Want to improve your credit score fast in 2026? This guide covers proven credit score tips, from reducing credit utilization to fixing errors on your credit report, so you can raise your score quickly and smartly.

Your credit score is one of those numbers that quietly controls a lot of your life. It decides whether you get approved for an apartment. It affects the interest rate on your car loan. It can even come up during job applications. And yet most people have no idea how their credit score actually works or what they can do to improve it.

If your credit score is not where you want it to be right now, you are not alone. Millions of Americans are in the same position. The good news is that your credit score is not permanent. It changes every month, and with the right moves, you can raise your credit score faster than you probably think.

This guide breaks down everything you need to know about how to improve your credit score fast in 2026, without gimmicks and without confusing jargon.

What Is a Credit Score and Why Does It Matter?

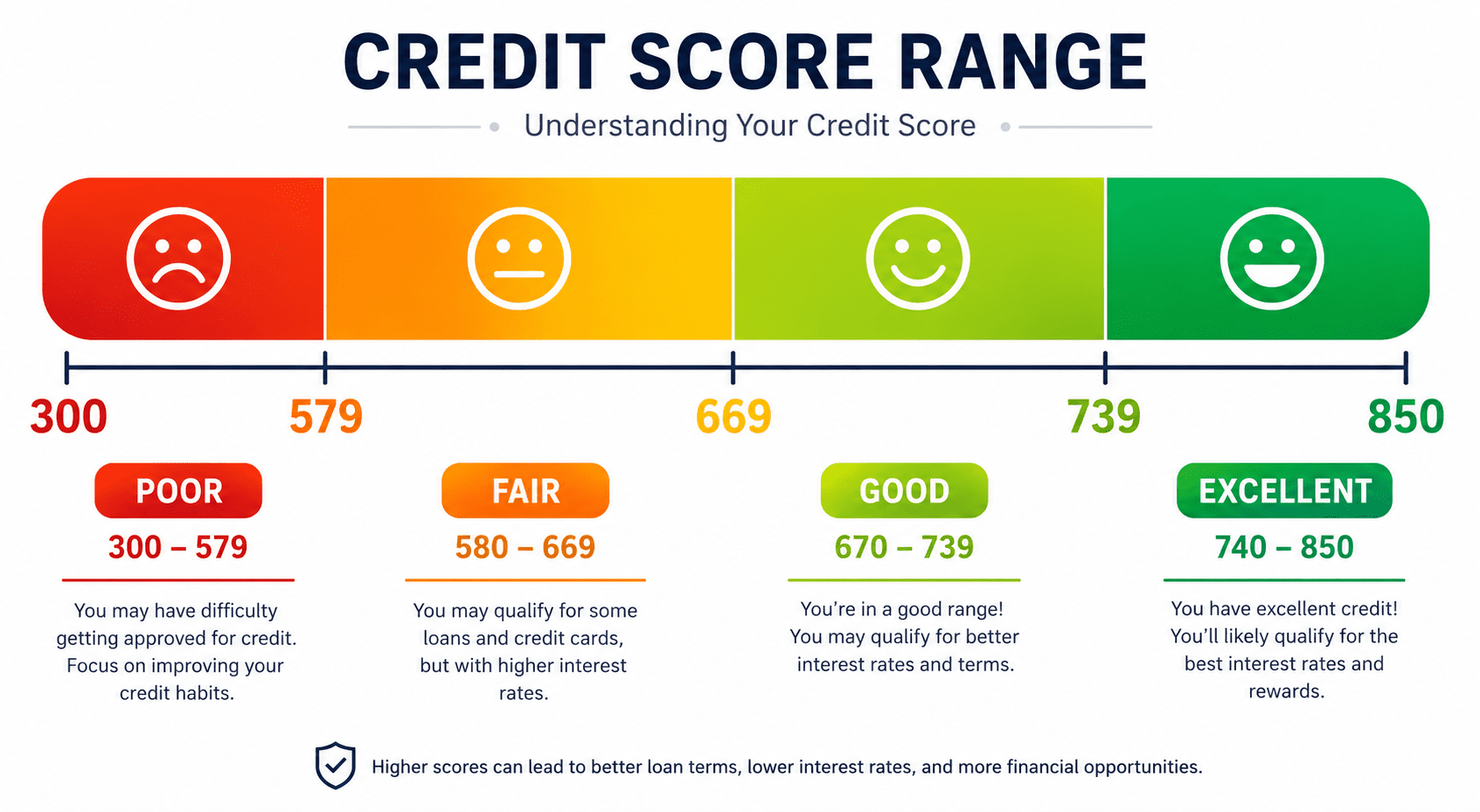

Your credit score is a three-digit number, typically ranging from 300 to 850, that tells lenders how risky it is to loan you money. The most commonly used model is the FICO score, and most lenders consider anything above 670 to be “good.”

