If you live in the Upper Midwest and you are shopping for health insurance, Medica is a name you have definitely come across. But is Medica insurance actually good? What does it cover? Who is it right for? And how does it stack up against the competition in 2026?

This is a full, honest look at Medica insurance, covering their plan types, costs, network, pros and cons, and everything you need to make an informed decision.

What Is Medica Insurance?

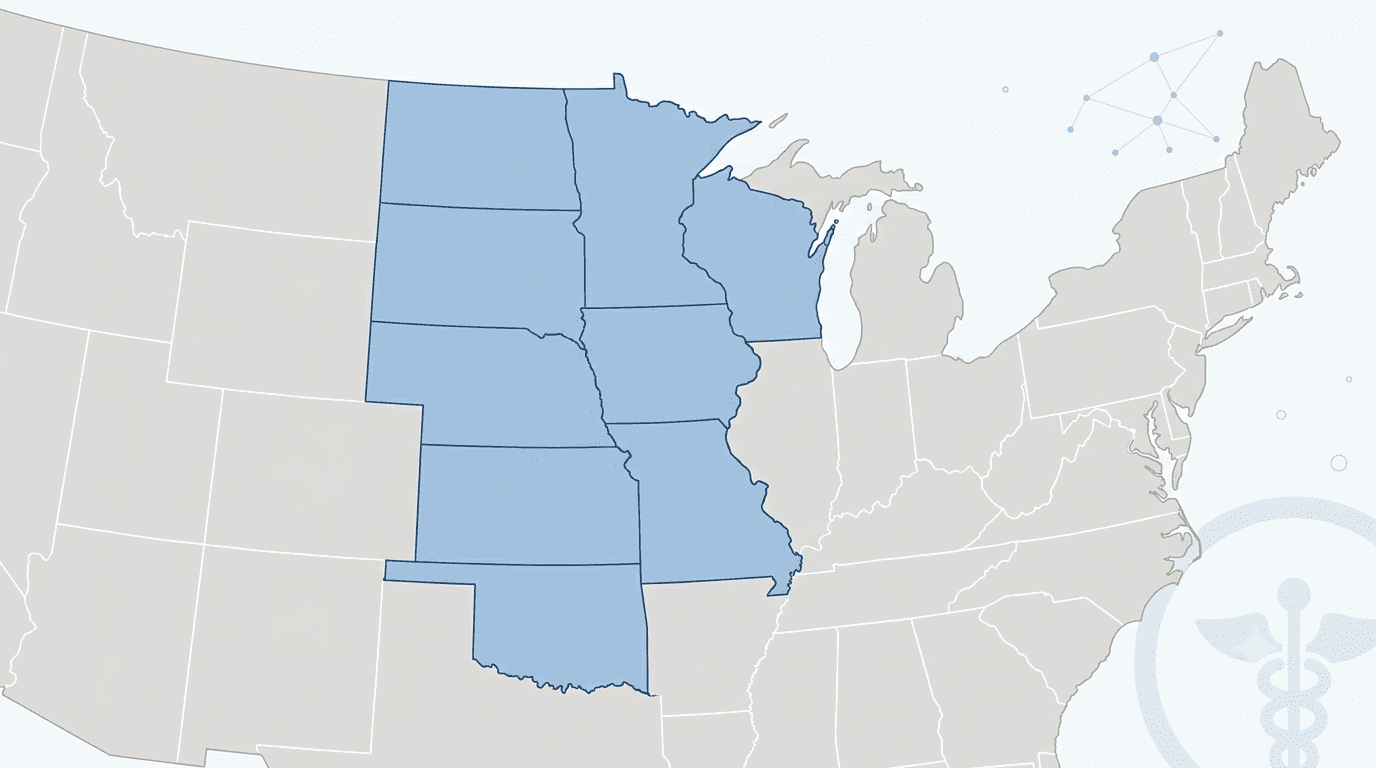

Medica is a nonprofit health services company headquartered in Minnetonka, Minnesota. It has been operating since 1974 and primarily serves individuals, families, and employers in the Upper Midwest, including Minnesota, Iowa, Kansas, Missouri, Nebraska, North Dakota, Oklahoma, South Dakota, and Wisconsin.

