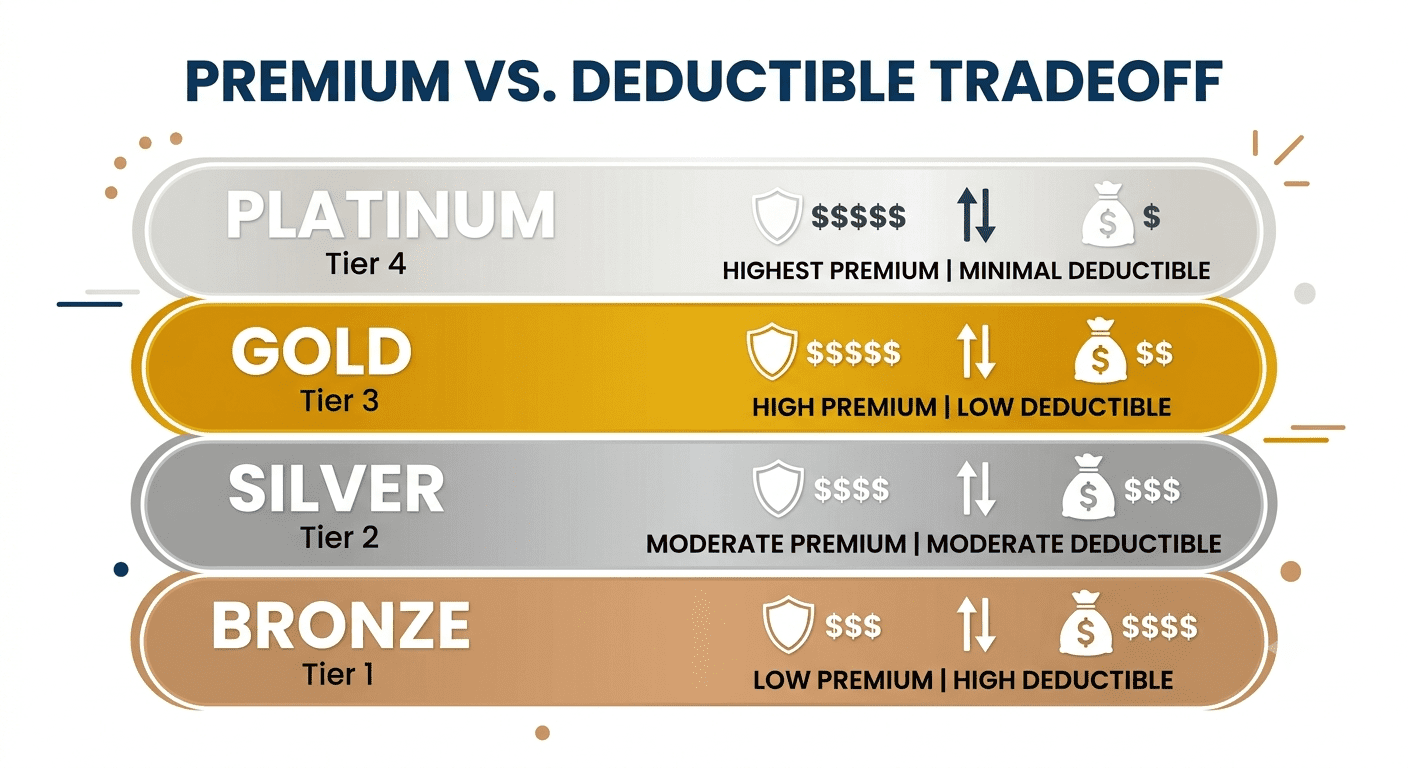

Plan tier is your call. Bronze plans have the lowest premiums but the highest deductibles. Silver plans sit in the middle. Gold and Platinum plans have higher monthly premiums but much lower costs when you actually use care.

Household size and income determine whether you qualify for subsidies through the marketplace. If your income falls between 100% and 400% of the federal poverty level, you may qualify for significant premium tax credits that reduce your monthly quote on medical insurance substantially.

