Learn zero-based budgeting and how to calculate your take-home pay accurately. Step-by-step guide with real examples, tax breakdowns, and actionable strategies for 2026.

Zero-Based Budgeting & Take-Home Pay Guide

Your Money in 2026:

Money struggles don’t start with bad math-they start because nobody teaches you the foundations.

Two paychecks look the same on paper. One person takes home $3,200. Another takes home

$3,950. Both earn $60,000 a year. The difference? Understanding zero-based budgeting and

knowing exactly what your take-home pay actually is.

This guide covers both. By the end, you’ll know exactly where every dollar of your paycheck goes,

and you’ll have a system that actually works when life gets unpredictable.

What Is Zero-Based Budgeting?

Zero-based budgeting (ZBB) is a planning method where you assign every dollar of income to a

specific purpose before the month starts. The goal:

Income – Expenses = $0

This doesn’t mean your bank account hits zero. It means every dollar has a job: rent, groceries,

savings, debt repayment, or a night out. Nothing gets spent by accident.

The method was created by Peter Pyhrr at Texas Instruments in the early 1970s as a way to justify

business spending. Since then, it’s become popular in personal finance because it works-especially

when combined with knowing your actual take-home pay.

The Core Principle

Traditional budgeting starts with last year’s spending and increments from there. Zero-based

budgeting starts from zero each month and asks: “What do I actually need this month?” It forces

intentional decisions.

How Zero-Based Budgeting Works: The 5-Step Process

Step 1: List Your Monthly Take-Home Income

Start with money actually deposited to your account-not gross salary.

Example: $60,000 annual salary = roughly $3,950/month take-home (we’ll explain the gap shortly).

Include:

Regular paychecks (after taxes)

Side hustle income

Freelance income

Bonuses (only if guaranteed)

If your income varies, use your lowest month from the last 12 months as your planned income.

Budget any surprise income next month.

Step 2: List Your Fixed Expenses

Fixed expenses stay the same every month:

Rent or mortgage

Insurance (auto, health, life)

Utilities (usually)

Minimum debt payments

Subscriptions you keep

Add them up. This is your baseline.

Step 3: Allocate to Variable Expenses

Variable expenses change month to month:

Groceries

Gas

Dining out

Entertainment

Clothing

Look at last 3 months of spending. Be realistic. If you actually spend $300 on coffee and dinners,

budget $300-not $100.

Step 4: Plan Your Savings & Goals

Give every dollar a job:

Emergency fund (start with $1,000, then 3-6 months expenses)

Retirement contributions

Goals (vacation, car, home)

Debt payoff

Step 5: Do the Math

Income – (Fixed + Variable + Savings) = $0

If you have money left over, you can increase savings or reallocate. If you’re short, cut variable

expenses or find income sources in Zero-Based Budgeting & Take-Home Pay

The key: Redo this every month. Adjust for the actual month ahead.

Why Knowing Your Take-Home Pay Matters for Budgeting

Here’s the thing most Zero-Based Budgeting & Take-Home Pay guides skip: you can’t budget with numbers that aren’t real.

If you earn $60,000 and budget as if you take home $5,000/month, you’ll overspend by $1,000

every month. That’s not a character flaw-it’s a math problem.

Let’s break down where the money actually goes by Zero-Based Budgeting & Take-Home Pay:

