To save money on a tight budget is no game. Let’s be real. Saving money when your paycheck barely covers the basics feels almost impossible. You cut the coffee shop visits, you skip the weekend plans, and somehow, the savings account is still looking empty at the end of the month.

If that sounds familiar, you’re not alone. The U.S. personal savings rate was sitting at just 4.0% in late 2025, well below the 6 to 8 percent that most financial advisors recommend. That means the majority of Americans are struggling to put anything meaningful away.

But here’s the thing: you don’t need a massive income to save money. You need the right system and a few honest habits. This guide walks you through practical, no-fluff ways to save money on a tight budget in 2026, even if you feel like there’s nothing left over.

First, Understand Where Your Money Actually Goes

Before you can save anything, you need to know what’s eating your paycheck. Most people have a rough idea but not an accurate one.

Spend one month tracking every single dollar. Every coffee, every app subscription, every impulse buy at the checkout line. You can use a free app like Mint or just go through your bank statements. The goal isn’t to judge yourself. The goal is to see the full picture.

What usually shows up when people do this?

- Subscriptions they forgot about

- Eating out more than they realized

- Small purchases that add up to a lot

- Utilities that could be trimmed

This one step alone can uncover $100 to $300 a month that’s quietly disappearing. You can’t fix what you can’t see.

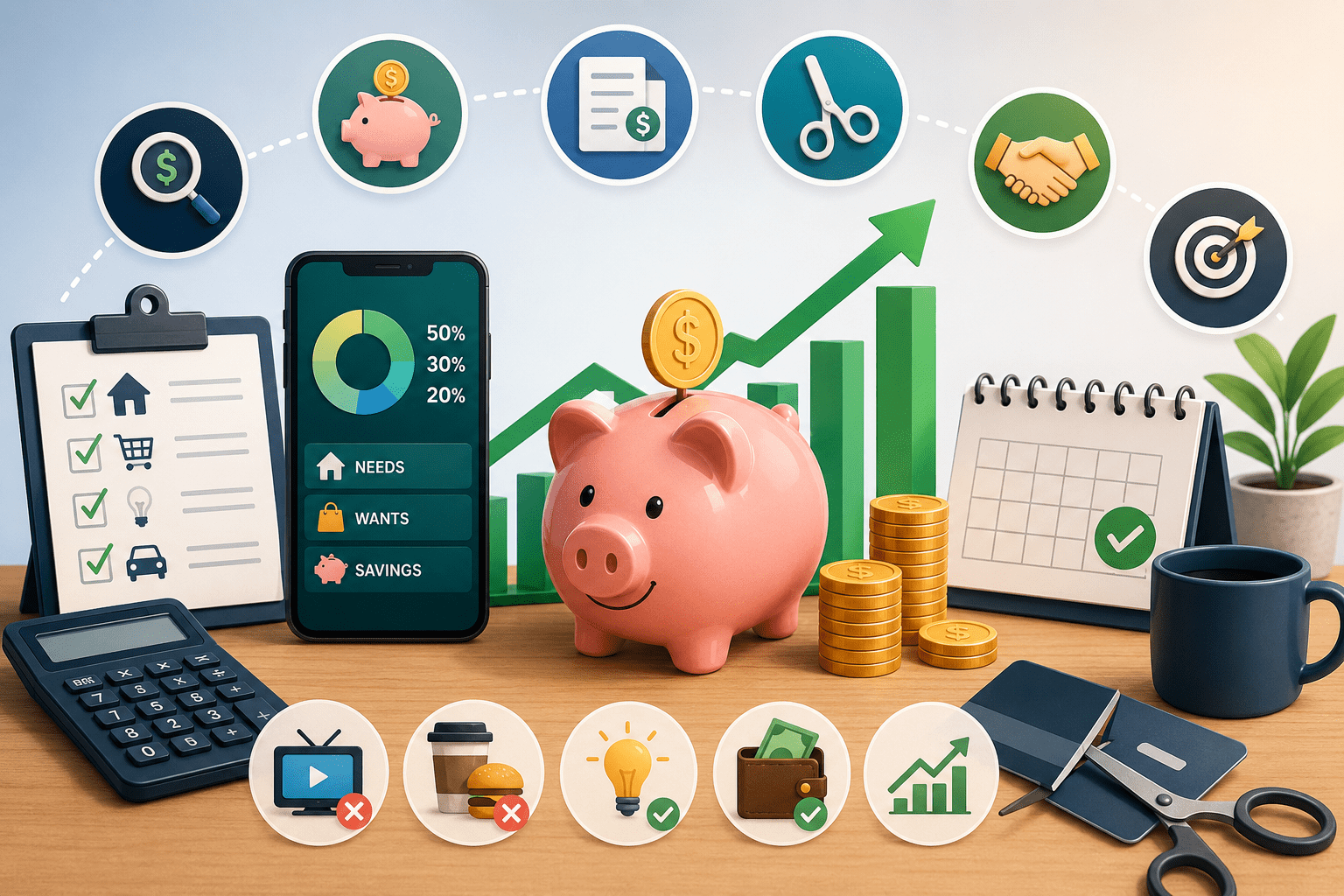

Use the 50/30/20 Rule as a Starting Framework

If you’ve never budgeted before or your current budget isn’t working, the 50/30/20 rule gives you a simple structure to start with.

Here’s how it breaks down:

- 50% of your after-tax income goes toward needs: rent, groceries, utilities, transportation, insurance

- 30% goes toward wants: dining out, entertainment, subscriptions, shopping

- 20% goes toward savings and debt repayment

Now, on a tight budget, the 30% for wants might feel laughable. That’s okay. Think of this as a target, not a rigid rule. Even shifting toward a 60/20/20 split where you cut wants and protect your savings is a solid move. The point is to assign every dollar a purpose.