How to Compare Medical Insurance Quotes the Right Way

Getting multiple quotes on medical insurance is the easy part. Comparing them properly is where most people go wrong.

Do not just look at the premium. A plan with a $250/month premium and a $7,000 deductible might cost you far more than a $400/month plan with a $1,500 deductible, especially if you have regular prescriptions, see specialists, or manage a chronic condition.

Calculate your total potential cost. Add up 12 months of premiums, then think about how much healthcare you realistically used last year. Add expected out-of-pocket costs. The plan with the lowest total annual cost for your specific usage is the winner, not the plan with the lowest quote on medical insurance at first glance.

Check the network. If your current doctor is not in a plan’s network, you will pay significantly more to keep seeing them, or you will have to switch providers entirely. Before you commit to any quote on medical insurance, run your preferred doctors through the insurer’s online provider directory.

Look at prescription drug coverage. Every plan has a formulary, which is a list of covered medications. If you take a specific drug, verify it is covered at a reasonable tier before choosing a plan.

Review what preventive care costs. Under ACA plans, most preventive services like annual checkups, screenings, and vaccinations are covered at $0 cost to you, even before you meet your deductible. This is worth confirming with any quote you are seriously considering.

Average Cost of Medical Insurance in 2026

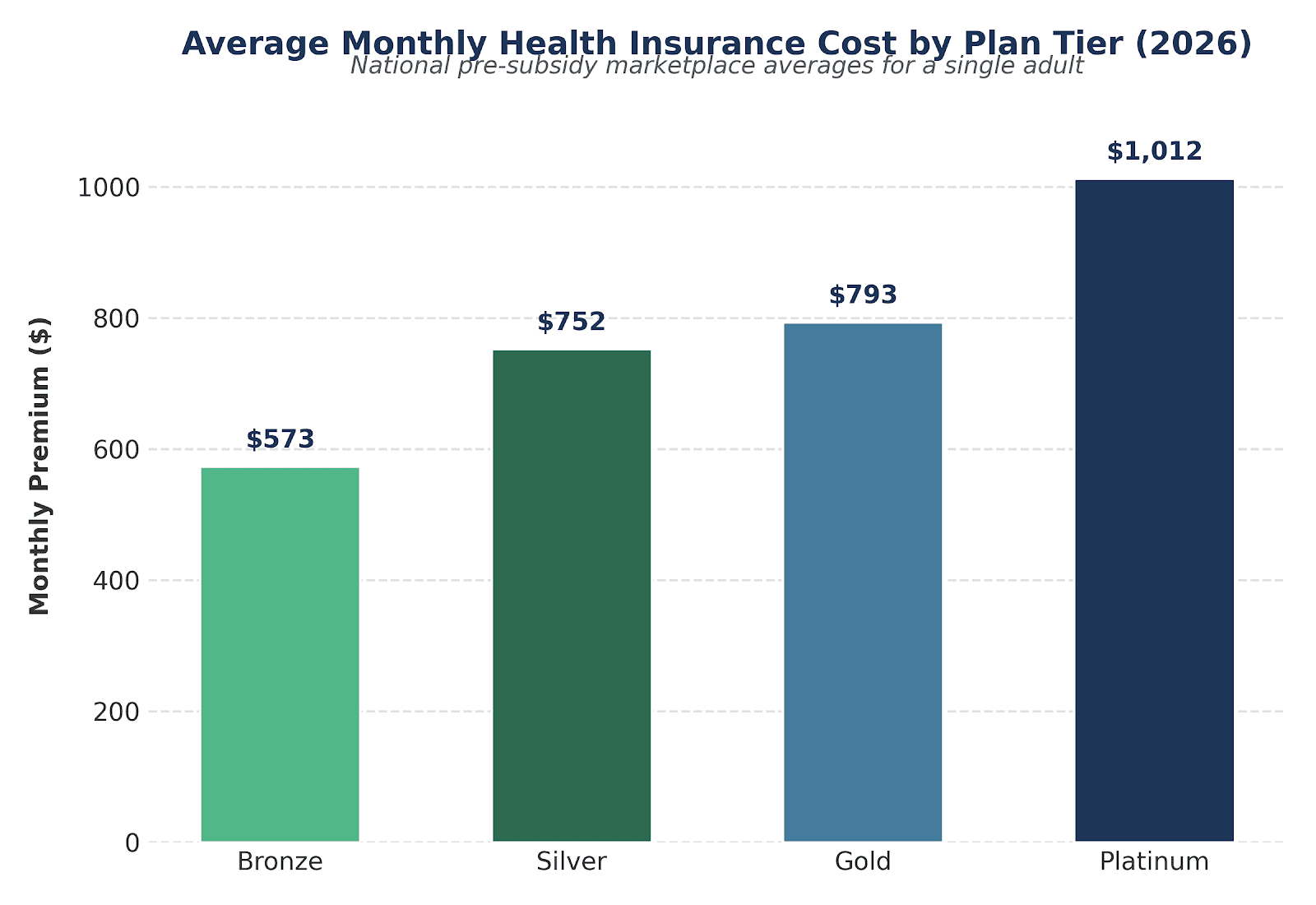

To give you a ballpark, the average monthly premium for a single adult on a Silver ACA plan is roughly $475 to $550 before any subsidies. For a family, you can expect anywhere from $1,200 to $1,800 per month, again before financial assistance.

However, if you qualify for premium tax credits, your actual quote on medical insurance can drop dramatically. Some households with incomes around 150% of the federal poverty level pay less than $10 per month for a Silver plan.

For employer-sponsored coverage, the average employee contribution for a single plan hovers around $115 to $130 per month in 2026, with employers picking up the rest of the cost.

Common Mistakes People Make When Getting a Medical Insurance Quote

Mistake 1: Only looking at the premium. Already covered above, but it is worth repeating because it is the most common and most costly mistake.