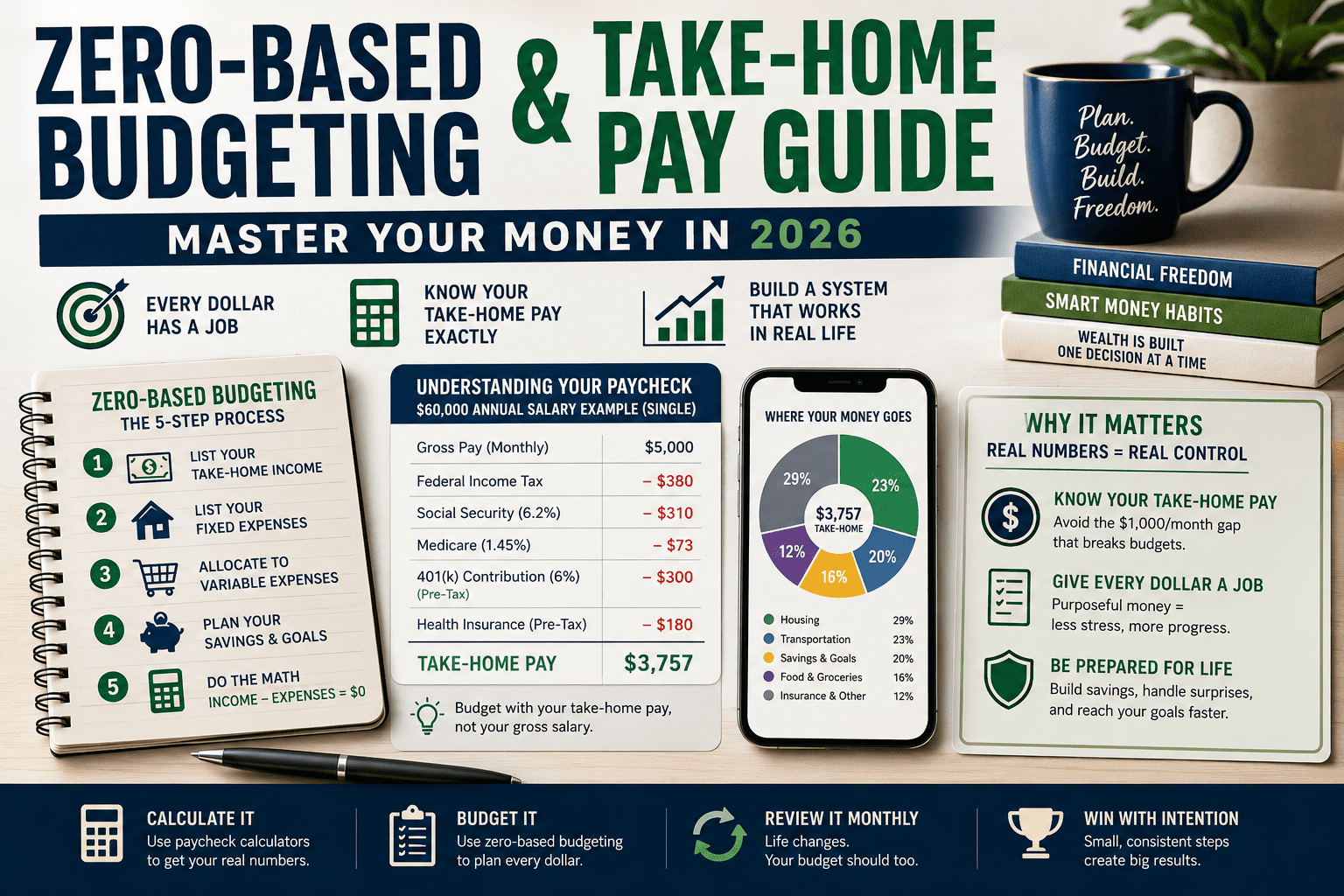

Understanding Your Paycheck: The Take-Home Pay

Breakdown

Gross Pay vs. Net Pay

Gross pay = total earnings before anything comes out. Net pay (take-home) = what actually hits

your account.

On a $5,000/month gross salary:

Federal income tax: ~$380

Social Security tax: ~$310 (6.2%, capped at $184,500 annual earnings)

Medicare tax: ~$73 (1.45%, no cap)

Pre-tax deductions (401k, health insurance, FSA): ~$150-400

Take-home: ~$3,750-4,000

The gap is shocking the first time you see it, but it’s where most people get budgeting wrong.

Federal Income Tax Withholding

Federal income tax is withheld based on your W-4 form. Your employer estimates what you’ll owe

on April 15 and withholds that amount throughout the year.

2026 federal tax brackets (single filer):

12% on income $12,400–$50,400

22% on income $50,400–$105,700

24%, 32%, 35%, 37% on higher brackets

Important: Your marginal rate (highest bracket) is not your effective rate (average rate on all

income).

Example: Earning $60,000 (single):

You might think you’re in the 22% bracket

Your actual effective rate is closer to 10.5%

Why? Because the first $12,400 is taxed at 10%, the next chunk at 12%, then 22% on the

remainder

Social Security & Medicare (FICA)

Zero-Based Budgeting & Take-Home Pay

FICA taxes are split 50/50 between you and your employer:

Social Security: 6.2% (stops once you earn $184,500/year)

Medicare: 1.45% (no cap, plus 0.9% additional if you earn over $200k)

On a $60,000 salary: ~$383/month in FICA taxes.

Pre-Tax Deductions (401k, Health Insurance, FSA)

Money deducted before income tax is calculated:

401(k) contributions (reduce both income tax and FICA)

Health insurance premiums

HSA or FSA contributions

Commuter benefits (transit, parking)

Life insurance (sometimes)

Example: If you contribute $500/month to your 401(k):

Your gross stays $5,000

But your taxable income drops to $4,500

You save federal income tax on that $500 (~$110 assuming 22% bracket)

That’s why 401(k) contributions reduce your tax bill

Post-Tax Deductions

Deducted after income tax is calculated:

Roth 401(k) contributions

Child support or wage garnishments

Some union dues

Life insurance (sometimes)

These don’t reduce your income tax-you pay tax on the full amount, then it comes out.

State & Local Taxes

Nine US states have zero income tax: Alaska, Delaware, Florida, Nevada, South Dakota,

Tennessee, Texas, Washington, Wyoming. If you live elsewhere, state taxes range from 2-13%.