Here is a quick breakdown of the credit score range:

- 300 to 579: Poor

- 580 to 669: Fair

- 670 to 739: Good

- 740 to 799: Very Good

- 800 to 850: Exceptional

The higher your credit score, the better the terms you can get on loans, credit cards, and mortgages. A difference of even 50 points on your credit score can mean thousands of dollars saved over the life of a mortgage.

What Factors Make Up Your Credit Score?

Before you can improve your credit score, you need to understand what goes into it. Your FICO score is calculated using five main factors:

1. Payment History (35%) This is the biggest factor by far. Paying your bills on time, every time, is the single most powerful thing you can do to build and maintain a strong credit score.

2. Credit Utilization Ratio (30%) This is how much of your available credit you are using. If you have a $10,000 credit limit and a $4,000 balance, your credit utilization ratio is 40%. Experts recommend keeping it below 30%, and ideally below 10% if you want a high credit score.

3. Length of Credit History (15%) The longer your credit accounts have been open, the better. This is why closing old credit cards can sometimes hurt your credit score.

4. Credit Mix (10%) Lenders like to see that you can handle different types of credit, such as credit cards, installment loans, and mortgages.

5. New Credit Inquiries (10%) Every time you apply for new credit, a hard inquiry shows up on your credit report. Too many hard inquiries in a short period can temporarily lower your credit score.

How to Improve Your Credit Score Fast in 2026

Now that you know what affects your credit score, here are the most effective strategies to raise your credit score quickly.

1. Always Pay Your Bills on Time

This sounds obvious, but it is the most important credit score tip of all. Payment history makes up 35% of your FICO score. A single missed payment can drop your credit score by 50 to 100 points, and that negative mark can stay on your credit report for up to seven years.

Set up autopay for at least the minimum payment on all your accounts. That way, you never accidentally miss a due date. If you have missed payments in the past, the damage fades over time as long as you stay consistent going forward.

2. Lower Your Credit Utilization Ratio

If you want to improve your credit score fast, reducing your credit utilization ratio is one of the quickest ways to see results. Since credit card balances are reported to the credit bureaus each month, paying down your balances can boost your score within 30 to 60 days.

Here is how to lower your credit utilization ratio:

- Pay down existing balances as aggressively as you can

- Ask your credit card company for a credit limit increase (without spending more)

- Keep older credit cards open even if you do not use them, because they contribute to your total available credit

- Spread balances across multiple cards rather than maxing out one

Keeping your credit utilization below 30% is the standard advice, but if you really want to raise your credit score fast, try to get it under 10%.

3. Check Your Credit Report for Errors

This is one of the most underused credit score tips, and it can make a big difference. According to the Federal Trade Commission, about one in five Americans has an error on their credit report. These errors can drag your credit score down significantly.

You are entitled to one free credit report per year from each of the three major bureaus, Equifax, Experian, and TransUnion, through AnnualCreditReport.com. In 2026, you can actually access your credit reports weekly for free.

Look for things like:

- Accounts that are not yours

- Late payments that you actually paid on time

- Incorrect personal information

- Duplicate accounts

- Paid-off debts still showing a balance

If you find errors, dispute them directly with the credit bureau. By law, they must investigate within 30 days. Getting even one error removed can improve your credit score by 20 to 100 pointS.

4. Become an Authorized User on Someone Else’s Account

If someone in your life, like a parent or spouse, has a credit card with a long history of on-time payments and a low credit utilization ratio, ask them to add you as an authorized user. Their positive credit history can show up on your credit report and give your credit score a meaningful boost.

You do not even have to use the card. Just being listed as an authorized user is enough to benefit from their good credit habits. This is one of the fastest credit score tips for people who are just starting to build credit or who have had setbacks.