Automate Your Savings Before to save money

This is the single most effective savings habit there is. Most people try to save what’s left over at the end of the month. That approach almost never works because there’s never anything left.

Flip the order. The moment your paycheck hits your account, set up an automatic transfer to a separate savings account. Even $25 or $50 a week matters.

If it’s not in your checking account, you won’t spend it. It’s that simple.

The psychological trick here is real. Once you stop seeing that money as “available,” you adjust your spending to what remains. Over 12 months, saving just $50 a week adds up to $2,600. That’s a real emergency fund.

Make Your Savings Work Harder With a High-Yield Savings Account

If you’re parking your savings in a regular bank account earning 0.39% interest, you’re leaving money on the table. Right now, the best high-yield savings accounts are offering APYs of up to 5.00%. That’s more than 10 times the national average.

Some strong options in 2026 include accounts from Varo Money, SoFi, Capital One 360, and Ally. Most of these are online banks with no monthly fees and no minimum balance requirements. They’re FDIC-insured, so your money is just as safe as it would be in any traditional bank.

The difference matters more than you’d think. On a $5,000 emergency fund, a 5% APY earns you $250 a year in interest. A traditional savings account at 0.39% earns you about $19. That’s free money you’re missing out on just because of where you keep your savings.

Moving your savings to a high-yield account takes about 15 minutes. It’s one of the easiest wins in personal finance right now.

Cut These Common Budget Drains First to save money

When you’re on a tight budget, small leaks sink the ship. Here are the areas that tend to bleed the most money quietly:

Subscriptions You’re Not Using

The average American household pays for 4 to 6 streaming services, plus software, fitness apps, box subscriptions, and more. Audit every subscription you’re paying for right now. Cancel anything you haven’t used in the last 30 days. For the ones you want to keep, check if there are promotional rates available. Many services offer discounted rates if you cancel and re-subscribe.

Eating Out Too Often

This is where most people’s budgets take the biggest hit. Cooking at home doesn’t mean eating rice and beans every night. It just means planning ahead. Batch cooking on Sundays, meal prepping lunches, and keeping a stocked pantry can cut your food spending significantly without making every meal feel like a sacrifice and you can save money too.

Utility Bills

Small changes like switching to LED bulbs, adjusting your thermostat by just a couple of degrees, unplugging electronics when not in use, and using cold water for laundry can lower your utility bill by $20 to $50 a month. That’s $240 to $600 a year.

Convenience Fees and Late Fees

ATM fees from out-of-network banks, late payment fees on bills, and rush delivery charges are all completely avoidable. Set up automatic bill payments to avoid late fees. Find a bank that reimburses ATM fees if you use cash regularly.

Negotiate More Than You Think You Can

A lot of people don’t realize how much of their regular bills are negotiable. Cable and internet providers, cell phone carriers, insurance companies, and even some subscription services will lower your rate if you simply ask, especially if you mention a competitor’s price. In thi way, you can save money easily.

Call your internet provider and ask if there are any current promotions. Call your car insurance company and ask when you last had a rate review. Ask your cell phone carrier about loyalty discounts. These calls take 20 minutes and can save you $50 to $150 a month in some cases.

The worst they can say is no.

Build a Bare-Bones Budget for Months When Things Get Tight

Life isn’t consistent. Some months are harder than others. A useful tool is having what some financial counselors call a “bare-bones budget” ready to go. This is a stripped-down version of your budget that covers only the absolute essentials: rent, utilities, food, transportation, and minimum debt payments.

When things get particularly tight, you switch to this mode temporarily. It removes the guilt of cutting things out because the decision is already made in advance. You’re not scrambling. You’re executing a plan.

Use the 24-Hour Rule on Non-Essential Purchase

Impulse spending is one of the most common budget killers. In order to save money, when you see something you want to buy but don’t need, wait 24 hours. In most cases, you’ll find the urge passes. If you still want it after 24 hours and it fits your budget, you can buy it without guilt.

For bigger purchases over $50 or $100, stretch that window to 72 hours or a full week. This one rule alone can save the average person hundreds of dollars a month.

Set Specific Savings Goals, Not Vague Ones

“I want to save money” is not a goal. It’s a wish.

Try this instead: “I will save money $2,400 by December 31, 2026 by putting aside $200 per month.”

That’s specific, measurable, and tied to an action. When your savings goal has a number and a deadline, it becomes something you can track and feel momentum toward. Progress is motivating. Vague intentions are not.

What If You Have Literally Nothing Left Over?

If you’re in a situation where you’re truly living paycheck to paycheck with no wiggle room, the first step to save money isn’t a savings account. It’s increasing income or reducing fixed costs.

Options to consider:

- A side gig with flexible hours (freelancing, delivery driving, tutoring)

- Moving to a cheaper housing situation or getting a roommate

- Refinancing or consolidating high-interest debt to lower monthly payments

- Applying for utility assistance programs if you qualify

Once you create even $50 to $100 of breathing room, that’s when you can start to save money.The system only works if you have something to work with.

The Bottom Line

To Save money on a tight budget in 2026 isn’t about willpower or deprivation. It’s about building a system that works without you having to think about it constantly.

Start by tracking your spending for one month. Set up an automatic transfer to a high-yield savings account. Cut the subscriptions you’ve forgotten about. Negotiate your recurring bills. Give every dollar a job.

You don’t have to do all of this at once. Pick two of these steps this week and start there. Small, consistent progress is what actually builds wealth over time.

Looking to understand how your take-home pay breaks down and where your savings potential really is? Try the Take-Home Pay Calculator at Fiscible to get a clear picture of your numbers.