Learn exactly how to build an emergency fund in 2026. Discover how much to save, where to keep it, and proven strategies to reach your goal faster, even on a tight budget.

Introduction:

Picture this: your car breaks down on a Tuesday morning, the repair bill lands at $1,400, and your checking account has $340 in it. What do you do?

For millions of Americans, that situation doesn’t just cause stress. It kicks off a chain reaction of credit card debt, missed bills, and sleepless nights that can take months to recover from.

That’s where an emergency fund comes in. It’s the most important financial cushion you can build. It won’t make you rich, and it’s not the kind of thing you brag about. But it’s the thing that keeps every other financial goal alive when life doesn’t go as planned.

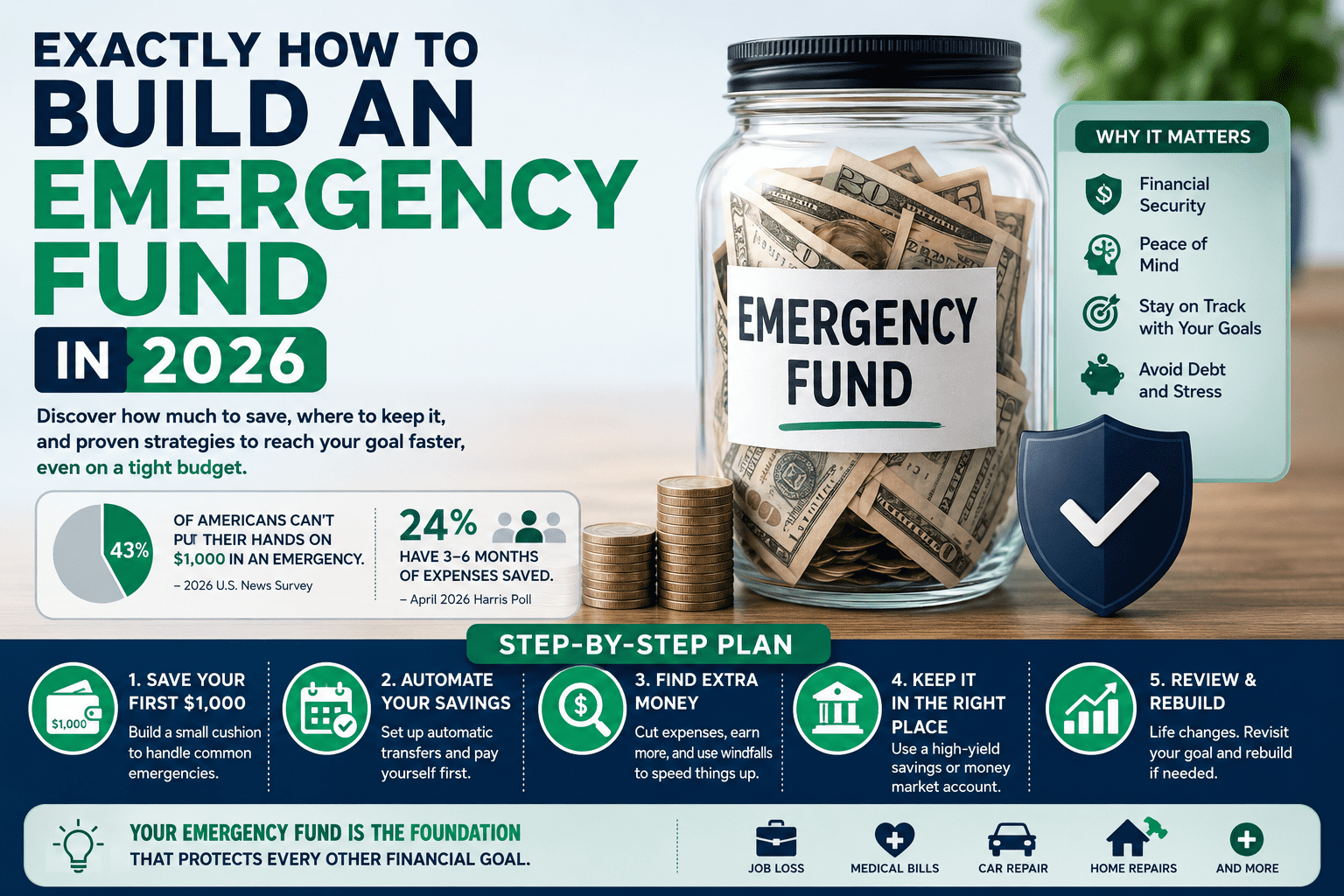

According to a 2026 U.S. News survey, 43% of Americans can’t put their hands on $1,000 in an emergency. An April 2026 Harris Poll found that while 78% of Americans have some money saved, only 24% have reached the recommended three to six months of essential expenses. The rest are just one bad day away from serious financial trouble.