Mistake 2: Not checking subsidy eligibility. Millions of people pay full price for a medical insurance quote without realizing they qualify for significant financial help. Always run your income through the HealthCare.gov calculator before ruling out marketplace plans.

Mistake 3: Skipping short-term plans without understanding the tradeoffs. Short-term medical insurance quotes are often much cheaper, but these plans do not cover pre-existing conditions, do not meet ACA standards, and can leave you exposed to very large bills.

Mistake 4: Not re-shopping during open enrollment. Insurance plans and pricing change every year. If you have not gotten a fresh quote on medical insurance during the most recent open enrollment period, you may be overpaying or missing better coverage options that are now available.

Mistake 5: Ignoring the out-of-pocket maximum. This number is your financial safety net. A plan with a very high out-of-pocket maximum could expose you to tens of thousands in costs if you have a serious illness or accident.

When Can You Get a Quote on Medical Insurance?

You can get a quote on medical insurance at any time. But you can only enroll in an ACA marketplace plan during Open Enrollment, which typically runs from November 1 through January 15 for coverage starting January 1.

Outside of that window, you can still enroll if you have a qualifying life event. These include losing job-based coverage, getting married or divorced, having a baby, moving to a new coverage area, or turning 26 and aging off a parent’s plan. These trigger a Special Enrollment Period that gives you 60 days to get a quote and sign up for a plan.

Final Thoughts

Getting a quote on medical insurance is genuinely easier today than it has ever been. But a quote is only useful if you know what you are looking at. Take the time to understand the full cost structure of any plan before you commit. Check the network. Run the numbers based on your actual healthcare usage. And always check whether you qualify for subsidies before assuming you cannot afford marketplace coverage.

A little research upfront can save you hundreds or even thousands of dollars over the course of a year. That is worth 30 minutes of your time.

Looking for more help navigating health insurance? Check out our guides on how to compare health insurance plans and how to choose the right plan for your budget on fiscible.com.