Struggling with debt? This guide breaks down the fastest, most practical ways to pay off debt in 2026, including the snowball and avalanche methods, consolidation tips, and real budgeting tricks that work on any income.

Getting serious about debt is the first step to financial freedom.

Let’s be real. Debt has a way of sitting on your chest like a weight you can’t shake. You make your minimum payments every month, and somehow the balance barely moves. You know something has to change, but you’re not sure where to start.

You’re not alone. According to recent data, the average American household carries over $100,000 in total debt when you factor in mortgages, credit cards, student loans, and auto loans. But here’s what most people don’t realize: debt is not a life sentence. With a clear plan and some discipline, you can pay it off faster than you think.

This guide walks you through the exact strategies that work in 2026, from the classic debt snowball and avalanche methods to lesser-known tactics like negotiating your interest rates and using windfalls wisely.

Why Most People Stay Stuck in Debt

Before jumping into solutions, it helps to understand why debt tends to stick around.

The biggest reason is minimum payments. Credit card companies design minimum payments to be low on purpose. When you only pay the minimum, most of that money goes toward interest, not the actual balance. You could spend years paying on a $5,000 credit card and barely chip away at what you owe.

The second reason is lifestyle creep. As income goes up, spending tends to go up with it. Even people earning good salaries find themselves stretched thin because they upgraded their lifestyle along the way.

The third reason? No plan. People vaguely want to be debt-free but never sit down and build a real, written strategy. That changes today.

Step 1: Know Exactly What You Owe

This sounds obvious, but a lot of people avoid looking at the full picture. Facing your debt total can feel uncomfortable, but it is the only way to take control.

Sit down and list every single debt you have. Write down:

- The creditor name

- The current balance

- The interest rate (APR)

- The minimum payment

- The due date

Once it’s all on paper (or a spreadsheet), you have your starting point. No more guessing.