This guide covers everything you need to know, including how much to save, where to keep it, and how to build it from scratch, even if you’re starting with nothing.

What Is an Emergency Fund (and What It Is Not)?

An emergency fund is a pot of cash you set aside specifically for unexpected financial emergencies. The word unexpected is key here. A holiday shopping budget isn’t an emergency. A car insurance renewal you knew was coming isn’t an emergency. But a sudden job loss, a big medical bill, a burst pipe in your home, or an urgent flight back to see family, those are exactly what this money is for.

It is not:

- An investment account

- A vacation savings fund

- A backup for impulse purchases

- A CD or any account where your money gets locked up

The reason this matters is that you need to be able to access this money fast, within a day or two at most. The goal here isn’t to earn a huge return. It’s to have money available and safe when you need it most.

How Much Should You Save in Your Emergency Fund in 2026?

For a long time, the standard advice was to save three to six months of living expenses. That advice still holds, but the bar has moved a bit higher in 2026. With inflation still hanging around, job searches taking longer than they used to, and the economy feeling uncertain, most financial experts now recommend aiming for at least four to six months, and closer to nine months if your income isn’t steady.

Here’s a simple breakdown by situation:

3 months: Works well for households with two incomes, very stable jobs like government or tenured positions, low debt, and good employer benefits.

6 months: A better target if you’re a single-income household, work in a field that can be unpredictable like tech, media, or finance, freelance with some consistency, or have dependents relying on you.

9+ months: Makes sense if you’re self-employed, earn commissions, run your own business, or have high fixed expenses or ongoing health costs.

How to Calculate Your Number

Don’t use your total monthly spending as the starting point. Instead, figure out your essential monthly expenses only, the bills that absolutely must be paid no matter what:

- Rent or mortgage

- Utilities like electricity, gas, water, and internet

- Groceries (a realistic amount, not a generous one)

- Insurance premiums for health, car, and home or renters

- Minimum payments on any debts like student loans, car loans, or credit cards

- Childcare or regular medications

Example: If your essential monthly expenses add up to $3,200, here’s what your target looks like:

- 3-month fund: $9,600

- 6-month fund: $19,200

- 9-month fund: $28,800

If you’re a single-income household, start with the six-month target and work toward it one step at a time.

Where Should You Keep Your Emergency Fund?

A lot of people make a simple but costly mistake here. They leave their emergency savings sitting in a regular checking account where it earns almost nothing, or they mix it in with their spending money and slowly chip away at it without realizing it.

Your emergency fund needs a home that is safe, easy to access, and earning a decent return.

High-Yield Savings Accounts (HYSA), Best for Most People

A high-yield savings account is the go-to choice for most people, and for good reason. As of May 2026, the best accounts are offering annual rates between 3.10% and 5.00%. Compare that to the national average of just 0.39% on a regular savings account, and you start to see the difference. A $10,000 emergency fund in a high-yield account at 3.10% earns around $320 a year. In a regular savings account, that same money earns about $39. Same balance, same easy access, but much better results.

Things to look for when choosing a HYSA:

- FDIC or NCUA insured up to $250,000

- No monthly fees

- No minimum balance (or a very low one)

- Fast transfers (same-day or next-day)

- Easy online and mobile access

Online banks tend to offer the best rates because they don’t have the overhead costs of running physical branches.

Money Market Accounts, A Solid Option Too

Money market accounts work similarly to high-yield savings accounts. They’re FDIC insured, earn competitive interest, and are easy to access. Some also come with check-writing privileges or a debit card, which can be handy if you want even faster access to your money in a pinch.

What to Avoid

- Regular checking accounts: The interest rate is almost zero, and it’s too easy to spend the money.

- Certificates of Deposit (CDs): Your money gets locked in for a fixed period, and you’ll pay a penalty for taking it out early. Emergencies don’t wait for CDs to mature.

- Stocks or investment accounts: The stock market can drop 20% to 30% at any time. Your emergency fund needs to be worth what you put in when you need it, not whatever the market decides on that day.

How to Build Your Emergency Fund: A Step-by-Step Plan

Looking at a six-month savings target can feel overwhelming. The key is to stop looking at the big number and focus on the very next step in front of you.