5. Do Not Close Old Credit Accounts

It might feel good to close a credit card you no longer use, but doing so can actually hurt your credit score. Here is why: closing an account reduces your total available credit, which increases your credit utilization ratio. It also shortens your average length of credit history.

If a card has no annual fee, keep it open. Use it occasionally for a small purchase and pay it off immediately. That keeps the account active and benefits your credit score without any risk.

6. Limit New Credit Applications

Every time you apply for a new loan or credit card, the lender does a hard inquiry on your credit report. One hard inquiry typically drops your credit score by 5 to 10 points. That might seem small, but if you apply for several things at once, it adds up.

In 2026, be strategic about when you apply for new credit. If you know you will need a mortgage or car loan in the next six months, avoid opening new accounts in the meantime. Your credit score will thank you.

7. Consider a Credit Builder Loan

If you have thin credit history or a poor credit score, a credit builder loan can be a smart tool. These loans, offered by credit unions and some online lenders, are specifically designed to help people build or rebuild credit.

The way it works is simple: you make fixed monthly payments over a set period, and those payments get reported to the credit bureaus. Since payment history is the biggest factor in your credit score, consistently making on-time payments on a credit builder loan can improve your credit score in a relatively short time.

8. Use a Secured Credit Card

A secured credit card is another excellent option for people looking to improve their credit score from scratch or after financial hardship. You put down a deposit, which becomes your credit limit, and then use the card like a regular credit card. Payments are reported to the credit bureaus, so responsible use builds your credit score over time.

Look for secured credit cards with low fees and a pathway to upgrade to an unsecured card after six to twelve months.

How Long Does It Take to Improve Your Credit Score?

This depends on where you are starting from and what actions you take. Some credit score improvements are fast. Paying down a high credit card balance, for example, can show up in your credit score within one to two billing cycles.

Other improvements take more time. Rebuilding after a missed payment, a collection account, or bankruptcy can take months or even years of consistent positive behavior.

Here is a rough timeline for how quickly common actions affect your credit score:

- Lowering credit utilization: 30 to 60 days

- Disputing and removing errors: 30 to 45 days

- Becoming an authorized user: 30 to 60 days

- Building a 12-month on-time payment history: 6 to 12 months

- Recovering from a late payment: 12 to 24 months of on-time payments to minimize impact

The key takeaway is that there is no shortcut that works overnight. Anyone promising to raise your credit score to 800 in a week is not being truthful. But consistent, smart habits applied over a few months can produce real, meaningful results.

Best Credit Monitoring Apps in 2026

Keeping an eye on your credit score is important while you are working to improve it. These apps let you track your credit score for free and alert you to changes on your credit report:

- Credit Karma: Free credit score updates using TransUnion and Equifax data

- Experian App: Free FICO score from Experian, with credit report access

- Credit Sesame: Real-time credit monitoring and personalized tips

- Mint: Combines budgeting with credit score tracking

Regular monitoring helps you catch identity theft, errors, and score changes so you can respond quickly.

Common Credit Score Mistakes to Avoid

Even people actively trying to improve their credit score can make mistakes that slow their progress. Watch out for these:

- Only making minimum payments: It keeps accounts current but does not reduce your credit utilization fast enough

- Maxing out cards even if you pay in full: If the balance is reported before your due date, it shows high utilization

- Applying for too many cards at once: Multiple hard inquiries signal financial stress to lenders

- Ignoring your credit report: You cannot fix what you do not know about

- Falling for credit repair scams: Legitimate credit repair takes time; no one can legally remove accurate negative information

Final Thoughts: Start Improving Your Credit Score Today

Your credit score affects more parts of your financial life than you might realize. Whether you want to buy a home, get a better interest rate on a loan, or simply feel more financially secure, improving your credit score is one of the highest-impact moves you can make in 2026.

The good news is that the path forward is straightforward. Pay on time. Reduce what you owe. Check your credit report regularly. Do not close old accounts. And be patient with the process.

Start with one or two of the credit score tips in this guide and build from there. Small, consistent actions add up. Six months from now, you could be looking at a significantly higher credit score and all the financial doors that come with it.

Looking for more ways to strengthen your finances? Check out our guides on How to Build an Emergency Fund and How to Pay Off Debt Fast right here on Fiscible.