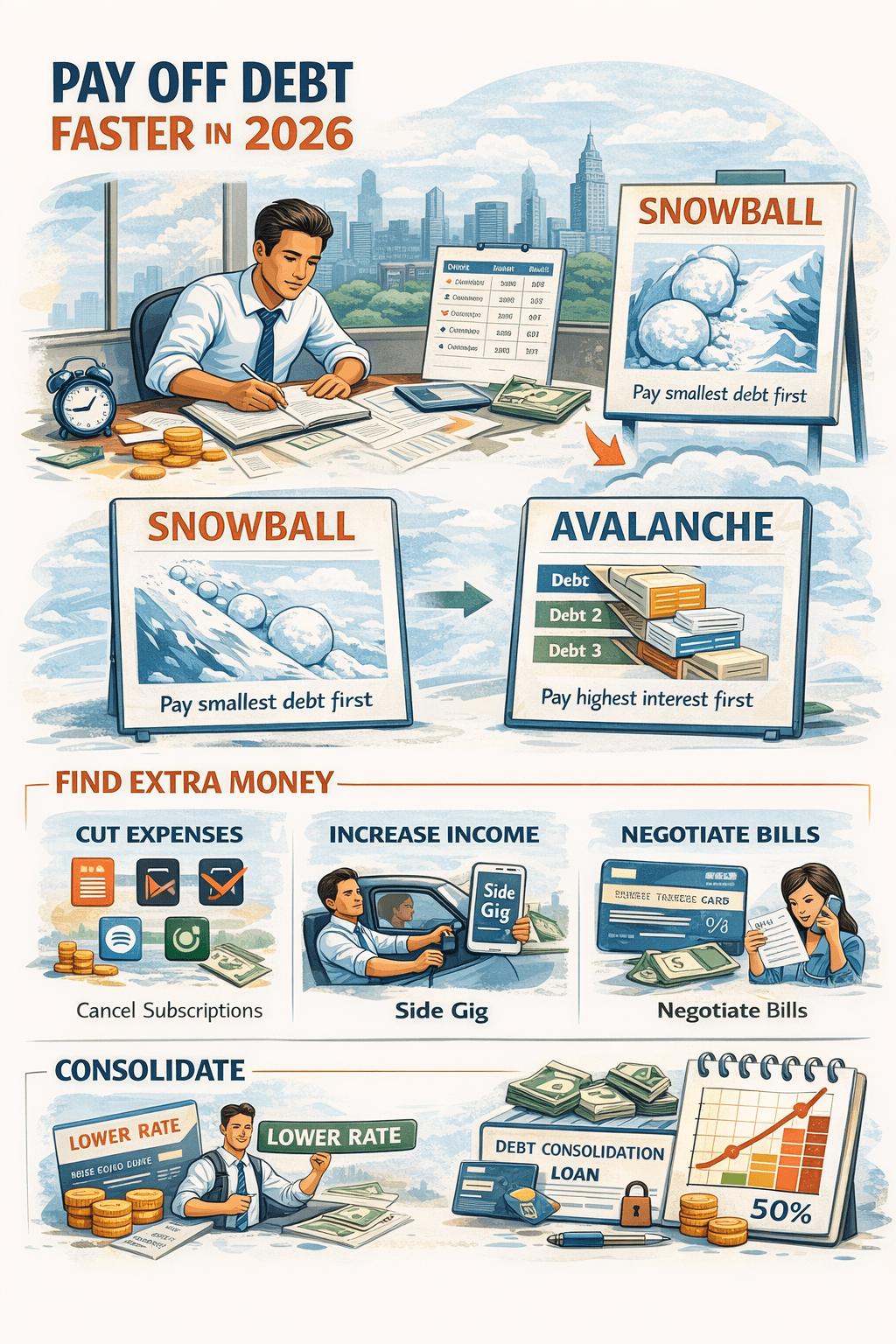

Step 2: Pick Your Payoff Strategy

There are two proven methods to pay off debt fast. Both work. The one you should choose depends on your personality.

The Debt Snowball Method

Made popular by personal finance expert Dave Ramsey, the snowball method works like this: you pay off your smallest balance first, regardless of interest rate. Once that’s gone, you roll that payment into the next smallest balance.

Why it works: It gives you quick wins. Paying off a small balance in a month or two creates momentum. That feeling of progress keeps you motivated to keep going.

Best for: People who struggle with motivation or have felt discouraged by debt before.

The Debt Avalanche Method

The avalanche method focuses on your highest interest rate debt first. You put every extra dollar toward the account with the highest APR while making minimum payments on everything else. Once that’s paid off, you move to the next highest rate.

Why it works: You pay less in interest overall, which means you get out of debt faster in terms of total time and total money spent.

Best for: People who are disciplined and motivated by math rather than emotional milestones. Neither method is wrong. Pick the one you will actually stick with.

Tracking your debt payoff progress makes a huge difference in staying consistent.

Step 3: Find Extra Money to Throw at Debt

Here’s where things get real. To pay off debt faster, you need more money going toward it each month. That means either cutting spending, increasing income, or both.

Cut the Obvious Stuff First

To pay off debt quickly, go through your last 30 days of spending. Look for subscriptions you forgot about, delivery fees you could avoid, or habits that are costing you more than you realize. Most people find $100 to

$300 in monthly spending they can redirect to debt without feeling much pain. Some quick wins:

- Cancel streaming services you barely use

- Cook at home three more nights per week

- Pause any non-essential subscriptions

- Cut back on coffee shop runs (this one adds up fast)

Negotiate Bills You Already Have

Call your credit card companies and ask for a lower interest rate. It sounds too simple to work, but it often does. If you have a decent payment history, customer service reps can often lower your APR by a few percentage points. That directly reduces how much interest you’re paying each month.

Also call your phone, insurance, and internet providers. Loyalty rarely rewards you in these industries. Threatening to cancel or mentioning a competitor’s price usually leads to a discount.