As a nonprofit, Medica insurance operates differently from publicly traded insurers. Surplus revenue is reinvested into coverage, member services, and community health programs rather than distributed to shareholders. That is not just marketing language. It affects how the company makes decisions around coverage and pricing.

In 2026, Medica insurance became even more significant in the Minnesota market after agreeing to assume more than 300,000 UCare members as UCare winds down its Individual and Family plans and Medicaid operations. This transition positions Medica as one of the most important health coverage providers in Minnesota for the foreseeable future.

What Plans Does Medica Insurance Offer?

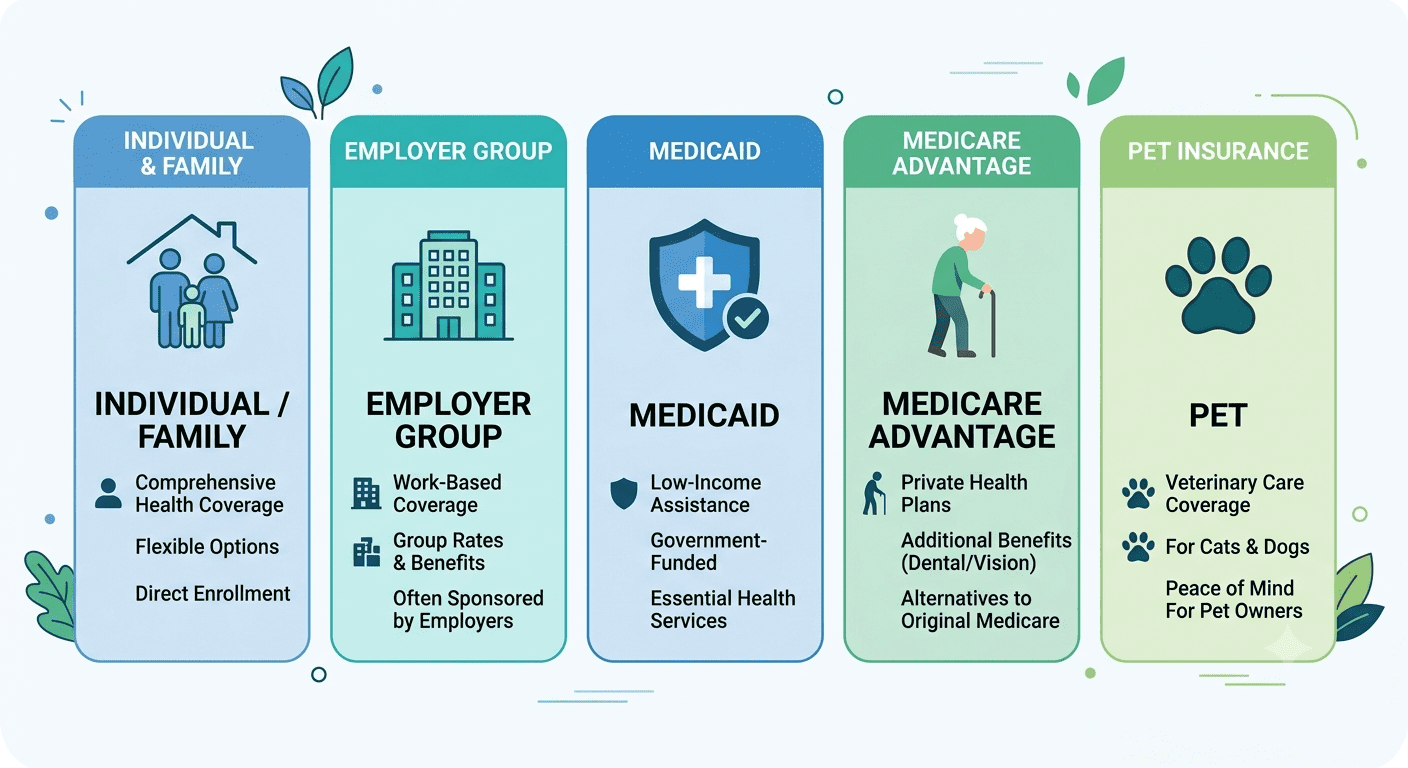

Medica insurance offers a fairly comprehensive range of plans across several coverage types.