In a high-tax state like California (13.3%), a $60,000 salary loses an extra $650/month.

Real-World Paycheck Examples

Single Employee, No Side Income

Gross monthly: $5,000 Breakdown:

Federal income tax: -$380

Social Security: -$310

Medicare: -$73

401(k) (6%, pre-tax): -$300

Health insurance (pre-tax): -$180

Take-home: $3,757

For a zero-based budget, plan around $3,750.

Dual Income, One 401(k) Maxed Out

Two people, $60,000 each:

Person A (maxing 401k): $2,950/month take-home

Person B (standard): $3,757/month take-home

Household take-home: $6,707/month

When you’re combining incomes for a household budget, add both take-home amounts. This is

where couples often trip up-they budget on gross ($10,000) instead of net ($6,707).

Freelancer with Variable Income

Month 1: $6,000 income Month 2: $2,500 income Average: $4,250/month

For zero-based budgeting, plan on $2,500 (lowest month). Anything above is buffer or next month’s

savings. This is critical for freelancers-use the low month, not the average.

Zero-Based Budgeting & Take-Home Pay vs. Other Methods

50/30/20 Rule

Allocate 50% to needs, 30% to wants, 20% to savings/debt.

Problem: Most people spend more than 50% on needs. In expensive cities, housing alone is 40-50%.

ZBB advantage: Your actual numbers. If needs are 65%, wants 20%, savings 15%-that’s fine.

Adjust monthly.

Traditional Budgeting

Set a budget once, adjust incrementally year-over-year.

Problem: Doesn’t account for life changes (new job, move, family). Gaps accumulate.

ZBB advantage: Monthly resets mean you’re always aligned with reality.

Zero-Based Budgeting & Take-Home Pay:

Envelope System

Physical cash divided into labeled envelopes (groceries, entertainment, etc.).

Connection to ZBB: The envelope system is a tool for executing ZBB, not a separate method. You can do ZBB with envelopes or with a budgeting app.

Common Zero-Based Budgeting & Take-Home Pay Mistakes (and How to Fix Them)

Mistake 1: Not Accounting for Irregular Expenses

Car registration, annual insurance, gifts, and holidays don’t appear monthly, so people skip them in

their budget. Then December hits and they’re shocked.

Fix: List annual irregular expenses, divide by 12, and put that amount in savings each month.

Example: $1,200 annual car registration = $100/month set aside.

Mistake 2: Over-Withholding Federal Tax

If you’re getting a $3,000 refund, you’ve been giving the IRS an interest-free loan all year.

Fix: Fill out a new W-4 with your employer. The IRSW-4calculator shows exactly how many

allowances you need.

Mistake 3: Forgetting Pre-Tax Deductions in Your Calculation

You’re told your salary is $60,000, but if you contribute $3,000/year to FSA or HSA, your actual

taxable income is $57,000.

Fix: Ask your HR for your actual take-home after all deductions. Use a SmartAssetpaycheck

calculator to model it out first.

Mistake 4: Planning on Average Income (Freelancers)

You made $60,000 last year but had months with $2,000 and months with $12,000.

Fix: Budget using your lowest month. Build a buffer with extra income. Once you have 3 months of

expenses saved, you can plan on average.

Mistake 5: Forgetting the Monthly Reset

You budgeted in January, life happened, and now it’s March-same budget. Life changes. Car breaks

down. New subscription. Bonus arrives.

Fix: Spend 20-30 minutes every month (Sunday evening works) redoing your budget for the month

ahead.

Tools That Help With Zero-Based Budgeting & Take-Home Pay

Calculation

For take-home pay calculation:

ADP Salary Calculator – accurate federal and state taxes

SmartAsset Paycheck Calculator – shows tax breakdown by state

PaycheckCity – includes deductions and benefits

EveryDollar – Zero-based built-in, pairs with budgeting philosophy

YNAB (You Need A Budget) – Forces awareness of where money goes

Monarch Money – Modern approach with goal tracking

Spreadsheet – Simple Google Sheets template (free, customizable)

Start with a calculator to find your real take-home, then pick a budgeting app that feels natural.

The Timeline: When Will This Feel Normal?

Month 1: You’re learning. Spending feels restrictive. You overshoot some categories.

Month 2: Patterns emerge. You know where the leaks are. Adjustments feel easier.

Month 3: This is the pivot. ZBB becomes automatic. You’re making conscious choices, not

scrambling.

Most people reach proficiency in 3 months. Stick with it.

Try Fiscible for Zero-Based Budgeting & Take-Home Pay

Fiscible breaks down exactly what you need to know about budgeting, taxes, and personal finance-

without the jargon. Whether you’re starting zero-based budgeting or diving deeper into how take-

home pay works, their guides walk through every step with real examples and tools you can use

today. Pick one thing from this guide and do it today. One action beats ten plans sitting in your

notes app.