Increase Your Income

Even a small amount of extra income each month makes a significant difference when it goes straight to debt. Options to consider:

- Pick up a weekend side gig (delivery driving, freelancing, tutoring)

- Sell things you no longer use on Facebook Marketplace or eBay

- Ask for extra hours at work if that’s possible

- Use cashback apps and put those earnings toward your debt

One extra $200 per month on a $5,000 credit card balance at 22% APR could cut years off your payoff timeline.

Step 4: Consider Debt Consolidation

If you’re juggling multiple high-interest debts, consolidation might be worth looking at. The idea is to combine multiple balances into one account with a lower interest rate.

Balance Transfer Credit Cards

Many cards offer a 0% promotional APR for a period of 15 to 21 months. If you transfer a high-

interest balance to one of these cards and commit to paying it down before the promotional period ends, you can save a significant amount in interest.

You typically need a credit score in the mid-600s or higher to qualify. There’s usually a transfer fee of 3% to 5% of the balance, so make sure the math still works in your favor.

Debt Consolidation Loans

A personal loan at a lower interest rate can replace several high-rate debts and simplify your monthly payments into one. The key is making sure the new loan’s interest rate is genuinely lower than what you’re currently paying. Otherwise, you’re just rearranging the furniture.

A word of caution: Debt consolidation is only effective if you stop adding new debt after consolidating. If you consolidate and then run the credit cards back up, you’ll be in a worse position than before.

Step 5: Use Windfalls Strategically

Tax refunds, work bonuses, birthday money, or selling something you own can give your debt payoff a serious boost. The temptation is to spend these windfalls on something fun, and while there’s nothing wrong with treating yourself a little, putting even 80% of a windfall toward debt can move your timeline up significantly.

A $2,000 tax refund applied to your highest-interest debt is not boring. That’s months of progress in one move.

Every extra payment, big or small, moves you closer to being debt-free.

Step 6: Automate Your Payments

Set up autopay for at least your minimum payments on every account. This protects your credit score and removes the mental load of remembering due dates.

For your extra debt payments, set up an automatic transfer on payday to move money to your debt before you have a chance to spend it. The phrase “pay yourself first” usually applies to savings, but when you’re in debt payoff mode, paying your future self means getting out of debt now.

Step 7: Track Your Progress

A debt payoff tracker, whether on paper, in a spreadsheet, or through a budgeting app, gives you something to measure against. Watching your balance drop month by month is genuinely motivating.

Some people color in a progress bar on a sheet of paper. Others use apps. The method does not matter. What matters is that you can see you’re moving forward.

What About Debt Settlement and Bankruptcy?

These options exist, and there are situations where they make sense. But they come with serious consequences.

Debt settlement companies typically charge fees between 15% and 25% of your enrolled debt. They require you to stop making payments during the process, which destroys your credit score and can lead to lawsuits from creditors. Chapter 7 bankruptcy stays on your credit report for 10 years.

Chapter 13 for 7 years.

These are last resorts. If you’re considering them, speak with a nonprofit credit counseling agency first. They can help you evaluate options without the high fees.

Building a Life After Debt

Getting out of debt is not the finish line. It’s the starting line.

Once you’re debt-free, the same money you were sending to creditors can now go toward an emergency fund, retirement contributions, investments, or a home purchase. The financial freedom that comes from having no payments is hard to describe until you experience it.

But it starts with a list, a strategy, and a commitment to stick with it even when progress feels slow.

Quick Recap: Your Debt Payoff Action Plan

- List every debt with balance, APR, and minimum payment

- Choose the snowball or avalanche method based on your personality

- Find extra money by cutting spending and/or earning more

- Consider consolidation if you qualify for a meaningfully lower rate

- Put windfalls toward debt aggressively

- Automate payments so you never miss one

- Track your progress every month

The path to being debt-free is not complicated. But it does require you to start.

Want to understand how your take-home pay breaks down so you can budget better? Try the Take-Home Pay Calculator at Fiscible to see exactly where your money goes before you even touch it.

One thought on “HOW TO PAY OFF DEBT FAST IN 2026: A POWERFUL GUIDE THAT ACTUALLY WORKS”