Individual and Family Plans These are the ACA-compliant marketplace plans most people are looking for when they shop Medica insurance. They are available in Bronze, Silver, and Gold tiers, with varying deductibles and premiums depending on the network and coverage level. Medica individual plans include the full set of ACA-mandated essential health benefits, including preventive care, mental health coverage, maternity care, emergency services, prescription drugs, and more.

Employer Group Plans Medica insurance offers fully-insured and self-funded group plan options for businesses of various sizes. These plans come with access to care management tools, wellness programs, and a tiered network structure designed to help employers manage costs.

Medicaid Plans Medica has a long history of managing Medicaid coverage in Minnesota, and their agreement to absorb UCare’s Medicaid members in 2026 expands this role significantly.

Medicare Advantage Insurance offers Medicare Advantage plans for adults 65 and older in their service area. These plans often include extra benefits beyond original Medicare, such as dental, vision, and fitness programs.

Pet Insurance Yes, Medica insurance actually offers pet health coverage. It is not their flagship product, but for pet owners in their service area, it is a convenient add-on.

Medica Insurance Plan Costs in 2026

Let us talk real numbers, because that is what actually matters when you are evaluating this insurance.

For individual ACA plans in Minnesota, Insurance Silver-tier EPO plans are ranked among the best available by MoneyGeek’s 2026 analysis of premiums, deductibles, and out-of-pocket maximums across all age groups. The gap between the cheapest and most expensive Silver plan for a 40-year-old in Minnesota is about $56 per month, which amounts to $672 per year. That difference matters, and it generally sits in a competitive range.

Typical Medica insurance deductible ranges for 2026:

For in-network Individual plans: some medica plans start with deductibles as low as $300 per individual, while higher-deductible options can reach $6,350 per individual.

For family plans: in-network deductibles range from around $900 to $12,700 depending on the tier.

Out-of-pocket maximums for in-network coverage range from $5,000 per individual to $6,350, with family out-of-pocket maximums reaching up to $12,700. The insurance plans generally do not impose an out-of-pocket maximum for out-of-network services, which is worth knowing if you travel frequently or live in areas with limited in-network provider choices.

For HSA-compatible plans, Medica offers a $0 virtual urgent care benefit once you meet your deductible, which is a genuinely useful feature for members who want to manage minor health issues without a costly in-person visit.

Medica Insurance Provider Networks

One of the most important things to understand about any Medica insurance plan is the network structure. Medica uses several broad regional networks that vary depending on where you live and which plan you choose.

In 2026, some Medica plans in Minnesota are offered in partnership with specific health systems. For example, plans labeled “Bold by M Health Fairview and Medica” connect you to the M Health Fairview network, while “North Memorial Acclaim by Medica” plans are built around the North Memorial Health network.

This tiered, provider-tied network approach is designed to lower costs by keeping care within specific systems. The tradeoff is that if your preferred doctor or specialist is not in the specific network tied to your Medica insurance plan, you may need to switch providers or pay significantly more.

Before enrolling in any Medica insurance plan, visit Medica.com or use the MNsure Plan Comparison Tool to verify that your current doctors accept the specific network tied to the plan you are considering. This step is non-negotiable if keeping your existing care team matters to you.

What Do Real Members Say About Medica Insurance?

Customer reviews of Medica insurance are, as with most health insurers, genuinely mixed.

On the positive side, many members praise Medica insurance for its competitive premiums, straightforward enrollment process, and accessibility of customer service during business hours. For straightforward medical needs, many policyholders report their Medica insurance coverage works as expected.

On the negative side, some Iowa members filed public comments with the Iowa Insurance Division regarding a proposed 26.8% rate increase for 2026, calling it unsustainable and disproportionate. Some Minnesota members starting new Medica plans in early 2026 reported difficulties receiving their plan documentation and benefits information promptly, leading to BBB complaints.