Step 1: Save Your First $1,000

Before you think about three or six months of savings, aim for $1,000. This idea, sometimes called “Baby Step 1,” exists because most real-world emergencies cost less than $1,000. A car repair, a doctor’s visit, a broken appliance, these things happen to everyone. Having $1,000 means you can handle it without reaching for a credit card.

Give yourself a deadline. Most people can save $1,000 in sixty to ninety days if they stay focused.

Step 2: Set Up Automatic Transfers

Willpower alone doesn’t build savings. What actually works is removing the decision entirely. Set up an automatic transfer from your checking account to your high-yield savings account for the day right after your paycheck comes in. You decide once, and the system handles it from there.

Even $50 or $100 a week adds up faster than it feels like it will. At $100 a week, you’re putting away $5,200 in a year. Start with what you can genuinely afford, then bump it up when you can.

Step 3: Find Extra Money to Speed Things Up

If your budget feels tight, here are some realistic ways to free up cash:

Look at your subscriptions. The average household is paying for four to seven subscriptions they barely use. Canceling just two of them at $15 each saves $360 a year. That goes straight into your fund.

Send windfalls straight to savings. Tax refunds, work bonuses, birthday money, extra income from a side gig, all of it goes into your emergency account before it gets spent anywhere else. A $2,000 tax refund can do more for your savings in one day than a year of small weekly transfers.

Sell things you don’t use. A few hours on eBay, Facebook Marketplace, or Poshmark can turn old clothes, electronics, and household items into real cash. That money goes into savings, not back into spending.

Cut back temporarily, not forever. You don’t have to live like a monk for the rest of your life. Just pull back on dining out, entertainment, and non-essential spending for two to three months and watch your savings jump. A short-term push can dramatically shorten your timeline.

Step 4: Keep It Separate and Label It

Open a dedicated high-yield savings account, preferably at a different bank than where you do your everyday spending, and give it a name. Call it “Emergency Only” or “Do Not Touch” or whatever helps it feel off-limits. Research in behavioral finance shows that people dip into separate, labeled accounts far less often than money sitting in a general account. The small friction of logging into a different app and seeing that label is genuinely enough to stop most unnecessary withdrawals.

Step 5: Review and Rebuild When Needed

Your emergency fund isn’t something you set up once and forget. Review it a couple of times a year. If your expenses have gone up, say you moved to a more expensive apartment, had a baby, or took on a car loan, your target number goes up too. And if you ever use the fund for an actual emergency, rebuilding it goes back to the top of your financial to-do list before anything else.

Common Emergency Fund Mistakes to Avoid

Mistake #1: Putting emergency savings in the stock market. It’s tempting to want your money working harder, but this is a real risk. When the market drops, and it does drop, your emergency fund drops with it. That’s the worst possible timing. Keep this money somewhere safe and boring.

Mistake #2: Saving too much in cash. There is such a thing as too much in an emergency fund. Once you’ve got twelve months of expenses saved, the extra cash is losing ground to inflation while sitting there. At that point, it’s smarter to put additional savings toward investments or paying down debt.

Mistake #3: Dipping into it for non-emergencies. A flight sale is not an emergency. A new phone is not an emergency. If you keep pulling from this account for things that aren’t real emergencies, it might mean you need a separate savings account for those planned but irregular expenses, things like car maintenance, holiday gifts, or vacations.

Mistake #4: Waiting for the “right time” to start. The best time to build an emergency fund is before you need it. The second best time is right now. Even $25 a week is a real start, and it builds the habit that matters most.

Final Thoughts: Your Emergency Fund Is the Base of Everything Else

All the bigger financial goals, investing, building wealth, paying off your mortgage, saving for retirement, none of them are secure without an emergency fund underneath them. The reason most people raid their 401(k) early, go into credit card debt over a car repair, or take out a personal loan for a medical bill is simple: they didn’t have an emergency fund to catch them.

Pulling $10,000 early from a 401(k) can cost $3,000 to $4,000 in taxes and penalties, and you permanently lose years of compound growth. Putting a $5,000 emergency on a credit card at 24% interest and paying it back with minimums can take over nine years and cost nearly $4,800 in extra interest. That’s almost double the original bill.

Your emergency fund stops all of that from happening. It’s not exciting. It won’t make you wealthy on its own. But it’s the thing that protects every other financial decision you make.

Start today. Open a high-yield savings account, give it a name, and transfer whatever you can right now. Six months from now, you’ll be really glad you did.

One thought on “HOW TO BUILD AN EMERGENCY FUND IN 2026: THE COMPLETE STEP-BY-STEP GUIDE”