This reflects a broader reality about Medica insurance: the company is managing significant growth following the UCare transition and absorbing over 300,000 new members. Growing pains at that scale are not uncommon, but it does mean that 2026 is a particularly important year to be proactive about verifying your coverage details if you are a new or transitioning Medica insurance member.

Pros and Cons of Medica Insurance

The Pros

Medica insurance is a nonprofit, which shapes how it approaches member services and reinvests surplus. This matters in the long run.

For healthy adults who do not expect to use a lot of care, Medica’s high-deductible, low-premium plans are an excellent value. They keep your monthly cost manageable while still protecting you from catastrophic expenses.

Medica insurance consistently earns recognition as one of the best EPO plan providers in Minnesota, according to MoneyGeek’s analysis. Their network partnerships with major Minnesota health systems give members access to high-quality facilities.

The company offers HSA-compatible plans, telehealth benefits, and wellness programs that add real value beyond just basic coverage.

The Cons

Medica insurance is geographically limited. If you live outside the Upper Midwest, Medica is simply not available to you.

Out-of-network coverage is limited and, in many cases, has no out-of-pocket maximum, meaning very high costs if you receive care outside your plan’s network.

The rate increases in some states, particularly Iowa, have been steep entering 2026. If affordability is your primary concern, it is worth comparing Medica insurance against all available plans in your area before committing.

Customer service experiences vary, and the UCare transition has added some administrative strain to the company in 2026.

Who Should Consider Medica Insurance?

Medica insurance is a strong choice for the right consumer in the right situation.

You are a good fit for Medica insurance if:

You live in Minnesota, Iowa, Wisconsin, or another state in Medica’s service area. Geographic eligibility is the first filter.

You are generally healthy and want a low-premium plan with a higher deductible to keep your monthly cost down. Medica’s high-deductible plans are built for this use case.

You prefer a nonprofit insurer that reinvests in member programs rather than a publicly traded company with shareholder obligations.

You or your family were previously covered by UCare and are transitioning to Medica insurance. Your coverage should continue seamlessly, and you can visit Medica.com or call to verify your specific plan details.

Medica insurance may not be the best fit if:

You live outside the Upper Midwest. Check marketplace options in your area.

You have complex ongoing healthcare needs and prioritize network flexibility. Medica’s provider-tied network plans can limit which doctors you can see affordably.

You are on a tight budget and Medica’s 2026 premium increases in your state have pushed it out of your comfortable range. Always compare available options on HealthCare.gov or your state marketplace before settling.

How to Enroll in Medica Insurance

You can enroll in a Medica insurance individual or family plan during Open Enrollment, which typically runs from November 1 through January 15. You can shop plans at Medica.com/ShopMNPlans or through your state marketplace.

If you are transitioning from UCare, no immediate action is required for your 2026 coverage to continue. Medica has confirmed that UCare members’ premiums, benefits, and networks remain the same as described during the transition period.

For employer group plans, your HR department or a licensed broker can walk you through Medica insurance group options.

If you qualify for Medicaid, you can enroll at any time through your state’s Medicaid office.

Final Verdict on Medica Insurance

Medica insurance is a solid, well-established nonprofit insurer that genuinely competes at the top tier of coverage options in the Upper Midwest. For healthy individuals looking for affordable monthly premiums, for families in Minnesota and surrounding states, and for anyone transitioning from UCare coverage, Medica insurance deserves serious consideration in 2026.

That said, do the homework. Check the specific network tied to the plan you are considering. Run your doctors through the provider directory. Compare the total annual cost, not just the monthly premium. And if you are in a state where Medica has proposed significant rate increases, make sure you are comparing it against every available option before you enroll.

Health insurance is one of the most consequential financial decisions you make every year. Medica insurance is a strong player, but the best plan is always the one that fits your specific needs, budget, and healthcare situation.

Explore more insurance guides on fiscible.com to compare your options and make smarter health coverage decisions in 2026.